The global automotive spring market is entering a sustained phase of structural growth, backed by rising vehicle production, electrification of powertrains, and intensified focus on ride quality and vehicle stability. The market is estimated to be valued at USD 4.3 billion in 2025 and is projected to reach USD 9.0 billion by 2035, expanding at a compound annual growth rate (CAGR) of 7.5% over the forecast period.

Between 2025 and 2028, the market is expected to grow from USD 4.3 billion to USD 5.4 billion, supported by sustained vehicle production and growing replacement demand across both passenger and commercial segments. During this phase, year-on-year growth remains stable at 7.5% to 8.0%, reflecting consistent demand for stronger, lighter, and more durable suspension components.

Subscribe for Year-Round Insights → Stay ahead with quarterly and annual data updates

https://www.futuremarketinsights.com/reports/sample/rep-gb-23381

From 2029 to 2032, the market is anticipated to reach USD 7.2 billion, with annual growth in the 7.2% to 7.6% range. This mid-phase expansion is being propelled by the adoption of high-strength alloys, chromium-silicon steel, and composite spring technologies, which improve load handling, ride comfort, and fuel efficiency. By 2033 to 2035, the market is forecast to climb steadily to USD 9.0 billion, maintaining YoY growth of 7.0% to 7.4%, supported by electric vehicle (EV) suspension requirements and a resilient global aftermarket.

Springs Become Critical to EV and Lightweight Vehicle Architectures

Automotive springs are evolving from traditional mechanical components into engineered performance systems. The segment represents approximately 2.5% of the global automotive components market and contributes nearly 3.1% to the aftermarket replacement ecosystem, highlighting their strategic role in vehicle durability and chassis performance.

In heavy commercial vehicle suspension systems, springs account for around 2.8% of component value, reflecting sustained logistics and freight activity worldwide. A further 2.2% share is linked to industrial and cross-sector applications, while motorsport and performance aftermarket channels contribute roughly 3.4%, supported by rising interest in track-ready and performance-enhanced vehicles.

Coil and Steel Springs Anchor Market Leadership

Coil springs are expected to account for 36.0% of total market revenue in 2025, maintaining their position as the dominant spring type. Their compact design, adaptability, and efficient shock absorption make them the preferred solution in passenger vehicles, SUVs, and light trucks. Their cost efficiency in mass production further strengthens their penetration in high-volume OEM applications.

In terms of material, steel springs are forecast to command a 62.0% market share in 2025, driven by their high tensile strength, fatigue resistance, and proven long-term reliability. Advances in tempering, alloy composition, and surface treatment technologies have extended service life while maintaining optimal weight and structural performance. Despite rising interest in composites, steel remains the backbone of mass-market vehicle suspension due to its cost-to-performance advantage.

Passenger Vehicle Segment Remains Primary Demand Engine

Passenger cars are projected to represent 44.0% of total market revenue in 2025, reflecting high global production volumes and increasing consumer expectations for ride comfort, handling precision, and noise reduction. The shift toward electric and hybrid passenger vehicles has accelerated demand for custom-tuned spring configurations capable of managing unconventional weight distributions from battery packs and electric drivetrains.

Urbanization, higher disposable incomes in emerging economies, and evolving regulatory frameworks around fuel efficiency and vehicle stability are reinforcing long-term demand for precision-engineered springs in this segment.

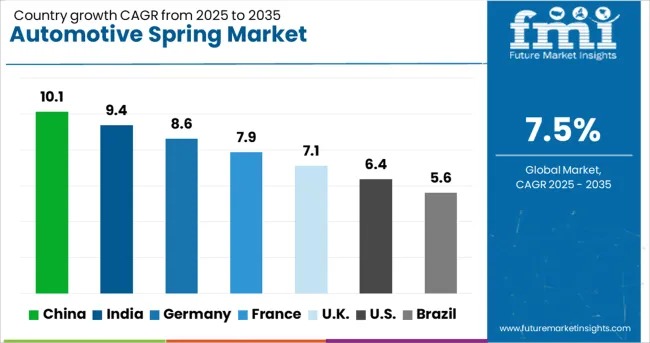

Asia-Pacific and China Lead Global Expansion

The Asia-Pacific region continues to serve as the primary growth engine for the automotive spring market. China is projected to register a 10.1% CAGR through 2035, supported by its large automotive manufacturing base, strong EV adoption, and expanding aftermarket demand.

India follows closely with a 9.4% CAGR, driven by high-volume two-wheeler production, increasing passenger car sales, and rising demand for commercial vehicles. In Europe, Germany is forecast to grow at 8.6% CAGR, benefiting from advanced engineering capabilities and strong collaboration between OEMs and suspension suppliers. The United Kingdom, at 7.1%, and the United States, at 6.4%, continue to demonstrate stable growth supported by performance vehicle demand and robust replacement cycles.

Technology Innovation Reshaping Spring Design

Technological progress is redefining spring performance and application potential. Manufacturers are deploying advanced heat treatments, precision shot peening, and corrosion-resistant coatings to improve fatigue life and durability. Composite and hybrid spring constructions are emerging, especially in EV platforms, offering substantial weight reductions without sacrificing strength.

Emerging formats, including variable-rate coil springs and electronically adjustable spring systems, are aligning with adaptive and semi-active suspension architectures. Modular spring assemblies capable of fine-tuning ride comfort and load capacity across multiple platforms are gaining adoption, particularly among global OEMs seeking scalable component strategies.

Personalize Your Experience: Ask for Customization to Meet Your Requirements

https://www.futuremarketinsights.com/customization-available/rep-gb-23381

Competitive Landscape Anchored by Engineering-Driven Leaders

The market is shaped by established global and regional manufacturers investing in material science, automation, and OEM partnerships. Leading companies include NHK Spring Co. Ltd, Sogefi Group, Mubea Fahrwerksfedern GmbH, Hendrickson USA L.L.C, Jamna Auto Industries Ltd., Rassini S.A.B. de C.V., Lesjöfors AB, Hyperco, and Tata AutoComp Systems Ltd.

Strategic priorities across these organizations include expanding production capacity near major automotive hubs, developing lighter and stronger spring alloys, and leveraging simulation-driven engineering to optimize load distribution and fatigue performance.

Outlook

The automotive spring market is transitioning into a high-value engineering segment, driven by EV platform evolution, lightweighting strategies, and heightened expectations for ride stability and durability. As vehicles become heavier, smarter, and more performance-oriented, suspension spring technologies are set to play a foundational role in next-generation chassis systems. The full market report offers detailed insights into competitive strategies, material innovations, regional dynamics, and investment hotspots shaping the global automotive spring industry through 2035.