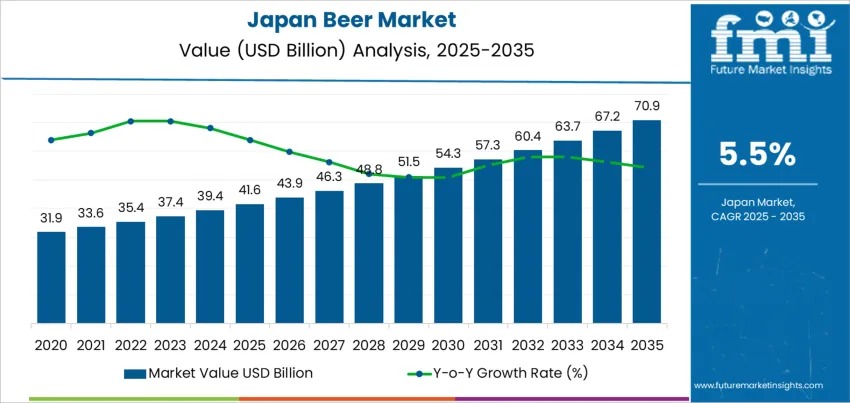

The Japan beer industry is experiencing a renewed phase of value-led growth, with demand valued at USD 41.6 billion in 2025 and projected to climb to USD 70.9 billion by 2035, registering a 5.5% CAGR. Market expansion is driven by premium-beer adoption, wider flavor portfolios, and brewery investments in production innovation. Strong tourism recovery, increased on-trade footfall, and rising interest in specialty beers are also fueling momentum across the country.

Growing adoption of returnable packaging, supply-chain optimization, and redesigned formats is shaping procurement strategies across bars, izakaya venues, retail chains, and hospitality networks. Major breweries continue to scale high-output manufacturing supported by advanced fermentation controls, yeast optimization, and aroma hop development to ensure consistent flavor quality for a diverse consumer base.

Explore trends before investing – request a sample report today! https://www.futuremarketinsights.com/reports/sample/rep-gb-29320

Premiumization, Seasonal Releases, and Diversified Taste Preferences Strengthen Consumption

Lager remains the leading product category due to its clean profile, food-pairing versatility, and dominance in convenience stores and restaurants. Japanese brewers are also expanding reduced-alcohol and low-malt lagers to align with calorie-conscious consumption patterns.

Urban clusters—including Kyushu & Okinawa, Kanto, and Kansai—exhibit the highest demand, supported by dense dining districts, convenience-store penetration, and robust cold-chain infrastructure for both canned and draught formats. Key players such as Asahi, Kirin, Suntory, and Sapporo continue to diversify offerings across mainstream, seasonal, and craft-inspired categories.

Quick Industry Stats (Japan Beer Industry, 2025–2035)

- Market Value 2025: USD 41.6 billion

- Forecast Value 2035: USD 70.9 billion

- CAGR: 5.5%

- Top Product: Lager

- High-Growth Regions: Kyushu & Okinawa, Kanto, Kansai

Value-Led Expansion Amid Market Maturity

Japan’s beer category remains structurally mature, shaped by decades of high per-capita consumption and entrenched brand loyalty. However, selective growth segments—premium craft beers, low-alcohol variants, and seasonal products—are sustaining uplift within an otherwise stable base.

Shifts in demographic patterns, including an aging population and lifestyle moderation among younger consumers, limit volume growth. Yet, demand remains intact due to:

- expanded craft experimentation,

- home-drinking trends supported by e-commerce,

- tourism-driven hospitality consumption,

- consistent on-premise popularity in business districts.

Innovation prevents deeper category stagnation, ensuring steady market value expansion even without major volume increases.

Why Demand Is Shifting

Japanese consumers increasingly explore specialty flavors, regional brews, and seasonal varieties promoted by convenience stores and supermarkets. Restaurant and nightlife venues continue to anchor beer consumption, especially in metropolitan areas known for after-work dining.

Demand is also shaped by:

- Rise of low-malt and low-calorie options appealing to health-conscious adults

- Packaging innovations such as compact cans and recyclable formats

- Tourism expansion supporting hospitality-linked sales

- Shift toward home consumption, accelerating canned beer demand

Constraints include taxation structures, rising input costs, and preference shifts toward cocktails, chuhai, and nonalcoholic beverages among younger audiences.

Leading Market Segments

By Product Type

- Lager – 45% share: Mass accessibility and strong brand loyalty

- Ale – 30%: Driven by craft styles (IPA, wheat ale)

- Stout – 15%: Seasonal and niche popularity

- Others – 10%: Fruit beers, low-alcohol variants

By Packaging Format

- Bottles – 42%: Strong restaurant and premium positioning

- Cans – 35%: Portability and convenience-store dominance

- Glass Packaging – 13%: Used for premium craft releases

- Others – 10%: Kegs, growlers, specialty formats

By Production Model

- Macro-breweries – 55%: Scale, reach, and quality consistency

- Craft breweries – 25%: Regional identity and diversified flavors

- Microbreweries – 15%: Localized artisanal offerings

- Others – 5%

Key Market Drivers

- Rising premium and craft beer interest

- Seasonal consumption during festivals and gatherings

- Convenience retail dominance

- Tourism recovery and on-premise revival

Market Restraints

- Aging population reducing frequent drinker base

- Health-driven lifestyle moderation

- Taxation influencing malt-content preferences

Emerging Trends

- Growth of non-alcoholic and low-malt variants

- Canned craft beers gaining national reach

- E-commerce accelerating home consumption

- Frequent limited-edition collaborations

Regional Outlook (CAGR 2025–2035)

- Kyushu & Okinawa: 6.8%

- Kanto: 6.3%

- Kansai: 5.5%

- Chubu: 4.9%

- Tohoku: 4.3%

- Rest of Japan: 4.1%

Competitive Landscape

The Japan beer market is dominated by four major players with broad national distribution:

- Asahi Group Holdings (40% share)

- Kirin Brewery Company

- Suntory Holdings

- Sapporo Breweries

Competition is shaped by brand identity, consistent flavour delivery, seasonal innovations, retail presence, and on-trade strength. Consumer loyalty remains high for domestic beer brands, reinforcing stable, repeat-purchase patterns across generations.