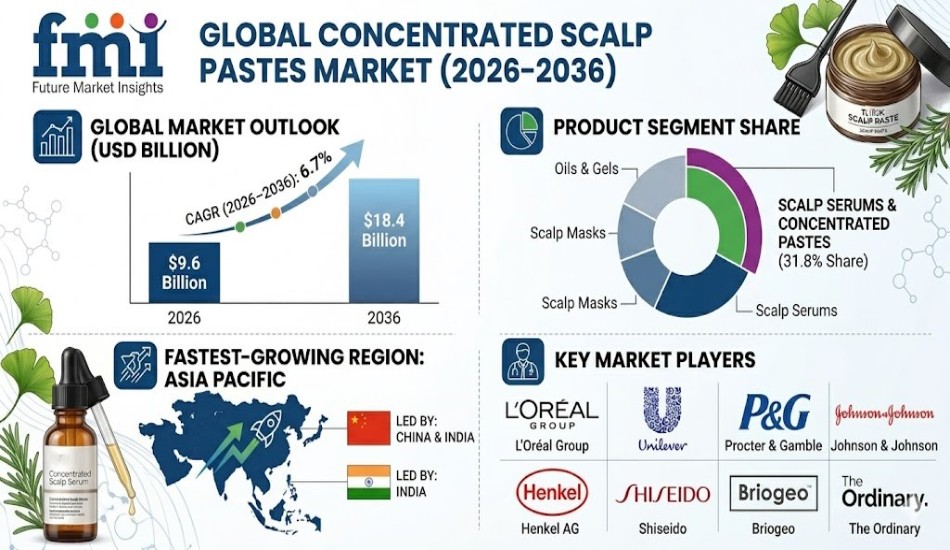

The global concentrated scalp pastes market is witnessing robust growth, driven by the convergence of dermatological science, high-efficacy formulations, and the rising importance of scalp health in modern hair care routines. According to Future Market Insights, the market is valued at USD 9.6 billion in 2026 and is projected to reach USD 18.4 billion by 2036, registering a CAGR of 6.7% over the forecast period.

This growth reflects a fundamental shift from cosmetic hair care toward treatment-led scalp therapy, where concentrated paste formats deliver targeted, long-lasting therapeutic benefits. These products are increasingly positioned as core solutions for inflammation control, microbiome balance, and follicular health rather than short-term cleansing alternatives.

Market Snapshot: Concentrated Scalp Pastes Market

Key Market Metrics

- Market Size (2026): USD 9.6 Billion

- Forecast Value (2036): USD 18.4 Billion

- CAGR (2026–2036): 6.7%

- Leading Product Segment: Scalp Serums & Concentrated Pastes (31.8% share)

- Dominant End Use: Hair Loss & Thinning (28.9% share)

- Leading Distribution Channel: Online Retail (36.4% share)

- Fastest-Growing Region: Asia Pacific (led by China & India)

- Key Players: L’Oréal Group, Unilever, Procter & Gamble, Johnson & Johnson, Henkel AG, Shiseido, Briogeo, The Ordinary

Discover Growth Opportunities in the Market – Get Your Sample Report Now : https://www.futuremarketinsights.com/reports/sample/rep-gb-31797

Growth Dynamics and Demand Drivers

The market is expanding rapidly due to a “dermatological pivot” in consumer behavior, where scalp care is increasingly viewed as the foundation of hair health. Consumers are shifting away from frequent, low-efficacy cleansing routines toward high-potency, low-frequency treatments that address root causes such as microbiome imbalance and inflammation.

Another major driver is the skinification of hair care, where ingredients traditionally used in skincare—such as ceramides, exfoliating acids, and probiotics—are now being incorporated into scalp formulations. This has elevated concentrated scalp pastes into dermocosmetic treatment categories.

Technological innovation is also accelerating adoption. Encapsulation systems, pH-controlled release mechanisms, and AI-powered scalp diagnostics are enhancing product performance and personalization, making these formats more effective and accessible.

Additionally, the growth of digital-first distribution channels supports adoption by enabling consumer education, guided routines, and subscription-based treatment models.

Segment Insights

By Product Type

- Scalp serums & concentrated pastes lead with 31.8% share due to high active density

- Exfoliating scrubs and pre-wash pastes gaining traction for microbiome reset

- Scalp masks expanding within premium and salon-based treatments

By End Use

- Hair loss & thinning dominates with 28.9% share, driven by follicular health focus

- Oil control and dandruff solutions emphasize microbiome balance

- Sensitive scalp and wellness segments growing steadily

By Distribution Channel

- Online retail leads (36.4%), driven by education and guided usage

- Salon and professional channels expanding for clinical-grade treatments

- Specialty stores supporting premium brand positioning

By Ingredient Type

- Dermatological and clinical formulations dominate adoption

- Microbiome-focused technologies gaining strong traction

- Natural and botanical formulations evolving within regulated frameworks

Supply Chain and Industry Structure

The supply chain for concentrated scalp pastes is evolving toward clinical-grade formulation and compliance-driven manufacturing. Raw materials include high-potency actives such as anti-inflammatory agents, microbiome regulators, and follicle-support compounds.

Major global players like L’Oréal, Unilever, and Procter & Gamble leverage advanced R&D ecosystems and dermatologist collaborations, while emerging brands focus on ritual-based treatments and direct-to-consumer engagement.

Distribution is increasingly diversified across e-commerce platforms, dermatology clinics, and professional salons, reflecting the hybrid positioning of these products between cosmetics and therapeutic care.

Pricing and Value Trends

Pricing is shifting toward a value-per-treatment model, where consumers evaluate products based on efficacy and longevity rather than upfront cost. Concentrated scalp pastes, requiring fewer applications, offer strong perceived value despite premium pricing.

Premium brands emphasize clinical validation and long-term scalp benefits, while mass-market players focus on accessible, dermatologist-inspired solutions.

Competitive Landscape

The market is led by multinational corporations with strong clinical research capabilities and global distribution networks. Companies such as L’Oréal, Unilever, Procter & Gamble, Henkel, and Shiseido dominate through dermatology-backed innovation and portfolio expansion.

At the same time, challenger brands like Briogeo and The Ordinary are gaining traction by focusing on ingredient transparency, microbiome science, and targeted treatment positioning.

Competition is increasingly centered on clinical efficacy, formulation science, and consumer education, rather than traditional branding alone.

Regional Analysis

Asia Pacific (High Growth Hub)

- China (7.8% CAGR): Regulatory standardization driving clinical adoption

- India (7.5% CAGR): Growth supported by AYUSH-led formalization and rising awareness

Europe

- Germany (6.9%): Strong shift toward anhydrous, chemical-safe formulations

- High demand for transparency and regulatory compliance

North America

- United States (6.2%): Growth driven by clinical validation and dermatology integration

- Increasing adoption in professional treatment settings

Other Markets

- United Kingdom (5.7%): Preventative healthcare approach boosting demand

- Emerging markets seeing faster adoption through professional education

Future Outlook and Opportunities

Looking ahead, the concentrated scalp pastes market is expected to evolve into a core segment of dermatology-led hair care. Growth will increasingly depend on clinical validation, biomarker-driven formulations, and personalized treatment systems.

Key opportunities include:

- Advanced microbiome-targeted technologies

- Integration of AI-driven scalp diagnostics

- Expansion into subscription-based treatment ecosystems

- Growth in emerging markets with regulatory formalization

Companies that successfully combine high-efficacy formulations, regulatory compliance, and consumer education will be best positioned to capture long-term value.

Conclusion

The rise of concentrated scalp pastes marks a significant transformation in the global hair care industry. As scalp health becomes central to beauty and wellness routines, these high-potency formats are moving beyond niche applications into mainstream adoption.

With strong clinical backing, evolving consumer awareness, and continued innovation, the market is set to experience sustained and high-value growth through 2036, redefining the future of scalp and hair care.

Why FMI: https://www.futuremarketinsights.com/why-fmi

About Future Market Insights (FMI)

Future Market Insights, Inc. (FMI) is an ESOMAR-certified, ISO 9001:2015 market research and consulting organization, trusted by Fortune 500 clients and global enterprises. With operations in the U.S., UK, India, and Dubai, FMI provides data-backed insights and strategic intelligence across 30+ industries and 1200 markets worldwide.

Contact Us:

Future Market Insights Inc.

Christiana Corporate, 200 Continental Drive,

Suite 401, Newark, Delaware – 19713, USA

T: +1-347-918-3531

For Sales Enquiries: sales@futuremarketinsights.com

Website: https://www.futuremarketinsights.com

LinkedIn| Twitter| Blogs | YouTube