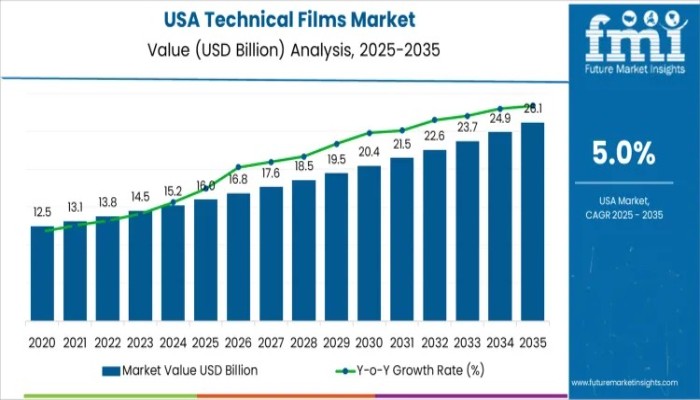

The demand for technical films in the United States is entering a phase of sustained and innovation-led growth, supported by expanding industrial usage, advanced manufacturing investments, and rising adoption across high-performance applications. Valued at USD 16.0 billion in 2025, the USA technical films market is projected to reach USD 26.1 billion by 2035, advancing at a CAGR of 5.0%. This growth reflects the essential role technical films play in modern electronics, automotive engineering, medical packaging, renewable energy systems, and specialty labeling.

Polyester-based films particularly PET and BOPET continue to dominate the market due to their balanced mechanical strength, optical clarity, barrier performance, and compatibility with high-speed processing lines. These advantages make them a preferred choice for both established manufacturers and new entrants seeking scalable, future-ready material solutions.

Unlock Growth Potential and Explore Market Opportunities With Our Comprehensive Industry Overview. Request Your Sample Now

Quick Stats: USA Technical Films Demand Outlook

- Market Value (2025): USD 16.0 billion

- Forecast Value (2035): USD 26.1 billion

- Forecast CAGR (2025–2035): 5.0%

- Leading Material Category: Polyester (PET/BOPET) Films

- Key Growth Regions: West USA, South USA, Northeast USA

- Top Players: 3M Company, DuPont, Eastman Chemical Company, Avery Dennison, Berry Global Inc.

Market Growth Outlook and Industry Dynamics

The USA technical films industry benefits from structurally stable baseline consumption combined with innovation-driven demand peaks. Electronics insulation, automotive component protection, medical compliance packaging, and specialty industrial labeling continue to shape procurement momentum. Consumption intensity remains highest in the West, South, and Northeast regions, where manufacturing density, healthcare infrastructure, and packaging throughput are strongest.

While global material science leaders anchor supply, new and mid-sized manufacturers are increasingly investing in advanced coating technologies, recyclable structures, and application-specific film formulations. This mix of established expertise and emerging innovation ensures controlled variability in demand cycles without structural downturns.

Why Demand for Technical Films Is Growing in the USA

Demand growth is fueled by the need for engineered materials that deliver barrier protection, electrical insulation, durability, and lightweight performance across multiple industries.

Key growth drivers include:

- Expansion of electronics and semiconductor manufacturing

- Lightweight material adoption in electric vehicles and mobility systems

- Rising use of sterilizable films in healthcare and medical devices

- Growth of solar energy and energy-efficient building solutions

- Increased automation requiring release films and surface protection layers

At the same time, manufacturers face challenges such as raw material price volatility, recycling complexities for multilayer films, and long qualification cycles in regulated sectors. These factors encourage incremental innovation rather than abrupt material shifts, favoring suppliers with strong R&D and regulatory capabilities.

Material and Application Trends Shaping Demand

Polyester Films Lead by Material Type

Polyester (PET/BOPET) films account for approximately 36.0% of total USA demand, supported by their tensile strength, thermal stability, cost efficiency, and suitability for coating and lamination.

Key advantages driving PET dominance:

- Strong compatibility with USA manufacturing infrastructure

- Expanding use in flexible electronics, solar cells, and precision packaging

- Ongoing advancements in thin-film and recyclable PET technologies

Other materials—including polyamide, polycarbonate, fluoropolymers, and specialty films—serve niche applications requiring chemical resistance, clarity, or superior dielectric performance.

Electronics & Electrical Applications Hold the Largest Share

Electronics and electrical applications represent around 40.0% of total demand, driven by usage in:

- Insulating layers and capacitor dielectrics

- Printed circuitry and flexible displays

- Protective films for smart devices and appliances

As USA semiconductor capacity expands and sustainability goals favor polymer-based engineering solutions, technical films remain central to innovation in IoT hardware, industrial automation, and renewable power infrastructure.

Regional Demand Patterns Across the United States

West USA: Innovation and Energy Applications Lead Growth

- CAGR: 5.8%

- Strong semiconductor, consumer electronics, and solar energy adoption

- High demand for UV-resistant, heat-stable, and precision-coated films

South USA: Automotive and Industrial Strength

- CAGR: 5.2%

- Automotive manufacturing and cold-chain packaging drive durable film demand

- Proximity to Gulf Coast resin production supports cost efficiency

Northeast USA: Medical and Specialty Film Innovation

- CAGR: 4.6%

- Medical device, pharmaceutical, and sensor manufacturing fuel demand

- Emphasis on regulatory compliance, traceability, and surface-treatment precision

Midwest USA: Stable Industrial and Packaging Consumption

- CAGR: 4.0%

- Durable goods, agricultural packaging, and food processing sustain baseline volumes

- Buyers prioritize long-run reliability and waste reduction on high-speed lines

Competitive Landscape: Established Leaders and Emerging Innovators

The competitive environment for technical films in the USA is defined by material science expertise, customization capabilities, regulatory compliance, and conversion efficiency. Established players continue to invest in advanced technologies while new manufacturers focus on niche applications and sustainable solutions.

Key market participants include:

- 3M Company – Specialty laminates, optical films, and insulation layers

- DuPont – High-performance polymer films for electronics and industrial use

- Eastman Chemical Company – Polyester films for solar control and automotive glazing

- Avery Dennison – Pressure-sensitive and industrial labeling film solutions

- Berry Global Inc. – Protective and process films with scalable USA manufacturing

Together, these companies—along with emerging suppliers—are shaping a resilient, innovation-driven market that supports lighter materials, energy efficiency, and advanced electronics integration.

Why FMI: https://www.futuremarketinsights.com/why-fmi

About Future Market Insights (FMI)

Future Market Insights, Inc. (FMI) is an ESOMAR-certified, ISO 9001:2015 market research and consulting organization, trusted by Fortune 500 clients and global enterprises. With operations in the U.S., UK, India, and Dubai, FMI provides data-backed insights and strategic intelligence across 30+ industries and 1200 markets worldwide.

Contact Us:

Future Market Insights Inc.

Christiana Corporate, 200 Continental Drive,

Suite 401, Newark, Delaware – 19713, USA

T: +1-347-918-3531

For Sales Enquiries: sales@futuremarketinsights.com

Website: https://www.futuremarketinsights.com

LinkedIn| Twitter| Blogs | YouTube