According to the latest insights by Future Market Insights, the global microalgae industry is entering a critical commercialization phase as producers seek to bridge the gap between biological potential and large-scale economic viability. While microalgae offer sustainable sources of proteins, omega-3 fatty acids, pigments, antioxidants, and specialty bioactive compounds, only a limited number of countries have successfully developed commercial-scale production systems capable of competing in global ingredient markets.

Quick Stats of Microalgae Market

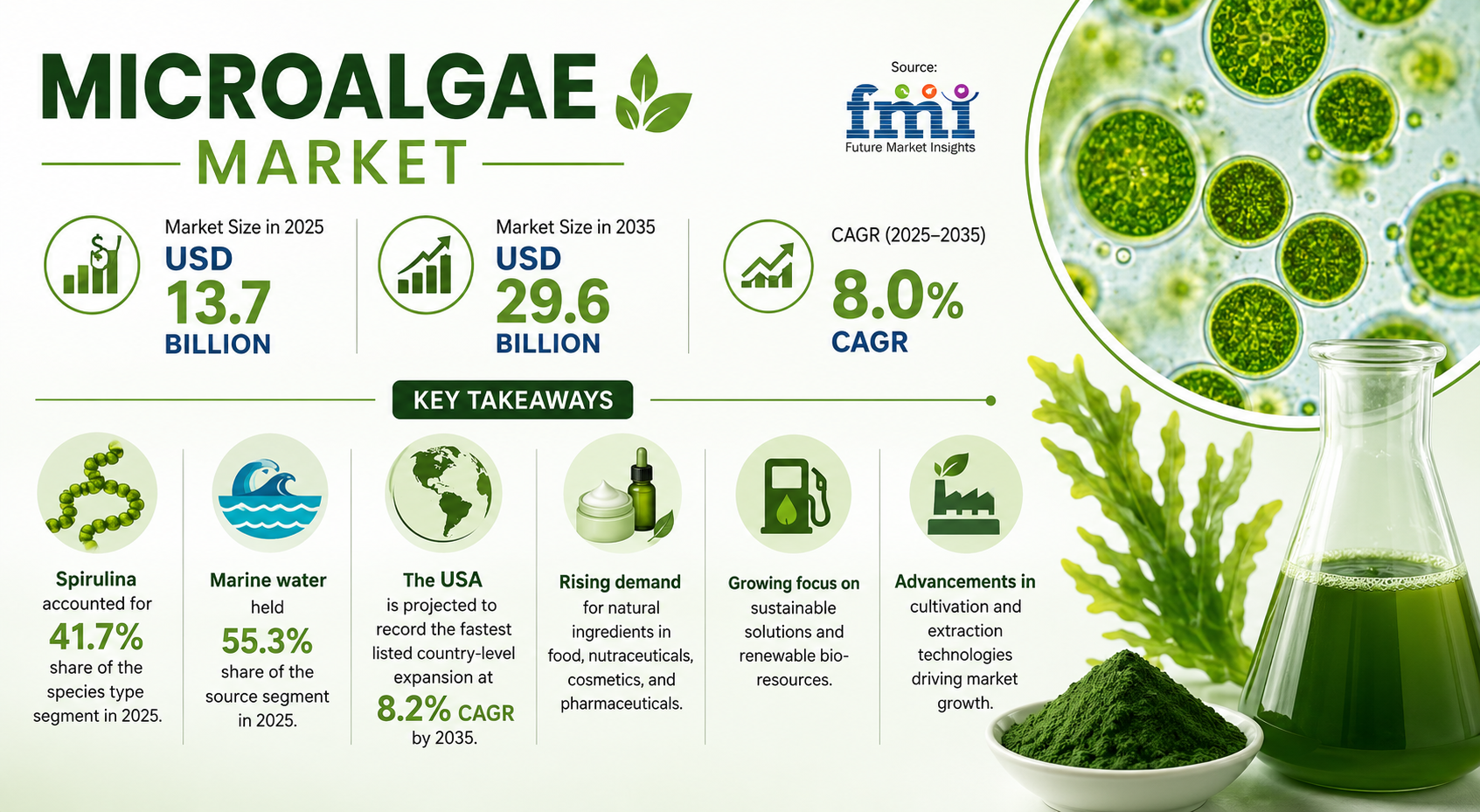

Market Size (2025): USD 13.7 Billion

Forecast Market Value (2035): USD 29.6 Billion

CAGR (2025–2035): 8.0%

Leading Species Type: Spirulina (41.7% Market Share)

Leading Source Segment: Marine Water (55.3% Market Share)

Fastest Growing Market: USA (8.2% CAGR)

Emerging Trend: Sustainable Algae Cultivation and High-Value Bioactive Ingredient Commercialization

Cultivation Systems Remain the Foundation of Commercial Competitiveness

The choice of cultivation technology continues to be one of the most important determinants of production economics within the microalgae industry.

Open raceway ponds remain the dominant production platform for commercially established species such as Spirulina and Chlorella. These systems offer lower capital requirements and reduced operational complexity, making them suitable for large-scale biomass production in regions with favorable climatic conditions.

However, open systems also face significant limitations including:

• Contamination risks

• Weather dependency

• Lower biomass concentrations

• Seasonal productivity fluctuations

• Reduced process control

To overcome these challenges, many producers are investing in closed photobioreactor systems that provide superior environmental control and higher productivity rates.

Closed cultivation technologies offer advantages including:

• Improved culture purity

• Higher biomass density

• Enhanced compound consistency

• Better traceability

• Reduced contamination exposure

While photobioreactors improve product quality and process reliability, their substantially higher capital and energy requirements continue to limit widespread adoption for lower-value ingredient applications.

As a result, cultivation system selection has become a strategic decision that directly influences long-term profitability and market positioning.

Harvesting and Drying Continue to Define Industry Economics

Harvesting and downstream processing remain the most significant barriers to commercial scalability across the microalgae value chain.

Unlike conventional agricultural crops, microalgae are produced in highly diluted liquid suspensions that require multiple concentration and dewatering stages before they can be converted into commercial ingredients.

Manufacturers must navigate complex processing steps including:

• Flocculation and concentration

• Sedimentation and flotation

• Centrifugation

• Membrane filtration

• Drying and stabilization

Each stage introduces additional costs, energy consumption, and potential biomass losses.

Drying remains particularly challenging due to its high energy intensity. Whether utilizing spray drying, drum drying, or freeze-drying technologies, processors must balance product quality with operating costs while maintaining ingredient functionality.

Industry experts report that harvesting and drying can collectively account for more than half of total production costs in many commercial facilities.

Energy Efficiency Emerges as a Key Determinant of Profitability

Energy availability and pricing are increasingly influencing global competitiveness within the microalgae industry.

Cultivation, harvesting, drying, extraction, and purification all require substantial energy inputs. Facilities operating in regions with affordable and reliable industrial power infrastructure often achieve significantly lower production costs than competitors facing higher utility expenses.

Producers are increasingly investing in:

• Heat recovery systems

• Process automation platforms

• Advanced aeration technologies

• Renewable energy integration

• Carbon utilization systems

These investments help reduce operating expenses while improving sustainability performance and environmental credentials.

Countries with access to low-cost electricity, industrial carbon dioxide sources, and favorable renewable energy infrastructure are strengthening their positions as preferred locations for commercial microalgae production.

Regulatory Frameworks Continue to Shape Commercial Adoption

Beyond production economics, regulatory acceptance remains a critical factor determining which microalgae ingredients achieve commercial success.

Food, nutraceutical, cosmetic, and feed applications each require different regulatory pathways that influence development timelines and commercialization costs.

Manufacturers must increasingly navigate requirements related to:

• Food safety validation

• Novel food approvals

• Ingredient traceability

• Manufacturing standards

• Product labeling compliance

Only a relatively small number of microalgae species currently possess broad regulatory acceptance across major global markets.

This regulatory concentration creates substantial advantages for established species such as Spirulina, Chlorella, Dunaliella, Haematococcus, and Schizochytrium while limiting commercialization opportunities for many emerging strains.

Leading Production Nations Strengthen Global Market Leadership

A small group of countries continues to dominate commercial microalgae ingredient production due to favorable combinations of infrastructure, climate, investment capital, and regulatory support.

The United States maintains leadership in high-value ingredient production, particularly in omega-3 oils, astaxanthin, and specialty nutraceutical applications. Advanced processing infrastructure and established regulatory pathways continue to support industry growth.

China remains the largest producer of large-volume microalgae biomass, benefiting from extensive cultivation capacity, established supply chains, and cost-efficient manufacturing operations.

India has developed a strong position in Spirulina production through year-round cultivation conditions, competitive labor costs, and expanding domestic nutrition markets.

Meanwhile, European producers increasingly focus on premium segments where quality assurance, sustainability certification, and traceability support higher value realization.

Vertical Integration Becomes the Preferred Commercial Model

As the industry matures, vertically integrated business models are increasingly outperforming standalone biomass production strategies.

Companies that control multiple stages of the value chain are better positioned to capture value while reducing operational risks.

Integrated producers benefit from:

• Improved quality control

• Lower logistics costs

• Stronger customer relationships

• Enhanced production planning

• Greater pricing stability

Many leading companies now combine cultivation, extraction, ingredient manufacturing, and end-market partnerships within a single operating framework.

Sustainability and Resource Efficiency Support Long-Term Growth

One of the most attractive characteristics of microalgae remains its ability to generate high-value nutritional compounds using significantly fewer natural resources than many conventional agricultural systems.

Microalgae cultivation offers advantages including:

• Minimal land requirements

• Reduced freshwater demand

• Carbon utilization opportunities

• High productivity rates

• Flexible production environments

These sustainability benefits continue to attract interest from food manufacturers, investors, and policymakers seeking alternative ingredient solutions capable of supporting future global nutrition needs.

However, achieving economic sustainability remains equally important.

The industry’s long-term success will depend on balancing environmental benefits with commercially viable production models capable of competing against conventional ingredients on both performance and cost.

Future Outlook

The future of the microalgae industry will be increasingly shaped by cultivation efficiency, harvesting economics, regulatory acceptance, and integrated value-chain development. While scientific innovation continues to expand the range of potential applications, commercial success will depend primarily on the industry’s ability to reduce production costs and improve operational performance at scale.

Explore More Related Studies Published by FMI Research:

Omega-3 Ingredients Market is segmented by Source (Fish Oil, Algae Oil, Krill Oil, and Others), Application (Food and Beverage, Dietary Supplements, Pharmaceuticals, Infant Nutrition, and Animal Nutrition), and Region. Forecast for 2025 to 2035.

Algae Products Market is segmented by Product Type (Proteins, Pigments, Lipids, Hydrocolloids, and Others), Source, Application, and Region. Forecast for 2025 to 2035.

About Future Market Insights (FMI)

Future Market Insights, Inc. (FMI) is an ESOMAR-certified, ISO 9001:2015 market research and consulting organization, trusted by Fortune 500 clients and global enterprises. With operations in the U.S., UK, India, and Dubai, FMI provides data-backed insights and strategic intelligence across 30+ industries and 1200 markets worldwide.

Contact Us:

Future Market Insights Inc.

Christiana Corporate, 200 Continental Drive,

Suite 401, Newark, Delaware – 19713, USA

T: +1-347-918-3531

Why FMI: https://www.futuremarketinsights.com/why-fmi

For Sales Enquiries: sales@futuremarketinsights.com

Website: https://www.futuremarketinsights.com