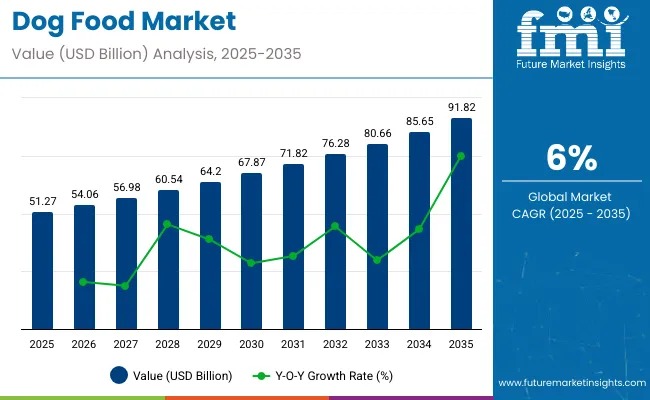

The global dog food market is entering a strong growth phase, projected to expand from approximately USD 51.27 billion in 2025 to around USD 91.82 billion by 2035, registering a steady compound annual growth rate (CAGR) of 6% over the forecast period. Rising pet ownership, increasing humanization of pets, and heightened awareness around canine nutrition and long-term health are reshaping consumer purchasing behavior worldwide.

Dogs are no longer viewed as companions alone; they are considered family members. This shift is driving owners to invest in high-quality, nutritionally balanced diets that mirror human food trends. As a result, premium, functional, and specialty dog food categories are witnessing robust demand across both developed and emerging economies.

Explore trends before investing – request a sample report today!

Growing emphasis on preventive healthcare for pets is significantly influencing product innovation. Manufacturers are focusing on clean-label formulations, functional ingredients, and targeted nutrition designed for breed, age, size, and health conditions. This evolution is strengthening the value proposition of dog food, transforming it from a basic necessity into a wellness-driven category.

Market Snapshot: Dog Food Industry Outlook

- Estimated Market Size (2025): USD 51.27 billion

- Projected Market Value (2035): USD 91.82 billion

- Value-based CAGR (2025–2035): 6%

Animal-Derived Ingredients Continue to Anchor Demand

Animal-derived ingredients such as chicken, beef, and fish remain central to dog food formulations, accounting for an estimated 36.8% market share in 2025. These ingredients offer superior digestibility and complete amino acid profiles essential for muscle development, immune support, and overall vitality.

In addition to protein, animal-origin ingredients deliver critical nutrients including Omega-3 fatty acids, which support joint mobility, skin health, cognitive function, and cardiovascular wellness. Their natural palatability aligns with dogs’ instinctive dietary preferences, while also reassuring owners seeking wholesome, biologically appropriate diets.

Manufacturers are increasingly emphasizing ethical sourcing and sustainability, ensuring traceability of animal proteins and reducing environmental impact. This strategy aligns with evolving consumer values and strengthens brand credibility in premium segments.

Specialty Pet Stores Drive Value-Based Growth

Distribution dynamics play a pivotal role in market expansion, with specialty pet stores accounting for nearly 34.8% of global sales in 2025. These outlets offer curated assortments of premium and veterinary-recommended products, supported by in-store expertise that helps pet owners make informed nutritional choices.

Personalized consultations, loyalty programs, and exclusive product launches enhance consumer engagement and encourage repeat purchases. Strategic collaborations between manufacturers and specialty retailers ensure efficient inventory management and faster rollout of innovative products, reinforcing this channel’s influence.

Sustainability and Innovation Reshape Product Portfolios

Sustainability has emerged as a defining theme across the dog food ecosystem. In 2025, Nestlé Purina launched a new line of sustainable, plant-based dog food, highlighting the industry’s shift toward environmentally responsible nutrition without compromising on quality or safety.

Beyond sustainability, innovation is accelerating across formats such as freeze-dried, dehydrated, and hybrid foods that combine the convenience of kibble with the nutritional benefits of raw or minimally processed ingredients. These formats appeal to time-conscious pet owners seeking nutrient retention and extended shelf life.

Regulatory Framework Ensures Safety and Transparency

Government regulations remain critical in safeguarding pet health and maintaining market integrity. Regulatory bodies worldwide enforce standards covering ingredient safety, nutritional adequacy, labeling accuracy, and manufacturing practices.

Key regulatory pillars include:

- Mandatory compliance with nutritional profiles such as AAFCO standards

- Strict labeling requirements for ingredient disclosure and feeding guidelines

- Enforcement of GMP and HACCP protocols

- Defined limits for contaminants including pathogens and heavy metals

Such frameworks foster consumer trust while encouraging manufacturers to maintain consistent quality across markets.

Regional Spending Patterns Highlight Growth Potential

Per capita spending on dog food varies significantly by region. Developed markets including the U.S., Canada, Germany, the UK, and Australia exhibit higher spending due to premiumization and strong awareness of pet health. Meanwhile, emerging markets such as China, India, Brazil, and South Africa are witnessing rapid growth driven by rising disposable incomes and expanding retail infrastructure.

Country-wise growth outlook (2025–2035):

- United States: 4.2% CAGR

- Germany: 3.8% CAGR

- United Kingdom: 2.7% CAGR

Competitive Landscape Remains Dynamic

The dog food market is moderately consolidated, led by global players with strong R&D capabilities and extensive distribution networks. Tier-1 companies such as Nestlé Purina, Mars Petcare, Hill’s Pet Nutrition, and The J.M. Smucker Company continue to drive innovation in formulation, sustainability, and targeted nutrition.

Regional and niche players are also gaining traction by focusing on specialized diets, premium ingredients, and agile product development, contributing to a diverse and competitive ecosystem.

Outlook

Despite challenges such as raw material price volatility and regulatory complexity, the global dog food market remains well-positioned for sustained growth. Increasing pet humanization, expanding e-commerce adoption, and continuous innovation in nutrition and sustainability will continue to define the industry’s trajectory through 2035.