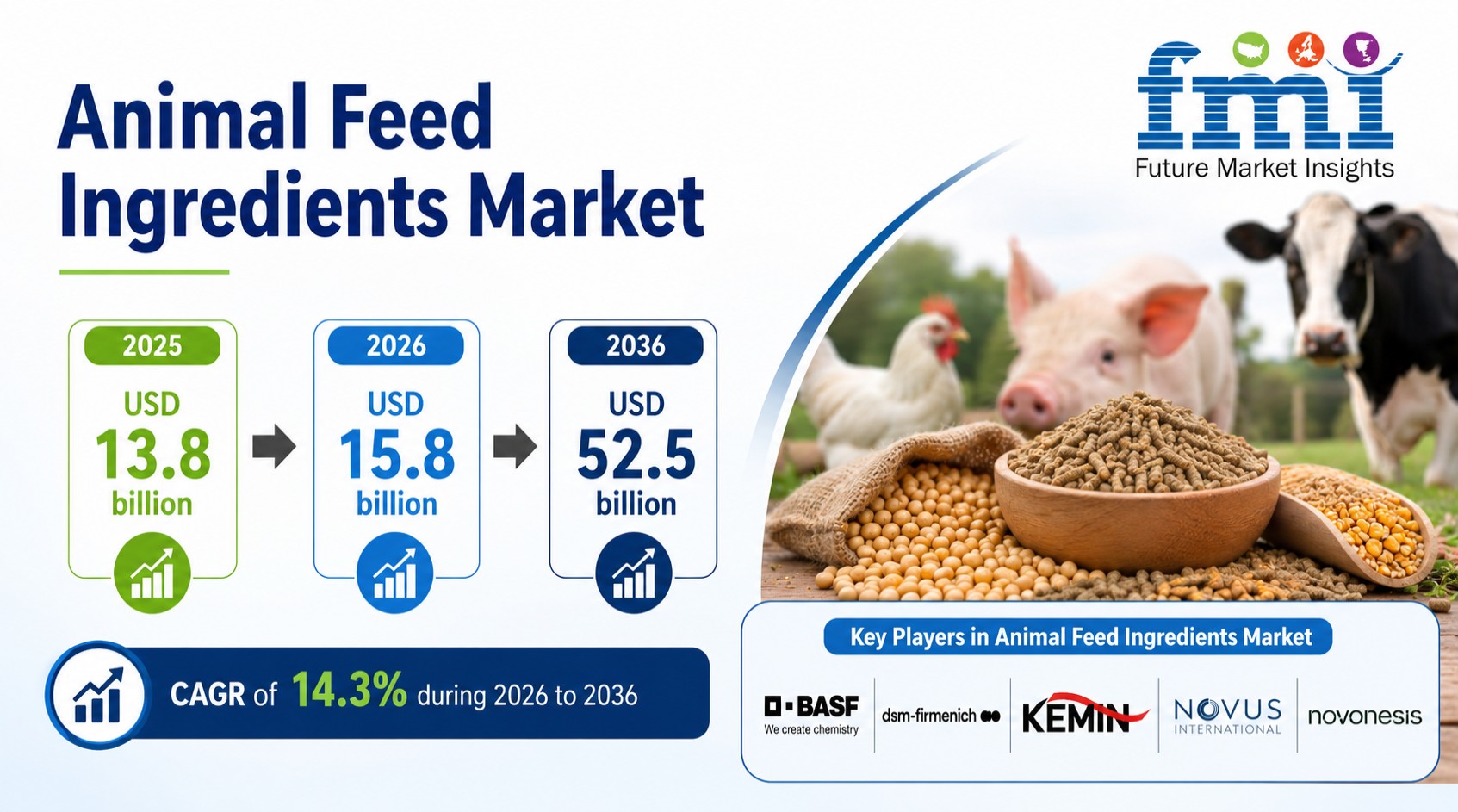

The global animal feed ingredients market is undergoing a structural expansion as modern livestock production transitions from basic volume output into highly precise, performance-linked nutrition management. Driven by regulatory changes, retailer standards, and the global push toward antibiotic growth promoter (AGP) reduction, the market is moving past simple least-cost ration balancing. Product demand is no longer governed merely by standard nutrient labels, but by the margin structures, processing survival, and gut-health protection intrinsic to functional ingredients. While traditional bulk inputs remain the core macro-supply, specialized additives like enzymes, probiotics, amino acids, and organic acids are aggressively locking down essential formulation roles by solving functional performance gaps.

Featured Snippet: Key Market Answer

Q: Why are functional feed ingredients shifting from optional boosters to formulation controls, and how do they address antibiotic-free production challenges?

A: Functional ingredients are becoming mandatory formulation controls because removing antibiotics exposes livestock to higher mortality, poor feed conversion, and performance variability. Traditional feed raw materials cannot maintain gut integrity or uniform growth under commercial stress on their own. Functional inputs like eubiotics, enzymes, and amino acids do not simply substitute for antibiotics; they actively control the digestive environment. They absorb the processing, stabilization, and technical development costs required to optimize nutrient digestibility, regulate microbial balance, and protect young-animal development.

Quick Stats of the Animal Feed Ingredients Market

- Core Growth Theme: Precision Nutrition and Gut-Health Management

- Dominant Objective: Minimizing performance variability across poultry, swine, dairy, and aquaculture

- Primary Sales Channel: Direct Technical Selling (driven by formulation support and farm trial scale-ups)

- Key Commercial Application: Starter feeds and young-animal vulnerability stages

- Crucial Technological Variable: Processing tolerance (thermal stability during pelleting and extrusion)

Market Overview: Formats Dictate the Margin Structure

The animal feed ingredients sector has evolved into a highly specialized ecosystem spanning bulk proteins, amino acids, feed enzymes, eubiotics, microbial additives, and encapsulated organic acids. Each input operates under entirely distinct production realities and cost-to-serve economics.

As modern integrators and large feed mills enter an era focused heavily on animal welfare and strict retail standards, procurement logic has shifted. Buyers no longer evaluate feed components solely by price-per-ton; they calculate precise cost-per-outcome metrics, such as feed conversion ratios (FCR) and uniformity across the flock or herd. This systemic maturation forces feed manufacturers to precisely align their raw material architectures with highly specific production stress periods, young-animal starter phases, or environmental challenges like heat and stocking density.

Key Growth Drivers across Formats

Broadening Consumer Base & Lifestyle Conversion

The transition away from sub-therapeutic antibiotic use toward clean-label and verified meat, milk, and egg production has fundamentally expanded the total addressable market for specialty additives. Commercial producers increasingly rely on functional inputs to mitigate the natural disease pressures and digestive drop-offs that occur when AGPs are removed from the system.

Precision Around Use Occasions

Growth is directly tied to targeted life-stage and species-specific applications. Starter feed programs for young piglets, chicks, and calves require exact dosing and highly digestible inputs to reduce early mortality risk, whereas later-stage feeds focus on maximizing muscle synthesis and environmental resilience.

The Trade-off of Preparation Friction

While traditional operations historically accepted the performance variability of simple grain-soy rations to keep input costs low, modern commercial integrators willingly absorb the higher unit cost of technical additives. Bypassing early-stage development issues, processing losses, and high mortality rates outweighs the initial cost of premium formulation inputs.

Strategic Channel Alignment

Ingredient physics and documentation govern market placement. Standard micro-ingredients thrive in digital supply networks and large-scale bulk distribution models. Meanwhile, sensitive live organisms, enzymes, and custom organic acid pre-mixes require direct technical selling channels where suppliers provide validation data, regulatory compliance, and on-site optimization support.

Technical & Ingredient Economics Balancing Act

Raw material choices heavily dictate profitability and product stability across different processing mechanisms:

- The Digestion Matrix: Feed enzymes like phytase, carbohydrases, and proteases allow nutritionists to adjust formulation matrix values dynamically. By unlocking bound nutrients from raw grains, brands can safely incorporate lower-cost alternative ingredients, mitigating the margin exposure brought on by volatile global commodity pricing.

- The Plant-Based Formulation Tax: Navigating alternative protein and plant-based carrier systems expanding into aquaculture and young-animal feed allows suppliers to target sustainability metrics. However, it imposes severe processing hurdles, often altering water stability or introducing anti-nutritional factors that require heavy texturizing and specialized processing to keep the feed palatable and bioavailable.

- Stability and Processing in Liquids and Pellets: Manufacturing functional feeds requires intense mastery over sensory and physical stability. Delicate inputs like live probiotic strains face severe viability threats from the heat, pressure, and moisture of standard grinding and pelleting lines, driving a technical need for specialized encapsulation or advanced thermostable product variations.

Segment Deep Dive: Powder vs. Alternative Formats

Multi-Serve Powders: The Value Anchor

Standard bulk ingredients and basic amino acid powders maintain total volume leadership. From a logistics standpoint, these commodities strip out unnecessary water weight, optimize cargo density, and provide long-term storage safety. For routine feed mill operations, bulk dry inputs remain the undisputed cost engine for baseline ration construction.

RTDs & Functional Liquids: The Premium Challenger

Liquid enzymes and post-pelleting application systems represent the high-margin frontier for complex processing setups. By applying temperature-sensitive functional inputs after the high-heat manufacturing phase, producers bypass stability issues. However, utilizing these liquid networks demands precision spraying infrastructure and highly rigorous equipment calibration.

Bars, Gels, and Edible Snacks: The Portability Play

Specialized starter gels, block supplements, and texturized creep feeds compete directly for pocket-share in high-value young-animal care. Commercial success in this category rests entirely on avoiding texturizing errors such as moisture loss or rapid degradation under barn conditions while maintaining highly stable, nutrient-dense profiles that attract young animals during early weaning periods.

Regional Market Dynamics

North America

North America maintains structural market leadership, backed by high per-capita meat production, highly sophisticated data integration setups, and advanced research networks pushing novel delivery breakthroughs like feed encapsulation and targeted gut-delivery systems.

Europe

The European marketplace is heavily steered by rigorous regulatory frameworks regarding EFSA health claims, strict historical bans on antibiotic growth promoters, and an intense commercial focus on nitrogen waste reduction, environmental tracing, and fully sustainable sourcing.

Asia-Pacific

Asia-Pacific represents the fastest-growing geographical region. Driven by rapid livestock urbanization, massive aquaculture modernization networks in China, and a surging youth workforce entering commercial farming frameworks in India, the region is rapidly scaling up its use of high-efficiency amino acid balancing and specialized young-animal starter feeds.

Competitive Differentiation Strategies

To maintain defensible premium pricing and secure high-value feed mill listings, leading manufacturers focus heavily on technical validation rather than basic product marketing:

- Third-Party Testing & Verification: With tightening scrutiny around food chain tracking, securing independent validation regarding contaminant control, active content stability, and claim accuracy is vital for gaining entry into major commercial integration channels.

- Controlled Hydrolysis Technology: Advancements in enzyme processing allow suppliers to offer targeted, pre-digested peptide structures that optimize absorption while drastically reducing the bitter notes and anti-nutritional factors common in raw plant isolates.

- Supply Chain Diversification: Top-tier ingredient companies are intentionally blending diverse probiotic strains, organic minerals, and plant-derived phytogenics within their commercial portfolios to hedge against sudden agricultural supply blocks and raw material price shifts.

Industry FAQs

What is the projected size of the global sports nutrition market? (Note: Retained context from architectural benchmark document) The global sports nutrition market is evaluated at USD 27.3 billion in 2025 and is projected to reach USD 65.6 billion by 2036, compounding at an 8.3% CAGR, driven by the normalization of performance nutrition across everyday lifestyle consumers.

Why does powder remain the leading format despite the rise of RTDs? (Note: Retained context from architectural benchmark document) Powder is highly defensible due to basic physics and supply chain math. It strips out water weight, maximizes active ingredient density per square inch of cargo space, offers long-term shelf stability, and provides consumers with the lowest possible cost-per-serving.

What are the primary operational risks when expanding from powders into liquids? (Note: Retained context from architectural benchmark document) Brands migrating into RTDs must manage massive spikes in freight costs (shipping water weight), strictly regulate liquid temperature stability, navigate high shelf-space slotting fees in physical retail, and manage shelf-stable sensory profiles to prevent protein degradation.

How is the Asia-Pacific region impacting global market strategy? (Note: Retained context from architectural benchmark document) Led by double-digit CAGRs in powerhouse growth markets like China and India, Asia-Pacific is driving major volume for entry-level functional formats, pulling forward global brand upgrades, and accelerating demand for lifestyle-friendly sports snacks.

Conclusion

The future architecture of the animal feed ingredients market will not be defined by a single additive category displacing another. Instead, commercial victory belongs to suppliers that treat format and functional validation as a core economic strategy.

Standard bulk materials will maintain their undisputed status as the volume engines for everyday baseline ration requirements. Concurrently, specialized convenience formats like encapsulated organic acids, thermostable enzymes, and validated probiotic strains will continue to lock down high-margin premium spaces by charging for the systematic reduction of producer risk. Success requires aligning raw formulation costs, processing constraints, and regulatory documentation directly with the exact performance outcome the producer expects at each specific stage of the production cycle.

Related Research Reports

- Animal Feed Additives Market – Supply chain analysis mapping the macro-trends across enzymes, amino acids, and plant isolates.

- Marine Active Ingredients Market – In-depth strategic analysis of marine lipids, proteins, peptides, carbohydrates, and pigments driving innovation across nutraceutical, pharmaceutical, food, and personal care industries.

- Cattle Feed Market – In-depth strategic analysis of concentrate feeds, roughages, feed additives, and precision nutrition solutions driving productivity, animal welfare, and commercial livestock performance.

FMI Custom Research: Strategic Intelligence for Confident Decision-Making

In today’s rapidly evolving business environment, leadership teams need more than market data they need clear, actionable intelligence tailored to their strategic objectives. FMI’s Custom Research solutions are designed around the specific business questions organizations need answered, enabling executives to evaluate growth opportunities, validate investments, assess competitive dynamics, and reduce uncertainty before making critical decisions. By combining deep industry expertise, primary research, and proprietary market intelligence, FMI delivers insights that help organizations move from assumptions to evidence-based strategies with greater speed and confidence.

Key Executive Benefits

- Decision-Ready Insights: Research tailored to your specific business challenges, growth plans, and investment priorities.

- Reduced Strategic Risk: Validate market opportunities, customer demand, and competitive positioning before committing resources.

- Market Entry Confidence: Assess opportunity size, regulatory barriers, channel dynamics, and competitive landscapes with precision.

- Competitive Advantage: Gain proprietary intelligence unavailable through syndicated reports or internal datasets.

- Faster Growth Decisions: Accelerate expansion, product development, portfolio optimization, and investment planning.

- Primary Market Validation: Access real-world customer, buyer, and stakeholder insights that support high-confidence decision-making.

- Global Industry Expertise: Powered by 100+ analysts, 20,000+ published reports, and 1.6 million+ hours of research experience.

- Proven Track Record: Over 7,000 market-entry engagements completed across six regions and 14 industry sectors with strong client retention.

Business Impact

FMI helps organizations transform market complexity into strategic clarity, enabling leadership teams to identify growth opportunities faster, optimize resource allocation, strengthen competitive positioning, and make high-stakes business decisions with confidence.

To explore how FMI Custom Research can support your strategic priorities, please connect with our team at – sales@futuremarketinsights.com

About Future Market Insights (FMI)

Future Market Insights is a leading provider of market intelligence, consulting services, and syndicated research reports. FMI delivers actionable insights across food and beverage, healthcare, consumer goods, biotechnology, chemicals, industrial products, and emerging technologies, helping organizations identify growth opportunities and make informed strategic decisions in evolving global markets.

Contact Us:

Future Market Insights Inc.

Christiana Corporate, 200 Continental Drive,

Suite 401, Newark, Delaware – 19713, USA

T: +1-347-918-3531

Why FMI: https://www.futuremarketinsights.com/why-fmi

For Sales Enquiries: sales@futuremarketinsights.com

Website: https://www.futuremarketinsights.com