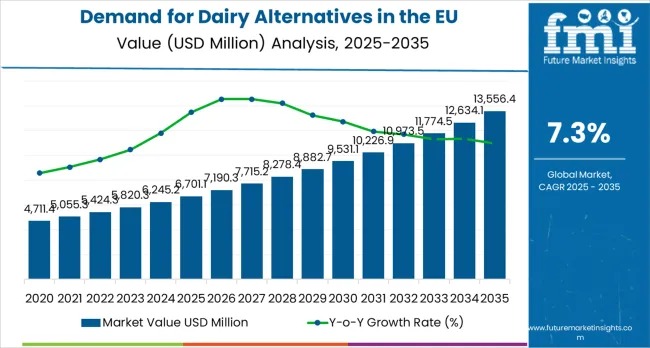

The European Union dairy alternatives market is entering a decisive growth phase, driven by structural shifts in consumer diets, sustainability priorities, and rapid product innovation. Sales are projected to rise from USD 6,701.1 million in 2025 to USD 13,556.4 million by 2035, representing an absolute increase of USD 6,701.7 million and total market growth of 100.0%. Demand is forecast to expand at a CAGR of 7.2% over the decade.

According to FMI’s latest food and ingredients intelligence, widely cited across health and nutrition studies, the EU dairy alternatives industry is expected to double in size as flexitarian eating becomes mainstream. Rising lactose intolerance awareness, ethical consumption, and expanding use cases across non-dairy milk, yogurt, cheese, ice cream, and butter alternatives continue to push the category beyond niche positioning into everyday consumption.

Explore trends before investing – request a sample report today! https://www.futuremarketinsights.com/reports/sample/rep-gb-27160

Market at a Glance: EU Dairy Alternatives

- Market Value (2025): USD 6,701.1 million

- Forecast Value (2035): USD 13,556.4 million

- Forecast CAGR (2025–2035): 7.2%

- Leading Product Type: Non-dairy milk (55.0% share)

- Top Application: Retail / at-home consumption (70.0%)

- Key Growth Markets: Germany, Netherlands, Italy

Between 2025 and 2030, demand is expected to climb to USD 9,503.6 million, accounting for 41.8% of total decade growth. This phase reflects rapid household adoption, wider product availability, and improving taste and texture parity with conventional dairy. From 2030 to 2035, sales are forecast to add USD 3,899.8 million, representing 58.2% of total growth, supported by foodservice expansion, premiumization, and precision fermentation technologies.

Why Demand Is Rising Across Europe

EU consumers increasingly rely on dairy alternatives as direct functional replacements for milk and dairy-based foods. Products must now deliver comparable performance—such as coffee foaming, yogurt creaminess, and cheese melting—rather than serving as occasional substitutes.

Growth is reinforced by:

- Expanding flexitarian, vegetarian, and vegan populations

- Rising concerns around lactose intolerance, cholesterol, and allergies

- Heightened awareness of dairy’s environmental footprint

- Stronger regulatory clarity on labeling, safety, and fortification standards

Sustainability credentials, ethical sourcing, and transparent nutritional profiles—particularly calcium, vitamin D, and B12 fortification—are becoming decisive purchase factors.

Product Trends: Beyond Non-Dairy Milk

Non-dairy milk remains the category backbone, holding 55.0% market share in 2025, though its share is projected to ease to 48.0% by 2035 as faster-growing segments mature. Oat, soy, almond, coconut, rice, and emerging pea- and cashew-based options dominate retail shelves, with barista-grade formulations fueling café demand.

Meanwhile, plant-based yogurt and cheese are the fastest-growing categories. Yogurt is expected to increase its share from 15.0% to 17.0%, while plant-based cheese expands from 12.0% to 16% by 2035. Improvements in fermentation, emulsification, and protein structuring are closing historic gaps in taste and texture, enabling broader consumer acceptance.

Key innovation drivers include:

- Precision fermentation for dairy-identical proteins

- Improved melting and cooking performance in cheese alternatives

- Probiotic and protein fortification in yogurts

Application and Channel Dynamics

Retail (at-home) consumption dominates with a 70.0% share in 2025, reflecting routine household integration. While this share is expected to moderate to 65.0% by 2035, absolute retail sales continue to rise as foodservice adoption accelerates.

Supermarkets and hypermarkets account for 35.0% of sales, benefiting from mainstream visibility and promotional pricing. Online retail is gaining momentum, projected to grow from 25.0% to 30.0% share, supported by convenience, subscriptions, and direct-to-consumer models.

Conventional dairy alternatives lead with 70.0% share in 2025, but organic products are expanding rapidly, expected to reach 40.0% share by 2035, driven by premium positioning and European organic preferences.

Country Outlook: Germany Leads Growth

Germany is the EU’s strongest growth market, forecast to expand at an 8.8% CAGR through 2035. A mature vegan ecosystem, strong retail penetration, and high environmental awareness underpin demand. The Netherlands follows at 6.0% CAGR, leveraging sustainability leadership and food-tech innovation, while Italy grows at 5.9%, supported by urban adoption and strong coffee culture.

France and Spain each post 5.8% CAGR, reflecting gradual dietary shifts despite traditional dairy cultures. The rest of Europe grows steadily as dairy alternatives gain normalized acceptance.

Competitive Landscape

The EU dairy alternatives market remains highly fragmented, creating room for differentiation. Danone (Alpro) leads with approximately 15.0% share, supported by scale, brand trust, and broad product coverage. Oatly holds around 7.0%, driven by oat specialization and strong café partnerships. Other players—including Nestlé, Unilever, and emerging fermentation startups—collectively account for 78.0%, highlighting ongoing innovation and competitive intensity.

Key Players

- Danone (including Alpro)

- Oatly

- Nestlé

- Unilever

- Freedom Foods Group Ltd.

- Living Harvest Foods Inc.

- The Whitewave Foods Company

- Earth’s Own Food Company Inc.