The global oilfield stimulation chemicals market is entering a transformative growth phase, poised to reach USD 11.3 billion by 2035 from an estimated USD 6.0 billion in 2025. Registering a CAGR of 6.5% between 2025 and 2035, the market’s momentum is underpinned by expanding exploration and production (E&P) operations, particularly across unconventional and mature reservoirs. As global energy demand continues to climb, the role of stimulation chemicals in optimizing well productivity and extending field lifecycles has become indispensable.

Oilfield stimulation chemicals are vital for enhancing the recovery efficiency of hydrocarbons from reservoirs that have become less productive over time. These specialized chemical formulations—including acids, surfactants, friction reducers, corrosion inhibitors, and gelling agents—enable better flow of hydrocarbons and mitigate operational challenges like scaling, corrosion, and formation damage. The rise of data-driven and environmentally responsible extraction processes is further redefining how these chemicals are deployed in both onshore and offshore operations.

Drivers Powering Market Expansion

The core growth driver of the oilfield stimulation chemicals market lies in the accelerating push for enhanced oil recovery (EOR) and the optimization of unconventional resources such as shale gas and tight oil formations. With easily accessible oil reserves diminishing, operators are relying more heavily on stimulation technologies to maintain consistent production rates.

Technological advancements in chemical formulations have led to improved performance, greater efficiency, and lower environmental impact. Manufacturers are focusing on controlled acid systems, biodegradable surfactants, and innovative viscosifiers that reduce water use and operational risks. In parallel, digital monitoring tools are allowing oilfield service companies to precisely manage chemical dosage and measure stimulation effectiveness in real-time, ensuring higher yields at reduced costs.

Government initiatives emphasizing sustainable oilfield operations are further pushing chemical innovation. Regulatory frameworks across North America and Europe are driving the shift toward safer and more environmentally compatible solutions, while developing economies in Asia-Pacific are increasing spending on oilfield infrastructure to meet surging domestic energy demand.

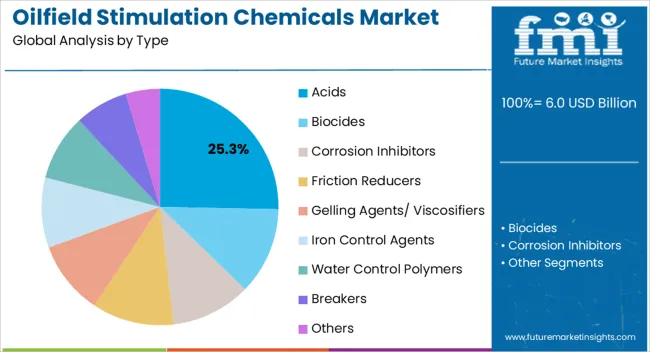

Acids Segment Retains Dominance

Among all chemical types, the acids segment remains the cornerstone of the oilfield stimulation chemicals market, accounting for an estimated 25.3% revenue share in 2025. Acids play a pivotal role in dissolving formation blockages, cleaning fractures, and improving hydrocarbon flow. The most commonly used variants—hydrochloric, formic, and organic acids—are being refined through modern formulations that enhance corrosion resistance and reaction control.

As E&P activities move into deeper and more complex geological formations, the need for effective acid stimulation grows. Operators in the Middle East, North America, and China are increasingly integrating acid-based treatments with advanced downhole delivery systems and coiled tubing techniques to improve penetration and uniformity. For new entrants and chemical innovators, this segment presents significant potential to develop smart acid systems that minimize environmental footprint while maintaining high efficiency.

Hydraulic Fracturing Remains the Leading Application

Hydraulic fracturing continues to be the most influential application segment, projected to command a 40.2% market share in 2025. This dominance stems from the extensive use of stimulation chemicals in shale and tight formations across North America, where hydraulic fracturing is a critical driver of oil and gas output. Chemicals such as surfactants, friction reducers, and gelling agents are crucial in maintaining fluid viscosity, proppant transport, and formation integrity.

The expansion of shale gas operations in the United States and Canada, alongside emerging exploration in China and India, is bolstering the global demand for these advanced chemical systems. Producers are simultaneously investing in sustainable formulations that reduce water use and mitigate environmental impact. For instance, bio-based friction reducers and non-toxic scale inhibitors are becoming central to compliance with tightening regulations in OECD markets.

Global Market Landscape and Regional Outlook

Regionally, North America remains the largest market for oilfield stimulation chemicals, with strong activity in the United States and Canada’s shale basins. However, the Asia-Pacific region is rapidly catching up, led by China’s 8.8% CAGR and India’s 8.1% CAGR forecast through 2035. The region’s emphasis on energy independence, combined with its massive untapped hydrocarbon reserves, continues to attract investment in well stimulation projects.

In Europe, countries such as Germany and France are maintaining steady growth rates of 7.5% and 6.8%, respectively, driven by technology adoption in mature oilfields and offshore recovery operations. The UK, with a projected CAGR of 6.2%, continues to modernize its North Sea operations through eco-friendly chemical solutions, while the USA remains a mature but vital market with a consistent 5.5% CAGR. Brazil, though growing at a slower 4.9%, continues to invest in offshore stimulation projects that sustain its oil output in deepwater fields.

Technological Advancements Reshaping Operations

Innovations in formulation science and process engineering are revolutionizing oilfield stimulation chemistry. Leading manufacturers such as BASF SE, Dow Chemical Company, and Clariant AG are pioneering environmentally responsible alternatives to traditional formulations, developing biodegradable surfactants and reduced-toxicity acids that maintain performance while ensuring regulatory compliance.

At the same time, major oilfield service companies including Baker Hughes, Schlumberger, and Halliburton are integrating smart chemical delivery systems with digital monitoring platforms. This fusion of chemistry and analytics is enabling precise, on-demand stimulation that enhances production rates and extends well life.

New entrants and mid-tier players are also making their mark. Firms like Kemira Oyj, Stepan Company, and Croda International Plc are focusing on niche chemical applications such as low-foaming surfactants and corrosion inhibitors tailored for specific reservoir conditions. Regional manufacturers in Asia and the Middle East are increasingly forming joint ventures with global giants to localize production and strengthen distribution networks, thereby reducing logistical costs and improving supply security.

Purchase this Report for USD 5,000 Only | Get an Exclusive Discount Instantly! https://www.futuremarketinsights.com/checkout/2687

Everything You Need—within Your Budget. Request a Special Price Now! https://www.futuremarketinsights.com/reports/sample/rep-gb-2687

Competitive Landscape and Strategic Developments

The oilfield stimulation chemicals market remains competitive, with both established and emerging players emphasizing innovation and regional expansion. Companies like Albemarle Corporation, Ashland Global Holdings, and Solvay S.A. are investing in R&D for new polymer-based viscosifiers and iron control agents designed for complex well environments. Meanwhile, Ecolab Inc. and Chevron Phillips Chemical Company are advancing their sustainability portfolios, introducing eco-compliant solutions to meet evolving regulatory standards.

A notable industry development occurred in early 2025, when several major chemical producers announced cross-industry collaborations to develop closed-loop chemical recycling for oilfield applications. These initiatives aim to reduce waste, lower operational costs, and support circular economy principles within the sector.

The continued globalization of the oilfield services supply chain is fostering the growth of new entrants, particularly in Asia-Pacific and the Middle East. These companies are leveraging regional feedstock availability and favorable government policies to establish local manufacturing bases, challenging established Western players with cost-competitive and adaptable product lines.

About Future Market Insights (FMI)

Future Market Insights, Inc. (ESOMAR certified, recipient of the Stevie Award, and a member of the Greater New York Chamber of Commerce) offers profound insights into the driving factors that are boosting demand in the market. FMI stands as the leading global provider of market intelligence, advisory services, consulting, and events for the Packaging, Food and Beverage, Consumer Technology, Healthcare, Industrial, and Chemicals markets. With a vast team of over 400 analysts worldwide, FMI provides global, regional, and local expertise on diverse domains and industry trends across more than 110 countries.

Contact Us:

Future Market Insights Inc.

Christiana Corporate, 200 Continental Drive,

Suite 401, Newark, Delaware – 19713, USA

T: +1-347-918-3531

For Sales Enquiries: sales@futuremarketinsights.com

Website: https://www.futuremarketinsights.com

LinkedIn| Twitter| Blogs | YouTube