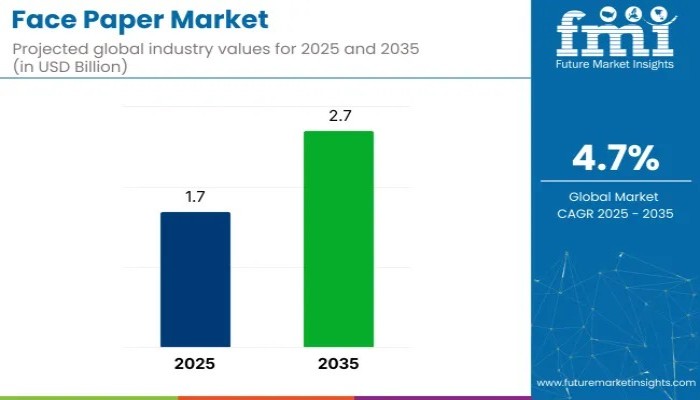

The global face paper market is projected to grow from USD 1.7 billion to USD 2.7 billion, registering a 4.7% CAGR from 2025 to 2035. This steady rise is largely driven by the expanding use of pressure-sensitive labels across retail, logistics, healthcare, pharmaceuticals, personal care, and e-commerce packaging. As industries prioritize traceability, regulatory compliance, and premium branding, demand for durable, printable, and high-performance face papers continues to surge.

Quick Stats of the Face Paper Market

- Market Size (2025): USD 1.7 billion

- Forecast Size (2035): USD 2.7 billion

- CAGR (2025–2035): 4.7%

- Top Product (2025): Coated Paper (61% share)

- Leading Application: Tags & Stickers (41% share)

- Top Growth Regions: Germany & China (5.7% CAGR)

- Leading Manufacturer: UPM Adhesive Materials (18% industry share)

Subscribe for Year-Round Insights → Stay ahead with quarterly and annual data updates – https://www.futuremarketinsights.com/reports/sample/rep-gb-22399

Face Paper Market Overview

Face paper plays a critical role in delivering sharp print quality, durability, and functional label performance. With the rapid adoption of digital and flexographic printing, brands and converters now demand substrates capable of supporting high-resolution, fast-drying, and eco-friendly applications.

Although often associated with labeling, the broader category of facial papers—including tissues, wipes, and napkins—also contributes significantly to global pulp consumption. Together, these segments reflect a complex supply chain where technological advancement, consumer preferences, sustainability trends, and fiber availability shape growth patterns.

Industry leaders like Kimberly-Clark highlight a shift toward wellness features, plant-based materials, and green packaging, reflecting an industry-wide pivot toward sustainable value creation.

Top Investment Segments Driving Market Expansion

Coated Grades Lead Material Preference (61% Share)

Coated face papers dominate due to their clarity, smoothness, and ink retention—essential for high-performance pressure-sensitive labels. Companies such as UPM Raflatac, Avery Dennison, and Mondi Group continue expanding investments into coated paper technologies.

Key Highlights:

- Enhanced moisture resistance

- Superior printability for high-speed automated presses

- Industrial-scale quality assurance from global suppliers

Tags & Stickers Shape Everyday Labeling (41% Share)

Tags and stickers remain indispensable in retail, FMCG, e-commerce, and logistics. Manufacturers including LINTEC, Flexcon, and Herma GmbH are developing fast-drying and high-tack labels to meet rising SKU complexity.

Market Drivers:

- High-volume use in pricing, inventory, and promotional labels

- Performance stability in cold-chain and outdoor conditions

- Expanding role in apparel, batch labeling, and product-level marketing

Permanent Adhesive Solutions Dominate Industrial Labeling (54% Share)

Permanent adhesives are crucial for long-term labeling across chemicals, logistics, and consumer goods. Leading suppliers—3M, Henkel, Avery Dennison—are engineering new peel-resistant, multi-surface adhesion technologies.

Advantages:

- Compliance-grade labels for drums and cartons

- Retention of critical data across transit cycles

- Strong adoption in warehousing, regulatory, and retail sectors

Glossy Finishes Boost Branding and Shelf Visibility (47% Share)

Glossy face papers are gaining popularity in luxury retail, cosmetics, and premium packaging. Suppliers like Sappi, Arconvert, and Fedrigoni optimize these substrates for digital printing and high-clarity branding.

Drivers:

- Enhanced color depth and contrast

- Surface protection in high-touch environments

- Growing demand in decorative and specialty labels

Packaging Sector Sets Benchmark for Adoption (33% Share)

From FMCG to pharmaceuticals, face paper is essential for identity, safety warnings, use-by dates, and traceability. Firms such as Wausau Coated and Nippon Paper are expanding durable, scannable, tamper-evident face paper solutions for global packaging lines.

Market Dynamics: Innovation, Regulation & Sustainable Growth

Strategic Innovation & Expansion

- UPM Raflatac expanded FSC-certified face papers across Europe and Asia

- Avery Dennison launched wash-off labels to support PET recycling

- Sappi partnered with Xeikon on digital-optimized materials

- Mondi modernized its German uncoated paper facility

Application-Focused Product Development

- Lintec introduced oil-resistant papers for foodservice packaging

- APAC brands adopted matte finishes for pharmaceutical labeling

- Textured papers gained traction in Europe’s wine and spirits segment

Cost Pressures & Material Substitution

- Pulp volatility caused 9–13% cost fluctuations

- Rise of synthetic alternatives like BOPP and PET-based labels

- Regulatory delays impacted adhesive formulations

Global Demand Distribution (CAGR 2025–2035)

| Country | CAGR |

| China | 5.7% |

| Germany | 5.7% |

| USA | 5.1% |

| Canada | 5.1% |

| India | 4.7% |

Growth is highest in Germany and China due to surging industrial labeling and advanced retail packaging systems.

Regional Highlights

India:

- 4.7% CAGR driven by vernacular packaging and high SKU turnover

- Strong adoption among Ayurveda, grooming, and cosmetic brands

- 22% of 2024 volumes came from personal hygiene and OTC labeling

China:

- 5.7% CAGR propelled by logistics automation and QR-enabled labels

- Thermal-responsive substrate demand up 23% YoY

- Jiangsu and Zhejiang remain major export hubs

USA:

- 5.1% CAGR with strong growth in medical and prescription labeling

- 67% of pharma packaging uses acid-free face paper

- QR-enabled labels applied to 63% of outbound parcels

Germany:

- Industrial goods and auto parts labeling driving demand

- Waterproof adhesives up 28% YoY for cold-route freight

Canada:

- Bilingual packaging regulations lifting specialty demand

- Cannabis labeling volumes rose 31% in 2024

Competitive Landscape: Leadership & Emerging Innovators

Leading Player: UPM Adhesive Materials (18% Share)

UPM continues to shape the industry through high-performance product launches and strategic acquisitions, including a new specialty paper manufacturer in early 2024.

Other Major Players:

- Delfort Group – Lightweight, eco-efficient specialty papers

- Emax Label Solution – Cost-effective technologies for SMEs

- Whitlam Group – Strong distribution-driven expansion

Emerging players are entering with niche innovations, although regulatory hurdles and supply chain complexity remain barriers.

Recent Industry Developments

- UPM Adhesive Materials acquired a specialty paper manufacturer (Q1 2024)

- Delfort Group launched lightweight face papers cutting material use by 15%

- New entrants focus on digital-ready, recyclable, and hybrid-print substrates

Why FMI: https://www.futuremarketinsights.com/why-fmi

About Future Market Insights (FMI)

Future Market Insights, Inc. (FMI) is an ESOMAR-certified, ISO 9001:2015 market research and consulting organization, trusted by Fortune 500 clients and global enterprises. With operations in the U.S., UK, India, and Dubai, FMI provides data-backed insights and strategic intelligence across 30+ industries and 1200 markets worldwide.

Contact Us:

Future Market Insights Inc.

Christiana Corporate, 200 Continental Drive,

Suite 401, Newark, Delaware – 19713, USA

T: +1-347-918-3531

For Sales Enquiries: sales@futuremarketinsights.com

Website: https://www.futuremarketinsights.com

LinkedIn| Twitter| Blogs | YouTube