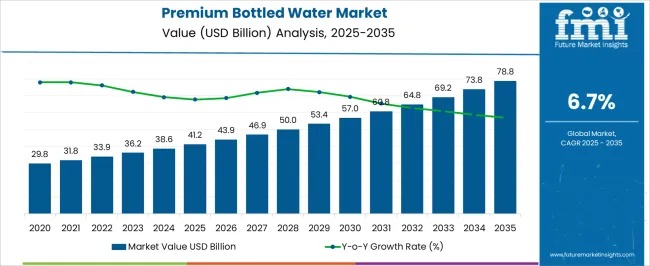

The global premium bottled water market is entering a sustained growth phase, supported by rising health awareness, premiumization across beverages, and expanding global retail reach. The market is expected to grow from USD 41.2 billion in 2025 to USD 78.8 billion by 2035, registering a 6.7% CAGR and generating an absolute dollar opportunity of USD 37.6 billion over the forecast period. This expansion reflects a clear shift in consumer behavior toward high-quality, mineral-rich, and branded hydration solutions that deliver both functional and lifestyle value.

Premium bottled water is increasingly positioned as a wellness-driven alternative to sugary drinks and carbonated beverages. Consumers are prioritizing purity, traceable sourcing, mineral composition, and premium packaging, particularly in urban markets. The rise of functional enhancements—such as added electrolytes, vitamins, and alkaline properties—along with innovations in glass and eco-friendly packaging, is further strengthening demand across both developed and emerging economies.

Get Exclusive Access To Data Tables, Market Sizing Dashboards, And Analyst Insights. Request Sample Report! https://www.futuremarketinsights.com/reports/sample/rep-gb-25948

Rolling CAGR analysis highlights the evolving nature of market growth between 2025 and 2035. From 2025 to 2028, growth remains slightly below the long-term average as North America and Europe continue volume-led expansion, supported by established consumption habits and strong brand loyalty. Between 2029 and 2032, rolling CAGR rises above the average as Asia Pacific, Latin America, and the Middle East accelerate adoption, driven by urbanization, rising disposable incomes, and premium lifestyle consumption. From 2033 to 2035, growth moderates as mature markets reach higher penetration, with incremental revenue increasingly driven by premium launches, functional variants, and brand differentiation rather than volume alone.

Market Snapshot and Demand Structure

In 2025, spring water leads the product landscape with a 28.6% share, reflecting consumer preference for naturally sourced, minimally processed hydration. From a demand perspective, the market is shaped by five major parent sectors:

- Packaged beverages (40%), driven by health- and lifestyle-conscious consumers

- Hospitality and tourism (25%), including luxury hotels, airlines, and resorts

- Retail and supermarkets (20%), offering premium accessibility for households

- Fitness and wellness (10%), integrating mineral- and electrolyte-rich water

- Foodservice and events (5%), catering to conferences and premium occasions

These sectors collectively influence branding strategies, packaging innovation, and price positioning in the global premium bottled water ecosystem.

Sustainability and Product Innovation at the Core

Recent developments underscore a strong focus on sustainability, functional differentiation, and consumer experience. Manufacturers are expanding portfolios with mineral-enhanced, flavored, and functional waters to capture wellness-oriented demand. Glass bottles, which account for 52% of packaging share, are gaining prominence due to recyclability, premium aesthetics, and taste preservation. Reduced plastic usage, recyclable PET, and reusable designs are aligning premium brands with global sustainability goals, particularly in Europe and North America.

E-commerce and direct-to-consumer channels are also reshaping distribution, offering convenience, subscription models, and broader brand discovery. Supermarkets and hypermarkets continue to dominate with a 47% share, benefiting from shelf visibility, impulse purchases, and strong retailer–brand collaborations.

Regional Growth Dynamics

Geographically, Europe accounts for over 35% of global consumption, led by France, Italy, and Germany, where mineral and sparkling water traditions remain strong. North America focuses on functional, vitamin-enriched, and alkaline water, while Asia Pacific is emerging as the fastest-growing region, supported by urbanization and rising middle-class incomes.

Country-level CAGR analysis shows:

- China at 9.0%, driven by urban consumption and e-commerce expansion

- India at 8.4%, supported by premium variants and modern retail growth

- Germany at 7.7%, shaped by sustainability and quality-driven innovation

- UK at 6.4%, led by functional and premium lifestyle segments

- USA at 5.7%, reflecting steady wellness-oriented demand

BRICS economies are driving volume expansion, while OECD markets emphasize value, branding, and sustainability.

Competitive Landscape and Strategic Focus

Competition in the premium bottled water market centers on source authenticity, brand storytelling, and packaging differentiation. Brands such as FIJI Water, Evian, San Pellegrino, Perrier, Acqua Panna, and Gerolsteiner Brunnen emphasize origin, mineral balance, and premium aesthetics. Multinationals including Coca-Cola, Danone, Nestlé, and PepsiCo leverage global distribution and marketing strength, while niche players focus on limited editions, luxury positioning, and exclusive partnerships.

Outlook

Looking ahead, the premium bottled water market is set to benefit from continued premiumization, functional innovation, and sustainability-driven branding. As consumers increasingly view water as a wellness and lifestyle product rather than a commodity, value-based growth is expected to remain resilient through 2035.