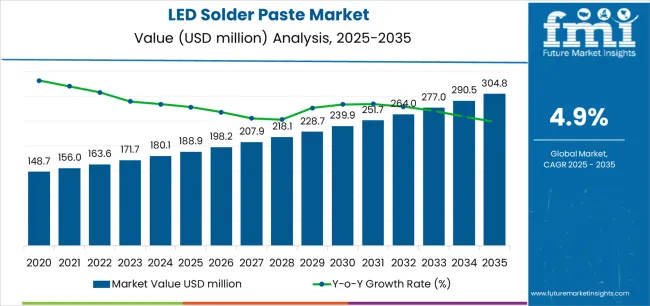

The global LED solder paste market is projected to grow from an estimated USD 188.9 million in 2025 to approximately USD 304.8 million by 2035, reflecting robust demand across diverse LED applications and a compound annual growth rate of nearly 4.9% through the forecast period. This significant expansion is being fueled by broader LED adoption in residential and commercial lighting, miniaturization trends in consumer electronics, and advanced automotive lighting requirements that collectively elevate the need for specialized soldering solutions.

As the LED industry evolves, both established players and emerging manufacturers are capitalizing on rising technology demands — reinforcing their footprints through innovation, market expansion, and tailored solutions that serve next-generation electronics assembly needs.

Market Dynamics & Growth Drivers

The LED solder paste market’s growth correlates strongly with the worldwide adoption of LED lighting across multiple sectors. LED products, from lighting panels to consumer electronics displays and automotive systems, demand high-quality solder paste capable of withstanding precise assembly conditions and stringent reliability standards. With miniaturization accelerating across consumer devices and industrial equipment alike, solder paste manufacturers are focused on flux formulations and alloy compositions that deliver consistent printability, superior thermal performance, and environmental compliance.

Across the globe, regions such as Asia Pacific, Europe, and North America are key contributors to market expansion, supported by expanding electronics manufacturing services (EMS) infrastructure and localized production capacities. These dynamics have created fertile ground for both established global specialty chemical companies and newer regional entrants seeking to capture market share through differentiated offerings tailored to specific applications.

To access the complete data tables and in-depth insights, request a sample report here

Innovation in Product Technology

A notable trend reshaping the market is the transition towards lead-free solder pastes. Environmental regulations, corporate sustainability goals, and customer preferences are driving widespread adoption of lead-free formulations that meet global compliance standards while enabling reliable joint formation across high-temperature LED assembly processes. Today, lead-free solder pastes dominate product portfolios and continue to see enhancements in alloy chemistry and flux activation to improve performance in fine-pitch applications and advanced manufacturing setups.

Simultaneously, cutting-edge developments in materials science are enabling the creation of specialized solder pastes with enhanced thermal cycling characteristics, optimized particle size distributions, and improved wetting performance. These innovations are particularly critical for automotive electronics assemblies — where reliability under harsh operating conditions is non-negotiable — and for high-precision industrial and consumer electronics where throughput and defect minimization are paramount.

Strategic Positioning of Established Leaders

Long-standing industry leaders hold significant advantage due to their deep technical expertise, global supply chains, and comprehensive product portfolios. These established manufacturers are driving growth by investing in research and development, establishing application support and service networks, and collaborating with electronics assembly partners to accelerate material qualification cycles.

Several top players in the LED solder paste market have built robust reputations by offering a blend of standard and advanced formulations, coupled with localized technical service capabilities that help manufacturers optimize their production lines. The strategic focus on quality, reliability, and compliance has sustained their leadership positions and fortified customer trust across regions and end-use segments.

Emerging Manufacturers and Competitive Landscape

Alongside traditional market leaders, a new wave of regional and niche manufacturers is gaining traction by leveraging technological agility, cost-competitive solutions, and market-specific knowledge. These emerging players are creating value through specialized product development — particularly for niche applications in industrial LED assemblies and emerging consumer technology platforms.

The competitive landscape is characterized by a mix of global chemical industry giants and smaller, specialized solder paste producers catering to unique application requirements. Many of these organizations are investing in partnerships with OEMs and EMS providers to co-develop materials optimized for localized manufacturing environments and specific product standards.

This diversification in the supplier base fosters greater competition, accelerates innovation, and ultimately drives broader adoption of advanced solder paste technologies across global markets.

Outlook and Strategic Opportunities

Looking forward, the LED solder paste market is positioned for sustained growth as LED integration expands into emerging sectors such as smart infrastructure, advanced automotive lighting, and next-generation consumer interfaces. Manufacturers focusing on application-specific solutions, eco-friendly formulations, and technical support services are expected to outperform in a market increasingly driven by performance expectations and regulatory demands.

Both established leaders and dynamic new entrants have strategic opportunities to expand their businesses by enhancing supply chain responsiveness, deepening engagement with manufacturing partners, and leveraging insights from emerging assembly trends. As electronics manufacturing technologies continue to evolve, the need for optimized soldering materials with enhanced performance, reliability, and sustainability credentials will keep innovation at the heart of competitive differentiation in this growing market.