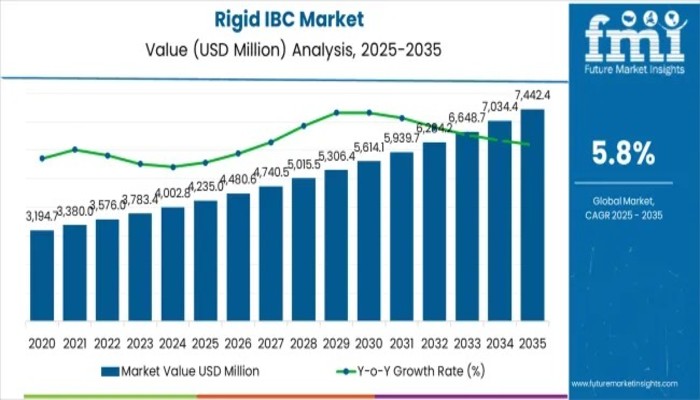

The global rigid intermediate bulk container (IBC) market is poised for a decade of robust transformation, projected to rise from USD 4,235 million in 2025 to USD 7,442.4 million by 2035, reflecting a steady CAGR of 5.8%. This expansion underscores the growing global emphasis on efficient bulk liquid handling, sustainable storage infrastructure, and reusable industrial packaging systems across chemical, pharmaceutical, food & beverage, and manufacturing sectors.

Explore Opportunities – Get Your Sample of Our Industry Overview Now!

Decade of Progressive Growth: From Transition to Transformation

FMI’s Packaging Innovation Tracker highlights two distinct growth phases defining the market’s trajectory.

- Phase 1 (2025 – 2030) marks the industry’s bulk handling adoption period, expanding from USD 4,235 million to USD 5,489 million, adding USD 1,254 million in value, and representing 39% of the decade’s total expansion. This stage is characterized by the accelerated shift from traditional drum containers to high-capacity rigid IBCs offering superior chemical resistance, reusability, and operational safety.

- Phase 2 (2030 – 2035) extends growth to USD 7,442.4 million, adding USD 1,969 million, or 61% of total decade growth, as rigid IBCs integrate seamlessly into automated filling systems, digital supply chain networks, and global logistics platforms.

This steady advancement signifies not just market growth, but a structural evolution in how global manufacturers store, transport, and manage bulk liquids, particularly within high-compliance sectors.

Regional Growth Outlook: Asia-Pacific Leads, Europe and North America Drive Innovation

- Asia-Pacific (6.7% CAGR) emerges as the fastest-growing region, with China (6.8%) and India (6.5%) driving petrochemical, specialty chemical, and food processing expansion. Both countries are leveraging industrial development programs and government incentives to scale domestic IBC manufacturing and bulk handling infrastructure.

- North America (6.2% CAGR) continues to demonstrate technological excellence, particularly in the United States, where major chemical and pharmaceutical producers adopt smart IBC systems with integrated tracking and hazmat compliance solutions.

- Europe (5.1% CAGR) maintains steady growth, led by Germany, France, and the UK, focusing on specialty formulations, pharmaceutical logistics, and sustainability compliance.

- Saudi Arabia and the broader GCC region show rising demand as industrial diversification initiatives and petrochemical capacity expansion reshape bulk chemical logistics, positioning the region as a pivotal IBC manufacturing hub by the early 2030s.

Material and Application Insights: Plastic Dominates, Chemicals Lead Demand

Plastic rigid IBCs remain the preferred choice commanding 71% of the market—due to lightweight construction, corrosion resistance, and cost efficiency. Advances in high-density polyethylene (HDPE) and composite materials have enabled superior durability and chemical compatibility.

The chemical segment, capturing 42% of total demand, remains the backbone of market growth. Increasing production of liquid chemicals, solvents, and petrochemical intermediates continues to propel global adoption. Additionally, the food & beverage and pharmaceutical sectors are expanding their use of FDA-compliant and cleanroom-validated IBCs, particularly for edible oils, flavor bases, and active pharmaceutical ingredients (APIs).

Drivers and Emerging Opportunities

Market expansion is propelled by three major forces:

- Operational Efficiency – Rigid IBCs enable bulk capacity optimization, reducing packaging waste and logistics costs while improving safety.

- Industrial Expansion – Rapid chemical production growth across Asia and the Middle East boosts large-volume storage requirements.

- Sustainability & Reusability – Circular economy initiatives favor reusable containers that minimize environmental impact and extend product lifecycles.

Emerging opportunity areas include:

- Smart IBCs with RFID and IoT tracking for real-time monitoring and regulatory compliance.

- Advanced composites with UV resistance and multi-trip durability.

- Food-grade systems catering to the global edible oil and liquid sweetener industries.

- Specialized UN-certified designs for corrosive and hazardous chemicals.

Competitive Landscape

The market remains moderately consolidated, with approximately 20 major participants controlling 45% of global share.

- Mauser Packaging Solutions, Schütz GmbH & Co. KGaA, and Greif Inc. lead through extensive global manufacturing networks and strong chemical industry partnerships.

- Emerging challengers like BWAY Corporation, Time Technoplast Ltd., and Snyder Industries are innovating in valve technology, specialty chemical resistance, and lightweight designs targeting regional chemical and industrial hubs.

Why FMI: https://www.futuremarketinsights.com/why-fmi

About Future Market Insights (FMI)

Future Market Insights, Inc. (FMI) is an ESOMAR-certified, ISO 9001:2015 market research and consulting organization, trusted by Fortune 500 clients and global enterprises. With operations in the U.S., UK, India, and Dubai, FMI provides data-backed insights and strategic intelligence across 30+ industries and 1200 markets worldwide.

Contact Us:

Future Market Insights Inc.

Christiana Corporate, 200 Continental Drive,

Suite 401, Newark, Delaware – 19713, USA

T: +1-347-918-3531

For Sales Enquiries: sales@futuremarketinsights.com

Website: https://www.futuremarketinsights.com

LinkedIn| Twitter| Blogs | YouTube