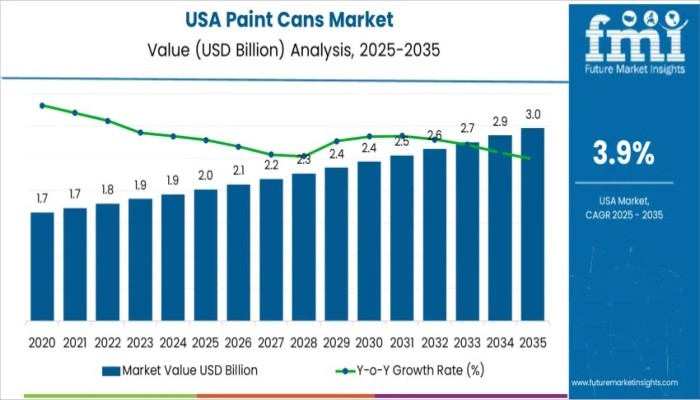

The demand for paint cans in the United States continues to reflect the country’s deep-rooted culture of renovation, construction, and ongoing maintenance across residential, commercial, and industrial spaces. Valued at USD 2.0 billion in 2025, the USA paint cans market is forecast to reach USD 3.0 billion by 2035, expanding at a CAGR of 3.9%. This measured yet reliable growth highlights the importance of rigid packaging formats in preserving paint quality while adapting to evolving regulatory, sustainability, and end-user expectations.

Market Overview: A Mature Industry with Room for Innovation

Paint cans remain a foundational component of the U.S. coatings ecosystem. From residential repainting cycles and commercial refurbishments to industrial and infrastructure maintenance, demand for durable, sealed containers remains consistent.

While the industry operates close to saturation due to its maturity, steady repainting demand and DIY culture ensure ongoing volume. Incremental growth is further supported by infrastructure refurbishment programs and the continued use of both solvent-based and water-based formulations that require reliable, protective packaging.

Discover Growth Opportunities in the Market – Get Your Sample Report Now

Quick Stats: USA Paint Cans Demand

- Sales Value (2025): USD 2.0 billion

- Forecast Value (2035): USD 3.0 billion

- CAGR (2025–2035): 3.9%

- Leading Packaging Type: Metal cans

- Key Growth Regions: West USA, South USA, Northeast USA

- Top Players: Ball Corporation, RPC Group Plc., Silgan Containers LLC, Kian Joo Can Factory Berhad, Colep Portugal S.A.

Why Demand for Paint Cans Is Growing

The steady rise in demand is closely tied to how Americans live, build, and maintain their environments. Home improvement activity, driven by real estate turnover and lifestyle upgrades, sustains frequent repainting. Contractors and professional painters continue to rely on standardized 1-gallon and 5-gallon cans for efficiency and compliance, while DIY consumers favor smaller formats for convenience.

Growth in industrial coatings, including automotive, marine, and infrastructure applications, further boosts demand for heavy-duty cans that resist corrosion and ensure long shelf life. Retail hardware chains and paint stores depend on standardized packaging to support custom color mixing, private-label offerings, and compliance with volatile organic compound (VOC) regulations.

Product and Material Trends Shaping the Market

By Product Type: Metal Cans Lead

Metal cans account for 44.9% of total demand, retaining leadership due to their strength, airtight sealing, and compatibility with solvent-based and industrial coatings.

Key Highlights:

- Metal cans dominate industrial and protective coatings

- Plastic cans (33.0%) support water-based paints and lightweight handling

- Hybrid cans (22.1%) balance dent resistance with material reduction

By Material Type: Plastic Gains Momentum

Plastic accounts for 57.0% of material usage, driven by cost efficiency, dent resistance, and ease of handling. Metal, at 43.0%, remains essential where vapor barriers and long-term storage are critical.

Key Highlights:

- Plastic improves consumer convenience and logistics efficiency

- Metal retains importance for volatile and protective coatings

- Sustainable plastics with improved barriers are gaining traction

By Capacity: Small Packs Dominate

Cans of 1000 ml and below represent 38.5% of demand, reflecting strong DIY activity and small-project repainting needs.

Key Highlights:

- Small packs align with DIY and trial color usage

- Mid-size cans support contractors and maintenance work

- Large formats serve industrial and commercial repaint cycles

Regional Dynamics: Where Demand Is Strongest

Demand is concentrated in regions with high construction spending and renovation frequency.

- West USA (4.5% CAGR): Driven by remodeling activity, sustainability mandates, and strong DIY culture

- South USA (4.0% CAGR): Supported by new housing, warm climates, and industrial coatings demand

- Northeast USA (3.6% CAGR): Urban renovations and compact living favor smaller can sizes

- Midwest USA (3.1% CAGR): Stable demand from manufacturing, agriculture, and infrastructure maintenance

Competitive Landscape: Established Leaders and Expanding Innovators

The competitive structure of the U.S. paint cans market is shaped by scale, technical expertise, and distribution reach. Ball Corporation leads with an estimated 37.3% share, leveraging integrated metal packaging operations and long-term partnerships with major coatings brands.

Other key players include:

- RPC Group Plc. – Flexible solutions across metal and plastic formats for niche and private-label coatings

- Silgan Containers LLC – Strong regional presence and reliable can-body manufacturing

- Kian Joo Can Factory Berhad – Cost-competitive bulk supply supporting value-focused brands

- Colep Portugal S.A. – High-specification cans for aerosol and protective coatings

Beyond established leaders, new and mid-sized manufacturers are increasingly investing in lightweight steel designs, improved linings, spill-control features, and recyclable materials. These innovations help suppliers differentiate, meet environmental standards, and support coatings brands seeking modern, sustainable packaging solutions.

Why FMI: https://www.futuremarketinsights.com/why-fmi

About Future Market Insights (FMI)

Future Market Insights, Inc. (FMI) is an ESOMAR-certified, ISO 9001:2015 market research and consulting organization, trusted by Fortune 500 clients and global enterprises. With operations in the U.S., UK, India, and Dubai, FMI provides data-backed insights and strategic intelligence across 30+ industries and 1200 markets worldwide.

Contact Us:

Future Market Insights Inc.

Christiana Corporate, 200 Continental Drive,

Suite 401, Newark, Delaware – 19713, USA

T: +1-347-918-3531

For Sales Enquiries: sales@futuremarketinsights.com

Website: https://www.futuremarketinsights.com

LinkedIn| Twitter| Blogs | YouTube