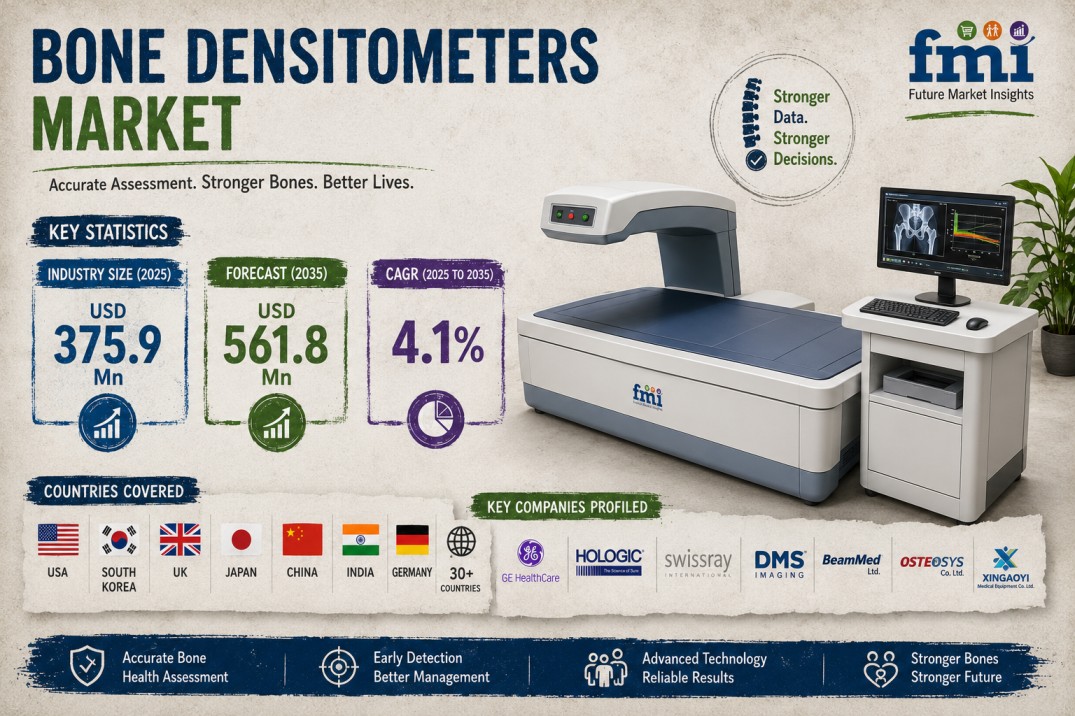

The global bone densitometers market is poised for steady expansion as healthcare providers accelerate equipment modernization and prioritize digitally integrated diagnostic infrastructure. Valued at USD 391.3 million in 2026, the market is projected to reach USD 584.8 million by 2036, growing at a 4.1% CAGR during the forecast period.

Growth is increasingly tied to procurement transformation rather than purely new installation volume. As hospitals replace aging densitometry systems and expand enterprise imaging capabilities, procurement teams are prioritizing technologies that improve workflow efficiency, interoperability, service reliability, and long-term lifecycle value. Bone densitometers, once viewed primarily as standalone osteoporosis diagnostic devices, are now becoming strategic components of hospital-wide digital imaging ecosystems.

The market remains heavily concentrated in core densitometry applications, with DXA systems accounting for 63.0% of total demand in 2026, reflecting their continued role as the clinical gold standard for osteoporosis diagnosis and fracture risk assessment. Meanwhile, hospitals dominate end-user demand with a 56.0% market share, driven by large-scale enterprise purchasing and imaging standardization initiatives. Regionally, China leads growth at 5.3% CAGR, supported by expanding healthcare infrastructure and rising osteoporosis screening adoption.

Market Overview

The bone densitometers industry is evolving from a traditional medical device segment into a strategically important component of digital healthcare infrastructure. Historically, procurement decisions centered on scanner accuracy, acquisition cost, and basic service support. Today, purchasing decisions increasingly consider interoperability, cybersecurity, predictive maintenance, and software lifecycle management.

This shift is being driven by rising osteoporosis prevalence, aging populations, and increasing demand for preventive diagnostics. Healthcare systems are under pressure to improve diagnostic throughput while integrating imaging technologies into unified enterprise platforms.

The market’s rise from USD 391.3 million in 2026 to USD 584.8 million by 2036 reflects this transition. Hospitals increasingly evaluate vendors not just on hardware performance but on their ability to deliver long-term enterprise imaging support and service partnerships.

Key Growth Drivers

The strongest growth driver is the rising prevalence of osteoporosis and age-related bone disorders. Aging populations across developed and emerging markets are significantly increasing the need for bone mineral density testing.

Replacement demand is another major catalyst. Many hospitals continue operating older DXA systems that lack workflow automation, advanced software analytics, and modern connectivity features.

Hospital modernization initiatives are also accelerating demand. Large healthcare networks are investing in digitally integrated imaging environments to improve efficiency, reduce operational silos, and standardize patient care workflows.

Growing awareness of preventive healthcare and fracture risk management is further supporting adoption of densitometry technologies across hospitals, specialty clinics, and imaging centers.

Technology & Innovation Trends

Technology innovation in bone densitometry is increasingly focused on digital integration and workflow optimization.

DXA systems, expected to hold 63.0% market share in 2026, remain the dominant technology due to their clinical accuracy and widespread adoption for osteoporosis diagnosis.

Advanced software capabilities are becoming critical purchasing criteria. Hospitals increasingly demand automated reporting, centralized image storage, cloud connectivity, and AI-assisted workflow tools.

Predictive maintenance systems are emerging as a major value-add in vendor contracts. These capabilities reduce downtime and improve equipment utilization.

Enterprise imaging integration is another disruptive trend. Instead of isolated densitometry systems, providers increasingly prefer solutions that connect directly with PACS, EMR, and broader radiology workflows.

Cybersecurity is also becoming a major differentiator as connected medical devices face increasing digital risk exposure.

Market Challenges & Restraints

Despite favorable demand trends, the market faces structural constraints.

One major challenge is high capital expenditure, particularly for advanced DXA systems integrated into enterprise imaging platforms.

Budget constraints in public healthcare systems often delay replacement cycles, extending equipment usage well beyond optimal lifecycle timelines.

Integration complexity presents another challenge. Hospitals with legacy IT infrastructure may face difficulties incorporating modern densitometry systems into existing digital ecosystems.

Procurement cycles are also becoming more complex due to increased stakeholder involvement, including radiology departments, IT teams, finance groups, and cybersecurity specialists.

Vendor lock-in concerns remain a key restraint for organizations considering single-supplier strategies.

Segment Analysis

By Technology

DXA leads with 63.0% share in 2026, supported by strong clinical acceptance and broad reimbursement support.

Peripheral DXA, quantitative ultrasound, and CT-based systems serve specialized or niche diagnostic applications.

By End User

Hospitals account for 56.0% of total demand, making them the dominant end-user segment.

Large hospital networks increasingly bundle densitometry procurement into broader imaging modernization initiatives.

Diagnostic imaging centers and specialty clinics continue contributing steady demand.

By Application

Osteoporosis diagnosis remains the leading application, driven by rising screening rates among aging populations.

Fracture risk assessment and body composition analysis are also gaining importance in clinical and wellness settings.

Research and academic use continue supporting demand in advanced institutions.

Regional Analysis

Asia Pacific

Asia Pacific remains the fastest-growing region for bone densitometers.

China leads global growth at 5.3% CAGR through 2036, driven by healthcare expansion, rising diagnostic awareness, and increasing elderly populations.

Growing public health focus on osteoporosis screening is supporting adoption across major hospital systems.

Other Asia Pacific markets are also expanding as healthcare infrastructure modernizes.

North America

North America remains a high-value market supported by strong reimbursement frameworks and advanced healthcare infrastructure.

Replacement demand is a major driver as hospitals upgrade aging densitometry systems to digitally connected platforms.

Large integrated delivery networks continue prioritizing enterprise procurement contracts.

Europe

Europe maintains stable growth supported by mature diagnostic infrastructure and preventive care initiatives.

Hospitals across the region increasingly prioritize interoperability, cybersecurity, and lifecycle service support when evaluating vendors.

Aging demographics continue supporting long-term densitometry demand.

Procurement Trends: Single vs Multi-Supplier Models

Procurement strategies are becoming a major competitive battleground in the bone densitometers market.

Single-supplier models are gaining popularity among hospitals seeking standardized workflows and integrated imaging ecosystems. Benefits include:

- Centralized software management

- Reduced workflow variability

- Easier staff training

- Lower maintenance complexity

- Stronger enterprise pricing leverage

Single-vendor agreements often include longer warranties, implementation support, and service guarantees.

However, multi-supplier models remain relevant for organizations prioritizing flexibility and competitive pricing. These models allow healthcare providers to:

- Reduce dependency on a single vendor

- Access specialized innovations

- Maintain pricing leverage

- Minimize technology lock-in risk

This creates an ongoing strategic debate between operational standardization and procurement flexibility.

Contract Evolution and Service Models

Contract structures in the bone densitometers market are becoming far more comprehensive.

Traditional procurement focused mainly on hardware purchase and installation. Modern enterprise contracts increasingly include:

- Software upgrade pathways

- Predictive maintenance

- Cybersecurity protections

- Regulatory compliance support

- Performance guarantees

- Interoperability commitments

- Training programs

- Long-term service agreements

Hospitals increasingly view service quality and lifecycle support as equally important as equipment performance.

Competitive Landscape

Competition in the bone densitometers market is increasingly defined by enterprise service capabilities, interoperability, and lifecycle support rather than hardware specifications alone.

Vendors capable of supporting hospital digital transformation initiatives are gaining stronger competitive positioning.

Key competitive differentiators include:

- Enterprise imaging compatibility

- Predictive maintenance capability

- Cybersecurity compliance

- Service response times

- Software upgrade support

Manufacturers with strong long-term institutional relationships are expected to capture greater replacement opportunities.

Leading Companies Analysis

Major global players include GE HealthCare, Hologic, Fujifilm, and Diagnostic Medical Systems.

GE HealthCare and Hologic maintain strong market positions through broad imaging portfolios and established service infrastructures.

These companies benefit from enterprise-scale service networks and integrated imaging ecosystem capabilities.

Specialized manufacturers continue competing through innovation, niche technology differentiation, and flexible deployment models.

Investment & Strategic Developments

Recent investments highlight growing strategic emphasis on imaging modernization.

Healthcare providers are increasingly allocating capital toward replacement of aging DXA systems and broader digital imaging integration.

Manufacturers are investing in:

- Advanced software analytics

- Connected device ecosystems

- AI-assisted workflow tools

- Predictive maintenance services

- Cybersecurity infrastructure

Investments increasingly prioritize long-term service and software value over hardware-only differentiation.

Future Outlook

The future of the bone densitometers market will be shaped by three major shifts: equipment replacement cycles, enterprise imaging integration, and service-based procurement models.

Densitometry systems will become more central to preventive healthcare as osteoporosis screening demand rises globally.

Suppliers that combine hardware excellence with software innovation and long-term service capabilities will be best positioned to capture market value.

Conclusion

The global bone densitometers market is transitioning from a traditional equipment-driven segment into a strategically important component of enterprise imaging infrastructure. With market value projected to rise from USD 391.3 million in 2026 to USD 584.8 million by 2036, growth is being driven by replacement demand, hospital modernization, and digital integration initiatives.

As healthcare providers prioritize workflow efficiency, interoperability, and long-term resilience, procurement decisions will increasingly favor manufacturers capable of delivering integrated solutions and strategic service partnerships. Companies that align with evolving hospital procurement expectations will define the next decade of market leadership.

Explore More Related Studies Published by FMI Research

- The Orphan Drugs Market was valued at USD 198.00 billion in 2025. Sales are expected to reach USD 207.11 billion in 2026 and USD 324.72 billion by 2036.

- The Research Antibodies Market was valued at USD 5.60 Billion in 2025. Sales are expected to reach USD 6.05 Billion in 2026 and USD 13.19 Billion by 2036.

- The joint reconstruction devices market is projected to grow from USD 30.2 billion in 2025 to USD 47.3 billion by 2035, at a CAGR of 4.6%.

FMI Custom Research: Strategic Intelligence for Confident Decision-Making

In today’s rapidly evolving business environment, leadership teams need more than market data—they need clear, actionable intelligence tailored to their strategic objectives. FMI’s Custom Research solutions are designed around the specific business questions organizations need answered, enabling executives to evaluate growth opportunities, validate investments, assess competitive dynamics, and reduce uncertainty before making critical decisions. By combining deep industry expertise, primary research, and proprietary market intelligence, FMI delivers insights that help organizations move from assumptions to evidence-based strategies with greater speed and confidence.

Key Executive Benefits

- Decision-Ready Insights: Research tailored to your specific business challenges, growth plans, and investment priorities.

- Reduced Strategic Risk: Validate market opportunities, customer demand, and competitive positioning before committing resources.

- Market Entry Confidence: Assess opportunity size, regulatory barriers, channel dynamics, and competitive landscapes with precision.

- Competitive Advantage: Gain proprietary intelligence unavailable through syndicated reports or internal datasets.

- Faster Growth Decisions: Accelerate expansion, product development, portfolio optimization, and investment planning.

- Primary Market Validation: Access real-world customer, buyer, and stakeholder insights that support high-confidence decision-making.

- Global Industry Expertise: Powered by 100+ analysts, 20,000+ published reports, and 1.6 million+ hours of research experience.

- Proven Track Record: Over 7,000 market-entry engagements completed across six regions and 14 industry sectors with strong client retention.

Business Impact

FMI helps organizations transform market complexity into strategic clarity, enabling leadership teams to identify growth opportunities faster, optimize resource allocation, strengthen competitive positioning, and make high-stakes business decisions with confidence.

To explore how FMI Custom Research can support your strategic priorities, please connect with our team at – sales@futuremarketinsights.com

Contact Us

Future Market Insights Inc.

Christiana Corporate, 200 Continental Drive,

Suite 401, Newark, Delaware – 19713, USA

T: +1-347-918-3531

Why FMI: Future Market Insights – Why FMI

Website: Future Market Insights