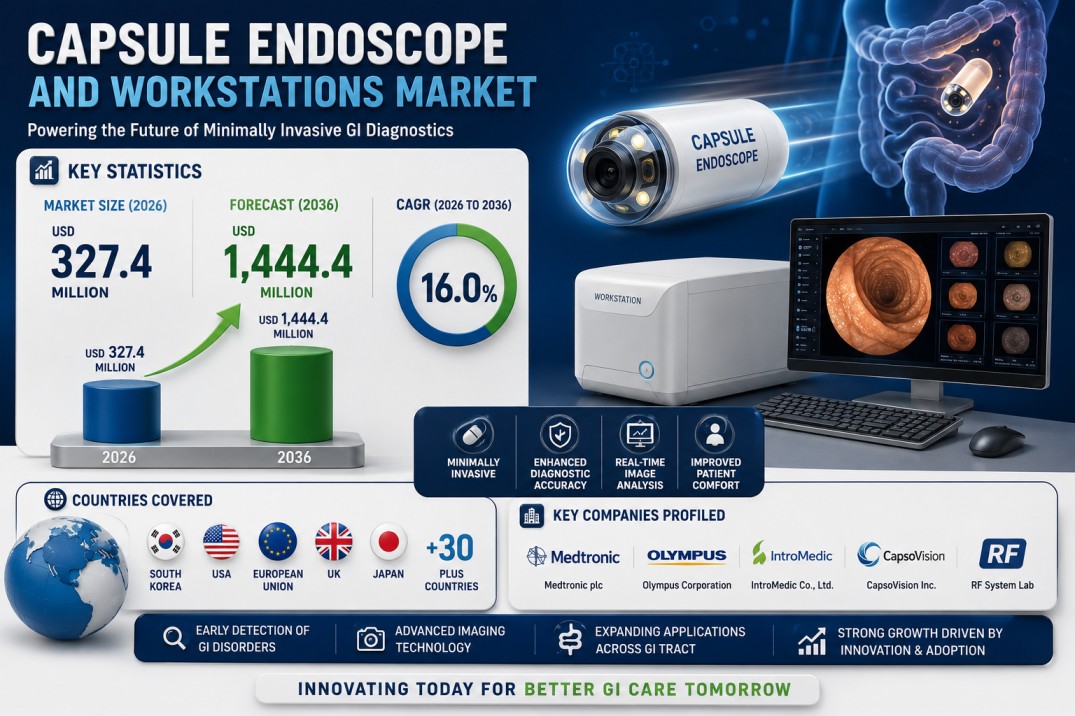

The global capsule endoscope and workstations market is positioned for rapid expansion as healthcare providers accelerate investments in minimally invasive gastrointestinal diagnostics and digitally integrated endoscopy infrastructure. Valued at USD 327.4 million in 2026, the market is projected to reach USD 1,444.4 million by 2036, growing at a 16.0% CAGR during the forecast period.

Growth is increasingly being shaped by procurement transformation rather than hardware adoption alone. Hospitals and ambulatory endoscopy centres are adopting capsule endoscopy solutions as part of broader gastrointestinal diagnostic modernization initiatives, integrating them into enterprise imaging and digital workflow ecosystems rather than treating them as standalone diagnostic tools.

The market remains highly concentrated in core capsule technologies, with capsule endoscopes accounting for 64.0% of the component segment in 2026, reflecting strong clinical adoption and regulatory confidence. Hospitals and large endoscopy centres continue to dominate demand, driven by enterprise purchasing strategies focused on standardization, software integration, and long-term service value. Regionally, South Korea (16.4% CAGR) and the United States (16.3% CAGR) are among the fastest-growing markets, supported by advanced healthcare digitization and strong diagnostic demand.

Market Overview

The capsule endoscope and workstations industry is evolving from a traditional medical device category into a strategically important component of digital gastroenterology infrastructure. Historically, purchasing decisions focused primarily on image quality, capsule performnce, and acquisition cost. Today, healthcare providers increasingly evaluate solutions based on software capabilities, artificial intelligence integration, interoperability, cybersecurity, and lifecycle service support.

This transition is being driven by rising gastrointestinal disease prevalence, increasing demand for minimally invasive diagnostics, and growing investments in digitally integrated healthcare environments.

The market’s growth from USD 327.4 million in 2026 to USD 1,444.4 million by 2036 reflects this transformation. Healthcare organizations are increasingly prioritizing vendors capable of delivering complete diagnostic ecosystems, long-term software support, and enterprise service partnerships.

Key Growth Drivers

The strongest growth driver is the rising prevalence of gastrointestinal disorders, including occult GI bleeding, inflammatory bowel disease, and small bowel tumors. These conditions require efficient, accurate, and patient-friendly diagnostic pathways.

Demand for minimally invasive diagnostics is another major catalyst. Capsule endoscopy enables visualization of gastrointestinal structures without invasive procedures, improving patient comfort and supporting outpatient workflows.

Healthcare modernization initiatives are also accelerating adoption. Hospitals and endoscopy centres are investing in digitally connected diagnostic ecosystems to improve efficiency, reduce workflow complexity, and standardize reporting.

Growing awareness of preventive diagnostics and earlier disease detection is further supporting market expansion across hospitals, specialty clinics, and ambulatory centres.

Technology & Innovation Trends

Innovation in capsule endoscopy is increasingly centered on digital integration, artificial intelligence, and workflow optimization.

Capsule endoscopes are expected to hold 64.0% market share in 2026, maintaining dominance due to strong clinical acceptance and expanding diagnostic applications.

Advanced workstation software is becoming a critical procurement criterion. Providers increasingly demand:

- AI-assisted image analysis

- Automated reporting

- Cloud-based image storage

- Centralized software management

- Advanced analytics capabilities

Artificial intelligence is emerging as a major differentiator by improving lesion detection, reducing review times, and enhancing diagnostic confidence.

Enterprise interoperability is another major trend. Providers increasingly prefer solutions that integrate with EMR, PACS, and broader gastroenterology information systems.

Cybersecurity has also become an important competitive factor as connected diagnostic systems face growing digital risk.

Market Challenges & Restraints

Despite strong demand, the market faces several structural challenges.

High capital and software subscription costs remain a major barrier, particularly for advanced AI-enabled diagnostic ecosystems.

Budget limitations in public and smaller healthcare systems can delay modernization and extend replacement cycles.

Integration complexity presents another challenge. Organizations operating legacy IT environments may face difficulties integrating modern capsule systems with existing enterprise infrastructure.

Procurement cycles are becoming increasingly complex due to the involvement of multiple stakeholders, including clinicians, IT departments, finance teams, and cybersecurity specialists.

Vendor dependency concerns remain a key restraint, particularly for organizations evaluating single-supplier strategies.

Segment Analysis

By Component

Capsule endoscopes lead the market with 64.0% share in 2026, supported by growing clinical adoption and regulatory compliance requirements.

Workstations represent a rapidly growing segment as software analytics and workflow management become increasingly valuable.

By Application

Small bowel diagnostics remains the leading application area.

Capsule technologies are particularly valuable for examining gastrointestinal regions that are difficult to access with traditional endoscopy.

Applications in bleeding detection, inflammatory bowel disease monitoring, and tumor screening continue to expand.

By End User

Hospitals and ambulatory endoscopy centres account for the majority of demand.

Large healthcare networks increasingly bundle capsule endoscopy procurement into broader enterprise digital transformation initiatives.

Specialized GI clinics continue contributing steady demand.

Regional Analysis

Asia Pacific

Asia Pacific remains one of the fastest-growing regions in the capsule endoscopy market.

South Korea leads with 16.4% CAGR, supported by advanced healthcare digitization, strong technology adoption, and increasing demand for minimally invasive diagnostics.

Other Asia Pacific markets are also expanding as healthcare infrastructure modernizes.

North America

North America remains a high-value market supported by advanced healthcare infrastructure and strong reimbursement mechanisms.

The United States is projected to grow at 16.3% CAGR, driven by strong investments in digital diagnostics, AI-enabled imaging, and enterprise healthcare platforms.

Large integrated healthcare systems continue prioritizing enterprise procurement contracts.

Europe

Europe maintains strong growth supported by mature diagnostic infrastructure and increasing adoption of minimally invasive GI diagnostics.

Healthcare providers increasingly prioritize interoperability, software lifecycle support, and cybersecurity when selecting vendors.

Procurement Trends: Single vs Multi-Supplier Models

Procurement strategies are emerging as a major competitive battleground in the capsule endoscope and workstations market.

Single-supplier models are gaining traction among hospitals seeking standardized workflows and integrated diagnostic ecosystems. Benefits include:

- Centralized software management

- Reduced workflow variability

- Easier staff training

- Lower maintenance complexity

- Stronger enterprise pricing leverage

Single-vendor agreements frequently include AI software licenses, implementation support, cloud services, and long-term service guarantees.

However, multi-supplier models remain important for providers prioritizing flexibility and competitive pricing. These models allow healthcare organizations to:

- Reduce dependency on a single vendor

- Access specialized innovations

- Maintain pricing leverage

- Improve supply chain resilience

This creates an ongoing strategic balance between operational standardization and procurement flexibility.

Contract Evolution and Service Models

Contract structures in the capsule endoscopy market are becoming increasingly comprehensive.

Traditional procurement focused mainly on hardware acquisition and basic maintenance. Modern enterprise contracts now commonly include:

- Software upgrade pathways

- Artificial intelligence capabilities

- Cybersecurity protections

- Cloud storage services

- Regulatory compliance support

- Performance guarantees

- Interoperability commitments

- Training programs

- Predictive maintenance services

Healthcare providers increasingly view software quality and lifecycle support as equally important as capsule hardware performance.

Subscription-based pricing models are becoming more common, especially for analytics and cloud services.

Competitive Landscape

Competition in the capsule endoscope and workstations market is increasingly defined by ecosystem capabilities, interoperability, and service infrastructure rather than hardware specifications alone.

Manufacturers capable of supporting digital transformation initiatives are gaining stronger competitive positioning.

Key competitive differentiators include:

- Enterprise diagnostic compatibility

- AI-assisted analytics

- Cybersecurity compliance

- Service response times

- Software upgrade support

Companies with strong long-term institutional relationships are expected to capture greater market share.

Leading Companies Analysis

Major global players include Medtronic, Olympus Corporation, AnX Robotica, and IntroMedic.

These companies maintain strong market positions through advanced imaging technologies, AI capabilities, and expanding service ecosystems.

Large manufacturers benefit from enterprise-scale support networks and integrated diagnostic platform capabilities.

Specialized innovators continue competing through niche imaging technologies and advanced analytics differentiation.

Investment & Strategic Developments

Recent investments highlight growing strategic emphasis on gastrointestinal diagnostic modernization.

Healthcare providers are allocating more capital toward:

- Advanced workstation software

- AI-assisted analytics

- Connected diagnostic ecosystems

- Cloud-based services

- Cybersecurity infrastructure

Manufacturers are increasingly prioritizing long-term software and service value over hardware-only differentiation.

Strategic partnerships between healthcare IT companies, AI firms, and cloud service providers are becoming more important.

Future Outlook

The future of the capsule endoscope and workstations market will be shaped by three major shifts: digital diagnostics expansion, enterprise integration, and service-based procurement models.

Capsule endoscopy will become increasingly central to gastrointestinal diagnostics as minimally invasive screening demand rises globally.

Suppliers that combine hardware innovation with advanced software capabilities and long-term service support will be best positioned to capture market value.

Conclusion

The global capsule endoscope and workstations market is transitioning from a hardware-driven medical device segment into a strategically important component of digital gastrointestinal diagnostic infrastructure. With market value projected to rise from USD 327.4 million in 2026 to USD 1,444.4 million by 2036, growth is being driven by rising demand for minimally invasive diagnostics, enterprise digital transformation, and evolving procurement strategies.

As healthcare providers prioritize workflow efficiency, interoperability, artificial intelligence, and long-term operational resilience, procurement decisions will increasingly favor manufacturers capable of delivering integrated solutions and strategic service partnerships. Companies aligned with these evolving enterprise expectations will define the next decade of market leadership.

Explore More Related Studies Published by FMI Research

- The surgical heart valves market was valued at USD 8.89 billion in 2025, projected to reach USD 10.24 billion in 2026, and is forecast to expand to USD 42.16 billion by 2036 at a 15.2% CAGR.

- The HSV testing market is projected to grow from USD 640.5 million in 2025 to USD 1,142.7 million by 2035, registering a CAGR of 6.0%.

- The chloramphenicol test kits market is projected to grow from USD 127.8 million in 2025 to USD 291.7 million by 2035, at a CAGR of 8.6%.

FMI Custom Research: Strategic Intelligence for Confident Decision-Making

In today’s rapidly evolving business environment, leadership teams need more than market data—they need clear, actionable intelligence tailored to their strategic objectives. FMI’s Custom Research solutions are designed around the specific business questions organizations need answered, enabling executives to evaluate growth opportunities, validate investments, assess competitive dynamics, and reduce uncertainty before making critical decisions. By combining deep industry expertise, primary research, and proprietary market intelligence, FMI delivers insights that help organizations move from assumptions to evidence-based strategies with greater speed and confidence.

Key Executive Benefits

- Decision-Ready Insights: Research tailored to your specific business challenges, growth plans, and investment priorities.

- Reduced Strategic Risk: Validate market opportunities, customer demand, and competitive positioning before committing resources.

- Market Entry Confidence: Assess opportunity size, regulatory barriers, channel dynamics, and competitive landscapes with precision.

- Competitive Advantage: Gain proprietary intelligence unavailable through syndicated reports or internal datasets.

- Faster Growth Decisions: Accelerate expansion, product development, portfolio optimization, and investment planning.

- Primary Market Validation: Access real-world customer, buyer, and stakeholder insights that support high-confidence decision-making.

- Global Industry Expertise: Powered by 100+ analysts, 20,000+ published reports, and 1.6 million+ hours of research experience.

- Proven Track Record: Over 7,000 market-entry engagements completed across six regions and 14 industry sectors with strong client retention.

Business Impact

FMI helps organizations transform market complexity into strategic clarity, enabling leadership teams to identify growth opportunities faster, optimize resource allocation, strengthen competitive positioning, and make high-stakes business decisions with confidence.

To explore how FMI Custom Research can support your strategic priorities, please connect with our team at – sales@futuremarketinsights.com

Contact Us

Future Market Insights Inc.

Christiana Corporate, 200 Continental Drive,

Suite 401, Newark, Delaware – 19713, USA

T: +1-347-918-3531

Why FMI: Future Market Insights – Why FMI

Website: Future Market Insights