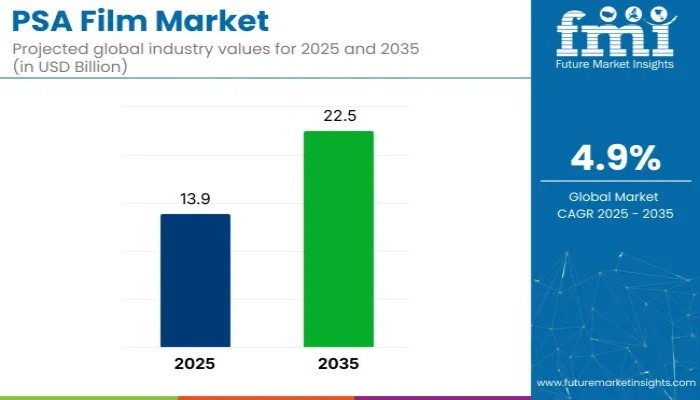

The global Pressure-Sensitive Adhesive (PSA) Film Market is set for a decade of sustained expansion, rising from USD 13.9 billion in 2025 to USD 22.5 billion by 2035, at a CAGR of 4.9%. As industries accelerate their shift toward lightweight, solvent-free, and high-efficiency bonding solutions, PSA films are emerging as a preferred choice for packaging, automotive, consumer electronics, and healthcare.

With packaging accounting for the leading 30% share and the Asia Pacific region—especially India and China—positioned as key growth hubs, the industry is evolving toward high-performance, sustainable, and application-specific film solutions.

Subscribe for Year-Round Insights → Stay ahead with quarterly and annual data updates – https://www.futuremarketinsights.com/reports/sample/rep-gb-22329

A Market on the Rise: Quick Stats

- 2025 Market Value: USD 13.9 billion

- 2035 Forecast Value: USD 22.5 billion

- CAGR (2025–2035): 4.9%

- Top Segment: Packaging (30% share)

- Key Growth Region: Asia Pacific

- Leading Players: 3M, Tesa SE, Flexcon Company, Inc.

Packaging Leads the Global Adoption Curve

The packaging industry continues to be the largest consumer of PSA films, driven by rapid e-commerce expansion, cold-chain logistics, and demand for tamper-evident, functional packaging. PSA films’ versatility in labels, protective wraps, sealing applications, and logistics identification is accelerating their adoption.

Consumer and brand preferences are also shifting toward recyclable and low-VOC film structures, prompting manufacturers to invest in bio-based and waterborne adhesive chemistries.

Automotive & Electronics Push PSA Films into High-Value Applications

Advanced PSA films—particularly silicone- and acrylic-based variants—are now integral to automotive interiors, electronics displays, and EV insulation layers. These films offer vibration damping, optical clarity, heat resistance, and dielectric protection, making them indispensable across:

- EV battery pack insulation

- Circuit and PCB protection

- High-resolution display lamination

- Surface protection during vehicle assembly

The global transition to electric mobility and connected devices is expected to significantly boost demand for high-performance PSA films.

Asia Pacific Dominates Volume, While North America and Europe Shift to Premium Films

The Asia Pacific region commands the largest share owing to its expanding packaging, electronics, and automotive manufacturing clusters. India and China alone are projected to grow at 6.1% and 5.3% CAGR, respectively, from 2025 to 2035.

Meanwhile, North America and Western Europe are witnessing rising use of specialty PSA films in medical devices, aerospace coatings, and high-end electronics—segments characterized by low tolerance for defects, demanding specifications, and higher margins.

Innovation Spotlight: Arkema’s 2023 Breakthrough

In February 2023, Arkema introduced a comprehensive portfolio of PSA solutions spanning hot melt, waterborne, UV, and specialty acrylic technologies—a move that underscores industry-wide commitment toward performance, sustainability, and material versatility. Such innovations are reshaping film performance parameters across emerging and traditional applications.

Market Share Across Parent Industries

PSA films hold specialized but critical market positions:

- Adhesive Films: 10–12%

- Packaging: 3–5%

- Automotive: 4–6%

- Textiles: 2–3%

- Consumer Electronics: 3–4%

These films are increasingly being adopted for fabric bonding, window tinting, electronics display protection, and smart-device components, illustrating their cross-sector versatility.

Top Investment Segment: BOPP Films Capture 40% of Packing Material Demand

BOPP (Biaxially Oriented Polypropylene) films are on track to dominate with a 40% share in 2025 due to:

- High transparency and tensile strength

- Moisture and chemical resistance

- Cost-effective processing

- Recyclability and lightweight nature

The increased global focus on flexible, sustainable packaging reinforces BOPP’s upward trajectory.

Key Market Dynamics: Drivers & Challenges

Growth Accelerators

- Rapid adoption in automotive, construction, and electronics

- Increased demand for insulation, masking, and protective layers

- Automation in production lines requiring reliable adhesive performance

Constraints

- Raw material volatility (PET resin, rubber, acrylics)

- Global supply chain fluctuations and trade restrictions

- Environmental compliance pressures, especially for solvent-based adhesive systems

Country-Level Growth Outlook (CAGR 2025–2035)

| Country | CAGR |

| India | 6.1% |

| China | 5.3% |

| United States | 3.9% |

| United Kingdom | 3.6% |

| Japan | 3.2% |

India leads with a 25% growth premium, supported by manufacturing expansion and PLI-backed electronics assembly growth. China follows closely, driven by the rising need for high-performance, electronics-grade PSA films.

Regional Highlights

United States

CAGR: 3.9%

Growth supported by EV battery insulation, aerospace-grade surface protection, and sustainable packaging solutions.

United Kingdom

CAGR: 3.6%

Net-zero construction, EV supply chain expansion, and antimicrobial film demand drive usage.

China

CAGR: 5.3%

Rapid industrial upgrades and circular-economy initiatives fuel adoption of recyclable PSA carriers.

India

CAGR: 6.1%

Strongest global growth; e-commerce logistics, construction, and consumer electronics propel demand.

Japan

CAGR: 3.2%

Specialization in optical-grade, microelectronics, and medical films secures steady demand.

Competitive Landscape

Dominant Players:

- 3M

- Tesa SE

- Flexcon Company, Inc.

Key Players:

- NEION Film Coatings Corporation

- Nanolap Technologies LLC

- Precision-polishing

Emerging Players:

- DermaMed Coatings Company, LLC

Players are investing heavily in bio-based adhesives, optical films, EV thermal tapes, and sustainable linerless label systems to differentiate in a competitive market.

Recent Industry Developments

- Henkel (2023): Introduced eco-friendly PSA solutions improving label durability and adhesion.

- PSTC Tape Week 2025 (Illinois): Highlighted advancements in cast and calendered vinyl PSA technologies for packaging, medical, automotive, and graphics applications.

Why FMI: https://www.futuremarketinsights.com/why-fmi

About Future Market Insights (FMI)

Future Market Insights, Inc. (FMI) is an ESOMAR-certified, ISO 9001:2015 market research and consulting organization, trusted by Fortune 500 clients and global enterprises. With operations in the U.S., UK, India, and Dubai, FMI provides data-backed insights and strategic intelligence across 30+ industries and 1200 markets worldwide.

Contact Us:

Future Market Insights Inc.

Christiana Corporate, 200 Continental Drive,

Suite 401, Newark, Delaware – 19713, USA

T: +1-347-918-3531

For Sales Enquiries: sales@futuremarketinsights.com

Website: https://www.futuremarketinsights.com

LinkedIn| Twitter| Blogs | YouTube