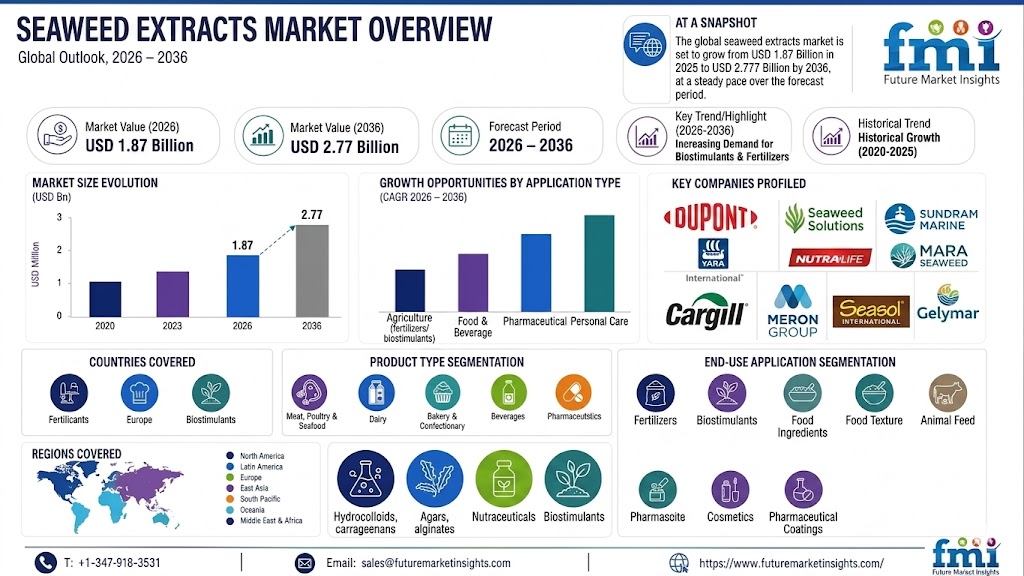

According to the latest insights by Future Market Insights, the global Seaweed Extracts market is undergoing significant transformation as geographic specialization, processing concentration, logistics exposure, and supply chain dependencies increasingly influence pricing structures. In 2026, the separation between Southeast Asia’s biomass cultivation strength and China’s industrial extraction capacity is creating new cost tiers, supply risks, and pricing dependencies across global seaweed extract markets.

Industry analysts highlight that Seaweed Extracts pricing is no longer determined only by raw biomass availability but is increasingly shaped by cultivation economics, processing throughput, freight conditions, energy costs, environmental compliance, trade policies, and manufacturers’ ability to convert marine biomass into consistent industrial-grade extracts.

Markets dependent on imported extracts are experiencing stronger exposure to processing concentration risks, while producers with integrated sourcing and diversified processing networks are gaining greater supply stability.

Southeast Asia’s Biomass Dominance Drives Raw Material Supply Dynamics

Southeast Asia remains the primary production hub for the major seaweed species used in commercial Seaweed Extracts, including Eucheuma, Kappaphycus, and Gracilaria.

Countries such as Indonesia and the Philippines account for a significant share of global tropical seaweed cultivation due to favorable environmental conditions, including:

- Warm coastal waters

• High year-round cultivation suitability

• Nutrient-rich marine ecosystems

• Extensive shallow farming zones

Seaweed farming benefits from relatively low cultivation costs because production depends heavily on manual labor, small-scale coastal farms, and community-based farming systems.

Typical production advantages include:

- Low capital requirements

• Multiple harvest cycles annually

• Large cultivation capacity

• Flexible smallholder supply networks

These conditions allow Southeast Asian producers to maintain competitive biomass pricing compared with higher-cost cultivation regions.

However, biomass quality remains a critical pricing factor. Differences in:

- Moisture levels

• Carrageenan content

• Purity

• Contamination levels

• Drying practices

create price differentiation between standard and premium biomass grades.

Farmers producing consistent quality biomass can achieve higher pricing premiums due to stronger processor demand and lower pre-processing losses.

China’s Processing Capacity Creates the Global Extract Supply Hub

While Southeast Asia dominates biomass cultivation, China has developed into the leading center for industrial Seaweed Extract processing.

Over previous decades, Chinese processors invested heavily in:

- Extraction facilities

• Filtration systems

• Concentration equipment

• Spray-drying technology

• Quality control infrastructure

Large-scale processing facilities provide significant advantages through:

- Lower unit production costs

• Higher throughput efficiency

• Advanced technical capabilities

• Consistent extract specifications

The extraction process requires substantial investment because converting biomass into refined extracts involves multiple stages, including:

- Chemical extraction

• Separation and purification

• Concentration

• Drying

• Quality testing

Processing scale has become a major competitive advantage, allowing large processors to capture higher value from seaweed biomass compared with raw material suppliers.

As processing capacity becomes concentrated among fewer industrial operators, global Seaweed Extract availability increasingly depends on processor utilization rates rather than biomass supply alone.

Processing Concentration Creates New Supply Chain Risk Points

The Seaweed Extract supply chain operates through two specialized geographic stages:

Stage 1: Biomass Production

Southeast Asia provides:

- Cultivation capacity

• Low-cost raw material supply

• Species diversity

Stage 2: Industrial Processing

China provides:

- Extraction expertise

• Manufacturing infrastructure

• Finished ingredient supply

This geographic split creates efficiency but also introduces vulnerabilities.

Even when biomass production remains strong, extract supply can face disruption due to:

- Processing capacity constraints

• Energy shortages

• Environmental restrictions

• Equipment downtime

• Manufacturing delays

This means supply reliability increasingly depends on processing availability rather than biomass abundance alone.

Two Pricing Nodes Shape Seaweed Extract Economics

The Seaweed Extract value chain has developed two major pricing points.

Biomass Pricing Node

Raw seaweed biomass pricing depends on:

- Species type

• Dry matter content

• Carrageenan yield

• Cleanliness

• Seasonal availability

Farmgate prices are influenced by local supply-demand conditions and farmer bargaining power.

Because biomass requires drying and has limited storage flexibility, producers often have limited ability to delay sales.

Extract Pricing Node

Industrial-grade extracts represent the second pricing point after:

- Extraction

• Refinement

• Concentration

• Drying

are completed.

Extract pricing reflects:

- Biomass input costs

• Chemical usage

• Energy consumption

• Processing labor

• Equipment depreciation

• Quality certification

• Profit margins

The transformation from biomass to refined extract creates substantial value addition, with processors capturing a larger portion of economic value due to specialized infrastructure requirements.

Freight and Container Conditions Influence Delivered Pricing

Seaweed biomass requires international transportation before processing, making logistics a major cost consideration.

Freight economics are influenced by:

- Container availability

• Shipping routes

• Fuel costs

• Port congestion

• Export seasonality

Container imbalance creates additional pressure because agricultural exports compete with other commodities for shipping capacity.

During periods of tight logistics availability:

- Freight costs increase

• Delivery timelines extend

• Inventory requirements rise

• Processor margins tighten

Processors often maintain additional biomass inventory to protect against supply interruptions, but prolonged freight disruption can lead to:

- Higher extract prices

• Longer lead times

• Reduced production flexibility

Buyers increasingly evaluate total landed cost rather than only supplier pricing.

Energy Costs and Environmental Compliance Reshape Processing Economics

Seaweed extraction is energy-intensive due to:

- Heating requirements

• Concentration processes

• Spray drying operations

Energy price volatility directly influences manufacturing economics.

Rising energy costs increase:

- Processing expenses

• Production costs

• Finished extract pricing

Environmental regulations also affect processing capacity.

Extraction generates wastewater containing:

- Organic residues

• Processing chemicals

• Suspended materials

Stricter discharge requirements require investment in:

- Waste treatment systems

• Monitoring infrastructure

• Compliance technologies

Smaller processors may face greater pressure due to the cost of meeting environmental standards, further increasing market concentration.

Trade Friction Creates Additional Cost Layers

Finished Seaweed Extracts are traded globally, exposing the industry to:

- Tariff changes

• Import regulations

• Trade restrictions

• Regional compliance requirements

Processors and buyers increasingly focus on:

- Supply chain transparency

• Regional production strategies

• Multi-source procurement

Some companies are exploring alternative processing locations to reduce trade exposure and improve regional supply security.

Alternative Processing Regions Gain Strategic Importance

Although China remains a dominant processing center, buyers are increasingly exploring supply diversification through:

- Secondary processing hubs

• Regional partnerships

• Direct investment models

• Long-term processor agreements

Emerging processing locations may help reduce dependence on a single manufacturing region.

However, alternative capacity development remains limited because extraction requires:

- Specialized equipment

• Technical expertise

• Significant capital investment

• Stable biomass access

Future Outlook

The future of the Seaweed Extracts industry will be shaped by the interaction between biomass availability, processing capacity, logistics efficiency, and supply chain diversification.

Manufacturers are expected to focus on:

- Integrated sourcing models

• Regional processing expansion

• Supply chain resilience

• Advanced extraction technologies

• Quality consistency improvements

Growing demand for natural hydrocolloids, plant-based ingredients, agricultural biostimulants, and functional marine ingredients will continue supporting market expansion.

As the industry evolves, pricing competitiveness will increasingly depend on balancing Southeast Asia’s biomass advantage with global processing capability and supply chain reliability.

FMI Custom Research: Strategic Intelligence for Confident Decision-Making

In today’s rapidly evolving business environment, leadership teams need more than market data—they need clear, actionable intelligence tailored to their strategic objectives. FMI’s Custom Research solutions are designed around the specific business questions organizations need answered, enabling executives to evaluate growth opportunities, validate investments, assess competitive dynamics, and reduce uncertainty before making critical decisions.

By combining deep industry expertise, primary research, and proprietary market intelligence, FMI delivers insights that help organizations move from assumptions to evidence-based strategies with greater speed and confidence.

Key Executive Benefits

- Decision-Ready Insights: Research tailored to specific business challenges, expansion plans, and investment priorities.

• Reduced Strategic Risk: Validate market opportunities, supply risks, and competitive positioning before allocating resources.

• Market Entry Confidence: Assess market size, regulations, supply structures, and competitive landscapes.

• Competitive Advantage: Gain proprietary intelligence beyond traditional syndicated research.

• Faster Growth Decisions: Support product development, geographic expansion, and strategic planning.

• Primary Market Validation: Access real-world buyer and stakeholder insights.

• Global Industry Expertise: Powered by 100+ analysts, 20,000+ published reports, and 1.6 million+ hours of research experience.

• Proven Track Record: Over 7,000 market-entry engagements completed across six regions and 14 industry sectors.

Business Impact

FMI helps organizations transform market complexity into strategic clarity, enabling leadership teams to identify growth opportunities faster, optimise resources, strengthen competitive positioning, and make high-impact business decisions with confidence.

To explore how FMI Custom Research can support your strategic priorities, please connect with our team at: sales@futuremarketinsights.com

Explore More Related Studies Published by FMI Research:

Algae Protein Market: Global Industry Analysis and Opportunity Assessment 2025–2035

Marine Ingredients Market: Global Industry Analysis and Opportunity Assessment 2025–2035

About Future Market Insights (FMI)

Future Market Insights, Inc. (FMI) is an ESOMAR-certified, ISO 9001:2015 market research and consulting organization, trusted by Fortune 500 clients and global enterprises.

With operations in the U.S., UK, India, and Dubai, FMI provides data-backed insights and strategic intelligence across 30+ industries and 1200 markets worldwide.

Contact Us:

Future Market Insights Inc.

Christiana Corporate, 200 Continental Drive,

Suite 401, Newark, Delaware – 19713, USA

T: +1-347-918-3531

Why FMI: https://www.futuremarketinsights.com/why-fmi

Website: https://www.futuremarketinsights.com