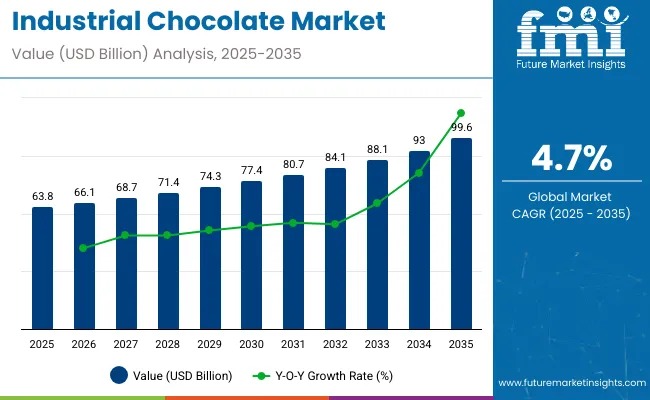

The global industrial chocolate market is entering a phase of steady, innovation-led expansion. Valued at USD 63.8 billion in 2025, the market is projected to reach USD 99.6 billion by 2035, growing at a CAGR of 4.7% over the forecast period. Industrial chocolate, a critical input for bakery, confectionery, dairy, and beverage manufacturers, continues to gain traction as brands balance indulgence with functionality, sustainability, and evolving consumer expectations.

Demand growth is underpinned by the rising use of chocolate as a versatile base ingredient across mass-market and premium food applications. From cakes and pastries to ice creams, fillings, coatings, and beverages, industrial chocolate remains indispensable for delivering taste, texture, and visual appeal at scale. Manufacturers are increasingly favoring high-quality cocoa derivatives to meet the growing appetite for premium, organic, and ethically sourced chocolate products.

Explore trends before investing – request a sample report today!

Market Snapshot Highlights

- Market Value (2025): USD 63.8 billion

- Forecast Value (2035): USD 99.6 billion

- Forecast CAGR (2025–2035): 4.7%

- Top Product Segment (2025): Cocoa butter (42.3% share)

- Top Application Segment (2025): Bakery (56.6% share)

- Fastest-Growing Market: China (6.1% CAGR)

Cocoa Butter and Bakery Applications Anchor Market Growth

By product type, cocoa butter dominates the industrial chocolate market, accounting for 42.3% of global value share in 2025. Its superior melting behavior, mouthfeel, and compatibility with premium chocolate formulations make it a preferred ingredient across bakery, confectionery, dairy, and even cosmetics. Rising demand for smooth-textured, high-cocoa-content chocolate has further strengthened cocoa butter consumption, particularly among premium and artisanal brands.

Cocoa liquor follows closely with a 35.0% share, supported by the expanding popularity of dark and high-cocoa chocolates. Increased awareness of antioxidants and perceived cardiovascular benefits has pushed food manufacturers to increase cocoa liquor content in finished products, reinforcing demand across both mass and specialty segments.

From an application perspective, the bakery segment leads with a commanding 56.6% share in 2025. Industrial chocolate is widely used in cakes, pastries, cookies, brownies, and fillings, making bakeries the single largest demand center globally. Growth in premium baked goods, café culture, and home baking trends—amplified by social media—continues to sustain volume expansion. Ice cream and frozen desserts account for 18% share, driven by consumer preference for indulgent chocolate coatings, inclusions, and plant-based frozen treats.

Premiumization, Technology, and Sustainability Shape Industry Strategy

Chocolate consumption patterns are shifting toward single-origin, bean-to-bar, and specialty formulations, a trend accelerated by small and mid-sized manufacturers seeking differentiation. At the same time, multinational players are investing heavily in R&D to reduce sugar, enhance heat resistance, and develop dairy-free and functional chocolate solutions without compromising taste.

Technological advancements in precision formulation, automation, and AI-driven process optimization are helping manufacturers increase throughput while managing costs. Sustainability has moved from a value-add to a baseline requirement, with certifications such as Fairtrade, Rainforest Alliance, organic, halal, and kosher becoming essential for global market access and brand credibility.

Regional Dynamics Highlight Asia Pacific Momentum

While North America and Europe remain high-volume, mature markets supported by strong confectionery and bakery industries, Asia Pacific is the fastest-growing region. Urbanization, rising disposable incomes, and westernized food habits are accelerating demand, particularly in China and South Korea. China stands out with a 6.1% CAGR, fueled by premium dessert chains, e-commerce penetration, and increasing preference for imported and ethically sourced chocolate ingredients.

Emerging markets including India, Indonesia, Brazil, and South Africa currently show lower per capita industrial chocolate consumption, but the gap is narrowing as global food brands expand processing capacity and quick-service restaurants scale operations.

Risk Factors and Forward Outlook

Despite positive fundamentals, the market faces challenges from cocoa price volatility, climate-related supply risks, and tightening regulatory standards on food safety and labeling. Compliance with sustainability and traceability requirements adds cost pressure, particularly for smaller players. In parallel, shifting consumer preferences toward sugar-free, plant-based, and functional products demand continuous innovation and investment.

Looking ahead, the industrial chocolate market is expected to benefit from the convergence of indulgence, health, and sustainability. Manufacturers that combine ethical sourcing, advanced processing technologies, and agile product development are well-positioned to capture growth opportunities through 2035.

Competitive Landscape

The market features a blend of global leaders, specialized cocoa processors, and emerging premium players. Companies such as Barry Callebaut, Cargill, Nestlé, Mars Inc., Blommer Chocolate Company, Olam Food Ingredients, Puratos Group, Mondelez International, The Hershey Company, and Fuji Oil Holdings continue to shape competition through vertical integration, innovation, and strategic acquisitions. As plant-based, functional, and traceable chocolate solutions gain prominence, competitive intensity is expected to rise across the decade.