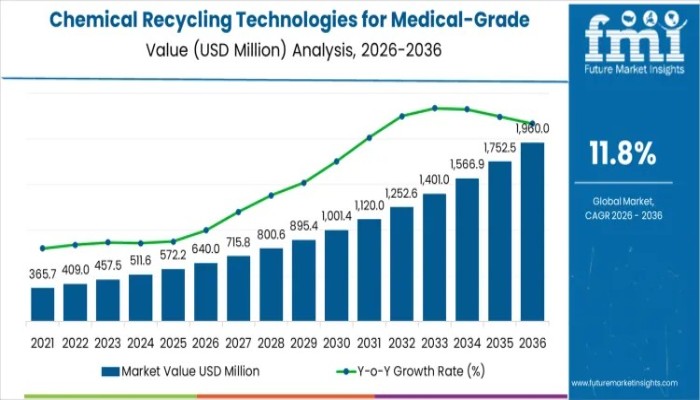

The global Chemical Recycling Technologies for Medical-Grade Plastics Market is entering a decade of accelerated and compliance-driven growth as healthcare systems, regulators, and material suppliers align around safer circularity. Valued at USD 640 million in 2026, the market is projected to reach USD 1,960 million by 2036, expanding at a robust CAGR of 11.8%.

This growth reflects not only rising volumes of medical plastic waste, but also a structural shift toward recycling technologies capable of meeting the exceptional purity, traceability, and performance requirements of medical and pharmaceutical applications.

Unlike conventional recycling segments, this market is shaped less by sheer processing capacity and more by regulatory readiness. Certification timelines, validation testing, contamination controls, and documentation standards significantly raise entry barriers.

Discover Market Opportunities – Get Your Sample of Our Industry Overview Today!

As a result, firms with established regulatory pathways and audit-ready operations are progressing faster, while smaller or newer technology providers face longer commercialization horizons. Over time, this dynamic is concentrating value among suppliers that integrate regulatory management directly into technology deployment.

Market Snapshot and Quick Stats

Key Market Metrics

- Market Value (2026): USD 640 million

- Forecast Value (2036): USD 1,960 million

- Forecast CAGR (2026–2036): 11.8%

- Leading Technology: Sterile-grade chemical recycling

- Key Growth Regions: Asia Pacific, Europe, North America

- Top Players: Eastman, BASF, Wanhua Chemical, GAIL, Teijin, Dow

Growth Trajectory: From Validation to Scale

Between 2026 and 2031, the market expands from USD 640 million to USD 997 million, reflecting controlled, compliance-led growth. This phase is defined by pilot-to-commercial transitions, early hospital and medical device partnerships, and cautious regulatory approvals for recycled content. Growth remains steady rather than explosive, as healthcare buyers prioritize risk mitigation and certification continuity.

From 2031 to 2036, expansion accelerates markedly, with the market rising from USD 997 million to USD 1,960 million. Larger facilities, standardized recycling protocols, and broader regulatory acceptance support faster compounding. Chemical recycling becomes more deeply integrated into medical-grade polymer supply chains, enabling higher processing volumes without compromising safety or consistency.

What Is Driving Market Expansion?

Growth is driven by the unique performance demands of healthcare plastics. Mechanical recycling often degrades polymer properties, making outputs unsuitable for sterile packaging, surgical devices, and pharmaceutical components. In contrast, chemical recycling technologies including solvolysis, pyrolysis, and depolymerization—break plastics down into monomers or intermediates that can be reprocessed to near-virgin quality.

At the same time, environmental policy initiatives and healthcare sustainability commitments are reshaping waste management strategies. Regulators are pushing to divert medical plastics from incineration and landfill, while hospitals and device manufacturers are setting circularity targets that do not compromise patient safety. Advances in feedstock segregation, contamination control, and process design are improving economic viability, encouraging investment in medical-grade recycling infrastructure.

Leadership by Plastic Type

Dominant Plastic Segments

- PP, PE, and PVC account for ~50% of demand

- Widely used in syringes, IV bags, tubing, trays, and protective equipment

- Provide consistent, high-volume waste streams suitable for chemical recycling

Chemical recycling is favored for these polymers because it overcomes contamination and additive challenges that limit mechanical methods. Medical-grade PP and PE form a strong secondary segment, particularly in disposables requiring sterility and mechanical reliability.

Leadership by Technology

Why Sterile-Grade Technologies Lead

- ~55% market share

- Combine depolymerization with validated sterilization and contaminant destruction

- Meet regulatory requirements for infectious and biohazardous waste

Hospitals and waste processors prioritize systems that deliver regulatory confidence, reproducibility, and audit readiness. Other technologies—such as high-volume processing or decontamination-focused systems—play supporting roles but lack the same level of medical approval compatibility.

Regional Demand Highlights

Country-Level CAGR (2026–2036)

- India: 14.0%

- China: 13.0%

- USA: 10.6%

- Germany: 9.2%

- Brazil: 9.0%

- India and China lead growth through rapid healthcare expansion, rising medical plastic consumption, and government support for recycling infrastructure.

- The United States balances sustainability goals with operational efficiency, driven by hospitals and medical device manufacturers seeking FDA-compliant recycled inputs.

- Germany reflects compliance-led adoption under stringent EU regulations.

- Brazil shows steady growth centered on established recycling hubs and industrial zones.

Competitive Landscape: Credibility Over Capacity

Competition in this market is defined by validation strength, risk control, and supply integrity rather than speed or scale alone.

Established Leaders

- Eastman and BASF leverage deep regulatory experience, closed-loop systems, and institutionalized process controls.

- Teijin emphasizes molecular consistency and material purity for high-risk medical applications.

Emerging and Pilot-Focused Players

- Wanhua Chemical integrates recycling into domestic polymer value chains, focusing on gradual compliance alignment.

- GAIL advances pilot projects to evaluate long-term regulatory and waste management potential.

- Dow maintains a partnership-driven, exploratory approach, preserving flexibility while assessing medical-grade opportunities.

In this environment, competitive advantage is built through long-term regulatory credibility, controlled scaling, and consistent performance across repeated validation cycles.

Why FMI: https://www.futuremarketinsights.com/why-fmi

About Future Market Insights (FMI)

Future Market Insights, Inc. (FMI) is an ESOMAR-certified, ISO 9001:2015 market research and consulting organization, trusted by Fortune 500 clients and global enterprises. With operations in the U.S., UK, India, and Dubai, FMI provides data-backed insights and strategic intelligence across 30+ industries and 1200 markets worldwide.

Contact Us:

Future Market Insights Inc.

Christiana Corporate, 200 Continental Drive,

Suite 401, Newark, Delaware – 19713, USA

T: +1-347-918-3531

For Sales Enquiries: sales@futuremarketinsights.com

Website: https://www.futuremarketinsights.com

LinkedIn| Twitter| Blogs | YouTube