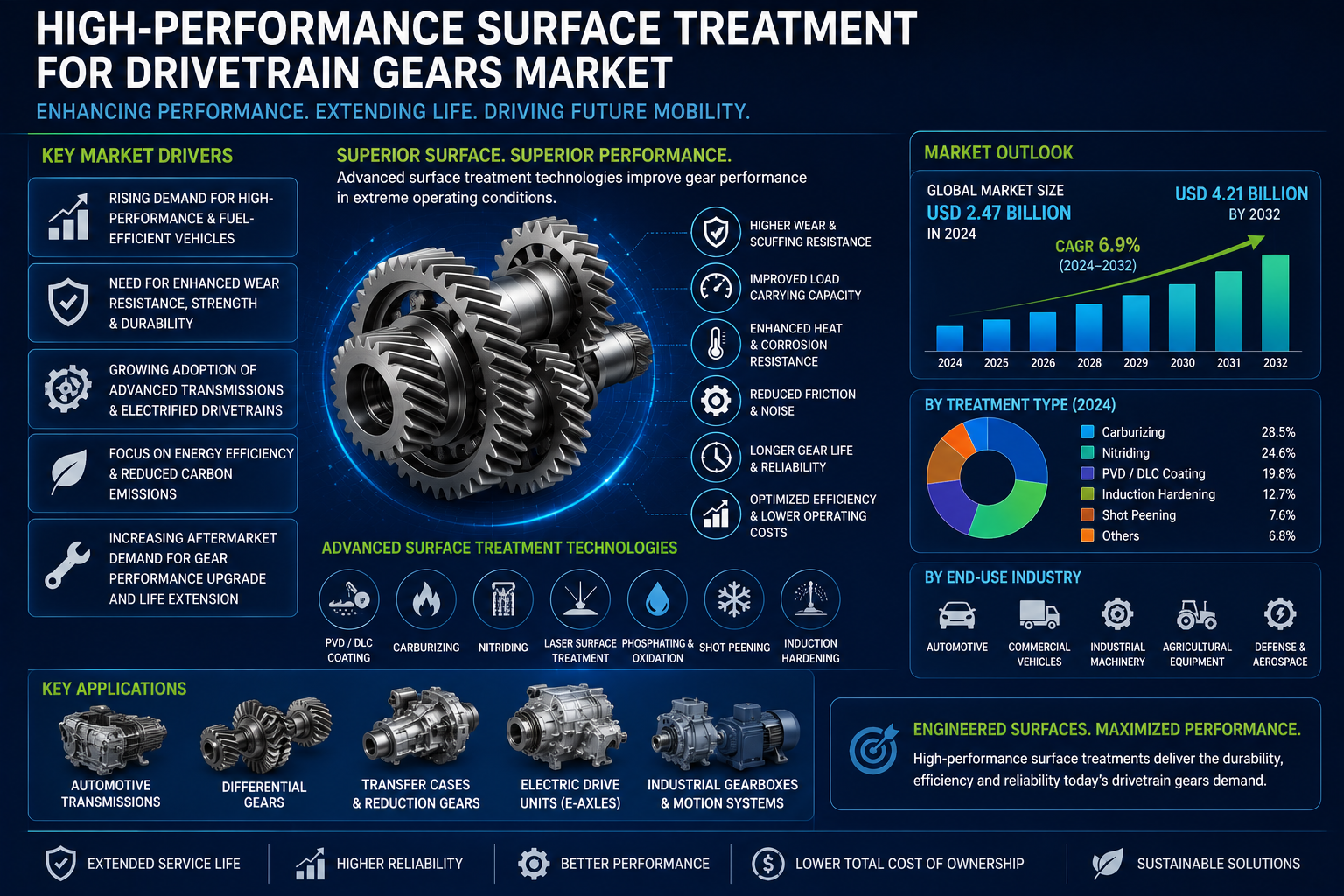

The global High-Performance Surface Treatment for Drivetrain Gears Market is entering a phase of sustained growth as automotive manufacturers increasingly focus on gear durability, efficiency, and performance across conventional and electric vehicle platforms. Valued at USD 942.8 million in 2025, the market is projected to grow from USD 997.4 million in 2026 to USD 1,752.8 million by 2036, registering a CAGR of 5.8% during the forecast period.

The market’s expansion is being driven by rising demand for advanced drivetrain systems, increasing adoption of electric vehicles, and the need for enhanced wear resistance in transmission, differential, and e-axle gears. As drivetrain architectures become more compact and torque-intensive, surface treatment technologies are evolving from a traditional manufacturing step into a critical performance and reliability enabler.

Surface Engineering Becomes Essential for Modern Drivetrains

Surface treatment technologies play a vital role in improving gear strength, reducing friction, enhancing fatigue resistance, and extending operational life. Modern drivetrain gears are subjected to increasingly demanding operating conditions, particularly in electric vehicles where instant torque delivery places higher stress on gear teeth and contact surfaces.

Manufacturers are therefore investing in advanced treatment processes such as carburizing, nitriding, induction hardening, physical vapor deposition (PVD) coatings, and shot peening. These processes improve surface hardness while maintaining core toughness, enabling gears to withstand continuous high-load conditions without premature wear.

As automakers strive to improve drivetrain efficiency and reduce maintenance requirements, treated gears are becoming a standard requirement across both internal combustion engine and electrified vehicle platforms.

Electric Vehicle Growth Reshapes Treatment Requirements

The rapid growth of electric mobility is creating new opportunities for high-performance surface treatment providers. Unlike conventional transmissions, electric drive units often operate at higher rotational speeds and generate unique wear patterns that require enhanced surface protection.

Compact e-axle systems demand tighter manufacturing tolerances and lower friction coefficients to maximize efficiency and reduce operational noise. As a result, gear manufacturers are increasingly adopting advanced coating technologies and precision-controlled heat treatment processes to meet evolving performance expectations.

Industry experts note that drivetrain suppliers are paying closer attention to distortion control, case depth consistency, and post-treatment inspection as these factors directly impact gear meshing quality and long-term durability in electric powertrains.

Original Equipment Segment Maintains Market Leadership

Original equipment (OE) applications are expected to dominate the market throughout the forecast period, accounting for 68.1% of total market revenue in 2026.

This leadership position reflects the growing trend of gear suppliers completing surface treatment processes before components reach vehicle assembly lines. Automakers increasingly prefer pre-treated drivetrain components that meet strict quality specifications and durability targets.

The integration of advanced treatment technologies during the manufacturing phase helps reduce warranty risks, improve drivetrain performance, and ensure consistent product quality across high-volume production programs.

As vehicle manufacturers continue to prioritize reliability and efficiency, OE demand is expected to remain the primary revenue contributor for surface treatment providers worldwide.

Alloy Steel Remains Preferred Material Choice

Alloy steel is projected to account for 52.5% of the market in 2026, maintaining its position as the most widely used material for drivetrain gear manufacturing.

The popularity of alloy steel stems from its compatibility with established surface treatment technologies such as carburizing and nitriding. These processes allow manufacturers to achieve the combination of surface hardness and internal toughness required for demanding drivetrain applications.

Advanced alloy compositions also provide improved fatigue strength and wear resistance, making them particularly suitable for high-performance transmissions, differentials, final drive gears, and e-axle systems.

While alternative materials continue to emerge, alloy steel remains the preferred option due to its proven performance, cost efficiency, and compatibility with large-scale automotive manufacturing processes.

Passenger Vehicles Drive Market Demand

Passenger cars are expected to account for 46.8% of global demand during the forecast period, supported by their substantial production volumes and widespread use of treated drivetrain components.

Every passenger vehicle relies on multiple gears within transmission and differential systems, creating a significant volume requirement for surface treatment services. Rising global vehicle production, particularly in Asia-Pacific markets, is further strengthening demand.

The growing adoption of hybrid and battery electric vehicles is also increasing the need for precision-treated gears capable of handling higher torque loads while maintaining quiet operation and long service life.

Asia-Pacific Emerges as Growth Hub

Asia-Pacific continues to represent the most dynamic region for the high-performance surface treatment for drivetrain gears market.

China is expected to lead global growth with a CAGR of 7.4% through 2036. The country’s dominant automotive manufacturing base, expanding electric vehicle production, and strong investment in advanced manufacturing technologies are driving substantial demand for gear treatment services.

China’s rapidly growing e-mobility sector is particularly important, as electric drivetrain systems require specialized surface treatment processes to meet durability and efficiency requirements.

India is projected to follow closely with a CAGR of 7.0% during the forecast period. Rising passenger vehicle production, expanding automotive component manufacturing, and increasing investment in transmission and drivetrain technologies are supporting market growth.

Local gear manufacturers are increasingly upgrading treatment capabilities to meet the quality standards required by both domestic automakers and export markets.

Technology Innovation Strengthens Competitive Landscape

Competition within the market is increasingly focused on process consistency, treatment quality, and technological innovation.

Leading companies are investing in advanced furnace technologies, automated inspection systems, and environmentally efficient treatment processes. Low-pressure carburizing, plasma nitriding, and advanced PVD coating technologies are gaining popularity as manufacturers seek improved performance while reducing energy consumption and emissions.

Companies capable of demonstrating repeatable case depth control, minimal distortion, and superior wear performance are expected to secure long-term contracts with major drivetrain manufacturers.

Industry leaders including Bodycote, Oerlikon Balzers, AICHELIN Group, and SECO/WARWICK continue to expand their capabilities through technology upgrades and international service networks, strengthening their positions in a highly competitive market.

Future Outlook

The High-Performance Surface Treatment for Drivetrain Gears Market is expected to remain on a strong growth trajectory through 2036 as automakers place greater emphasis on drivetrain reliability, efficiency, and durability. The transition toward electric mobility, increasing vehicle production, and growing demand for advanced gear performance will continue to create opportunities for specialized surface treatment providers.

As drivetrain systems become more sophisticated and performance expectations rise, surface treatment technologies will play an increasingly critical role in ensuring the longevity and efficiency of next-generation automotive powertrains.

Browse more industry reports

Automotive Radar Sensors Market – https://www.openpr.com/news/4533979/automotive-radar-sensors-market-to-reach-usd-30-8-billion

Automotive Glass Market – https://www.openpr.com/news/4533984/automotive-glass-market-to-reach-usd-40-8-billion-by-2036-driven

Permanent Magnet Motor Market – https://www.openpr.com/news/4533987/permanent-magnet-motor-market-to-reach-usd-161-2-billion-by-2036