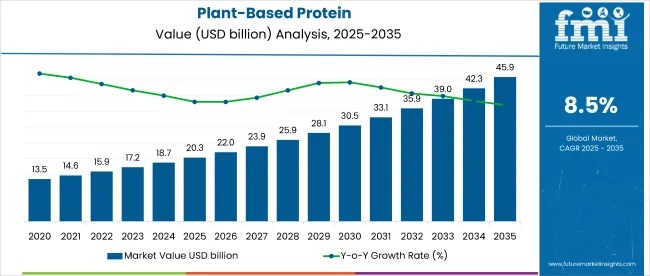

The global plant-based protein market is entering a decisive growth phase, projected to expand from USD 20.3 billion in 2025 to USD 46.0 billion by 2035, registering a robust CAGR of 8.5% over the forecast period. This acceleration reflects a structural shift in global food systems as consumers, regulators, and manufacturers converge around sustainable, ethical, and clean-label nutrition.

Plant-based proteins now account for 1.9% of the global food & beverage market and an estimated 23.4% of the protein ingredients market, underscoring their growing role in mainstream formulations. Adoption is accelerating across food & beverage, sports nutrition, dietary supplements, and convenience foods, supported by rising awareness of environmental impact, animal welfare, and long-term health outcomes.

Get Exclusive Access To Data Tables, Market Sizing Dashboards, And Analyst Insights. Request Sample Report! https://www.futuremarketinsights.com/reports/sample/rep-gb-11442

From a functional perspective, plant-based proteins contribute 11.8% of the functional food segment, 9% of sports nutrition, and 6.3% of global dietary supplements. Within vegan food formulations, their share exceeds 30%, reflecting their essential role in product structure, nutrition, and labeling. While still niche in the clean-label ingredient space, penetration has reached 4.5% and continues to climb as brands reformulate with plant-forward credentials.

Regulatory Alignment and ESG Momentum Drive Market Confidence

The market’s growth trajectory is reinforced by evolving regulatory frameworks that favor non-GMO, organic, and clean-label certifications. Governments across the USA, EU, Japan, and India are actively promoting plant-based innovation through agricultural incentives, sustainability programs, and public health guidelines. In parallel, manufacturers are aligning with ESG benchmarks, focusing on transparent sourcing, low-carbon processing, and traceable supply chains—factors increasingly influencing procurement and brand trust.

East Asia Emerges as the Growth Engine

Regionally, East Asia stands out as the fastest-growing hub, led by Japan, which is forecast to expand at a 9.1% CAGR between 2025 and 2035. Japan’s growth is underpinned by advanced food processing technologies, strong demand for functional and senior nutrition, and innovation in fermented and soy-based proteins. The USA remains the largest market by value, growing steadily at 6.1% CAGR, while the UK is projected to register 6.3% CAGR, driven by flexitarian diets and sustainability awareness.

Segment Leadership Highlights Scale and Efficiency

In 2025, soy protein is expected to dominate the product type segment with a 36.4% market share, supported by its complete amino acid profile, cost efficiency, and wide application across meat alternatives, dairy substitutes, and nutritional products. Global ingredient leaders continue to expand soy-based portfolios to meet volume and performance requirements.

By form, isolates will lead with a 41.2% market share, favored for their high protein concentration, purity, and functional versatility. Isolates are increasingly used in sports nutrition, infant formula, and functional beverages where digestibility and clean labeling are critical. From a nature standpoint, conventional plant-based proteins will maintain dominance at 78.3% share, reflecting established supply chains, economies of scale, and consistent availability for large-scale manufacturers.

Nutritional Products Anchor Demand

By end use, nutritional products will account for 19.8% of global demand in 2025, driven by sustained interest in preventive health and protein-enriched diets. Plant-based proteins are widely used in powders, bars, and supplements targeting athletes, aging populations, and wellness-focused consumers.

Consumption, Storage, and Distribution Patterns

Per-capita consumption varies significantly by region. Canada and the Netherlands show high usage of isolate-based blends in home and institutional cooking, while Japan’s urban centers favor soy and mung bean proteins. India demonstrates moderate but rising consumption through soy chunks, fortified wheat blends, and lentil formats distributed via retail and cooperatives.

The market operates a dual-format logistics model:

- Shelf-stable powders move through ambient silos

- Emulsified or rehydrated formats require chilled or frozen distribution

Countries such as Germany, Malaysia, and Brazil maintain mixed inventory systems to serve both foodservice and retail channels efficiently.

Innovation Trends and Market Challenges

Recent industry trends point to hybrid product development, combining plant-based proteins with cultured or precision-fermented ingredients to enhance taste and nutrition. Advances in extraction and fermentation technologies are also improving functional performance while reducing off-notes.

However, challenges remain. Raw material price volatility, driven by climate and geopolitical factors, impacts peas, soy, and fava beans. Additionally, digestibility and allergen concerns associated with soy and wheat require ongoing formulation innovation.

Competitive Landscape and Strategic Expansion

The market is moderately consolidated, led by global ingredient majors and specialized innovators. Companies such as Archer-Daniels-Midland, Cargill, Kerry Group, and Glanbia are investing in sustainable extraction technologies and customized formulations. European players continue to leverage locally sourced, non-GMO proteins, while North American suppliers are strengthening transparency and private-label offerings.

Recent developments include a November 2024 collaboration between Ingredion and Lantmännen to scale pea protein isolates in Europe, and BENEO’s launch of faba bean-based texturates to support hybrid and plant-based product innovation.

As global diets continue to evolve, plant-based proteins are moving beyond niche positioning to become a foundational component of future-ready food systems—combining scalability, sustainability, and nutritional performance at global scale.