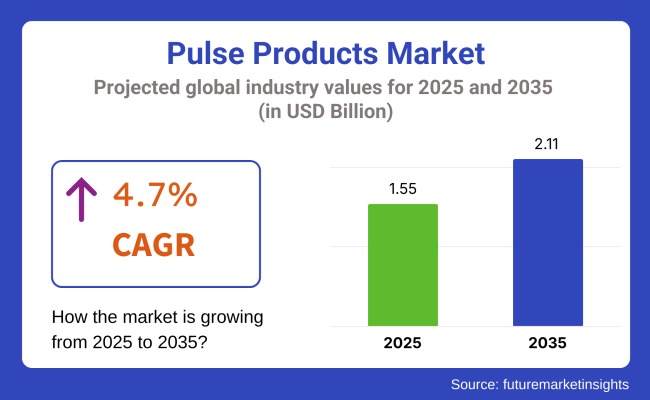

The global pulse products market is projected to grow from USD 1.55 billion in 2025 to USD 2.11 billion by 2035, registering a compound annual growth rate (CAGR) of 4.7% over the forecast period. This growth is fueled by increasing consumer preference for plant-based proteins, rising awareness of pulses’ health benefits, and the global shift toward sustainable food production and consumption.

Pulse products—including lentils, chickpeas, peas, and beans—are rich sources of protein, fiber, and essential micronutrients, making them a preferred choice among health-conscious consumers and those adopting plant-based diets. As dietary patterns globally shift toward plant-based foods for environmental sustainability and health benefits, demand for pulse-based products such as protein isolates, flours, snacks, and ready-to-eat meals is rising steadily.

Beyond vegetarian and vegan diets, pulses are gaining popularity as functional ingredients in gluten-free, low-glycemic, and high-protein foods. The use of pulse products in bakery items, meat alternatives, and processed foods is expanding, supported by pulses’ low carbon footprint and minimal resource requirements compared to animal-based proteins.

Explore trends before investing – request a sample report today!

Pulse Products Market Overview

North America and Europe currently lead the market due to high awareness of health and sustainability. Meanwhile, the Asia Pacific region is poised for the fastest growth, driven by increasing consumption in countries like India, China, and Southeast Asia, where pulses are dietary staples.

In 2024, India experienced record pulse imports of 6.63 million tonnes due to adverse weather impacting domestic production. To stabilize prices, the government removed import duties on chickpeas and extended duty-free imports of yellow peas until 2026. Additionally, India launched a six-year program to boost domestic production, including increased Minimum Support Prices (MSP) and development of heat-tolerant pigeon pea cultivars. The Indian pulse market is expected to grow at a CAGR of 5.38%, reaching 60 million tonnes by 2033.

Chickpeas Lead Pulse Products Market

Chickpeas are set to capture 45% of the pulse products market in 2025 due to their rich nutritional profile. High in essential minerals such as zinc, iron, phosphorus, and magnesium, chickpeas are valued for supporting balanced diets. Their fiber content also contributes to controlling blood sugar levels and lowering cholesterol, appealing to a global base of health-conscious consumers.

Chickpeas are used in soups, salads, snacks, and plant-based protein alternatives. Chickpea flour is increasingly popular in gluten-free products, reinforcing chickpeas’ dominance in both processed and whole-food segments.

Food & Beverages Dominate Application Segment

The food and beverage sector holds a 53% share of the pulse products market, driven by the versatile applications of pulse starch in pasta, noodles, soups, sauces, meat and poultry products, pastries, and confections. Pulse starch offers functional benefits such as gel texturization, binding, coating, and thickening, making it an attractive alternative to traditional starches like corn or potato.

As consumer preferences shift toward clean-label, plant-based, and functional foods, pulse starch is increasingly adopted for its sustainable and versatile properties.

Key Market Trends

- Rising Demand for Convenience: Hectic lifestyles, increasing nuclear families, and higher disposable income are boosting demand for ready-to-eat (RTE) foods, soups, snacks, and bakery items made from pulse products.

- Growing Health Consciousness: Sociodemographic changes and the adoption of pulse proteins in various food and beverage products are driving market growth, while environmental concerns over animal-based proteins support pulses as a sustainable alternative.

Market Players and Competitive Landscape

- Tier 1 Companies – Industry leaders hold a 50% market share, recognized for extensive product portfolios, high production capacity, and broad geographic reach.

- Tier 2 Companies – Mid-size players with a 30% share influence regional markets through solid business acumen and regulatory compliance.

- Tier 3 Companies – Small-scale businesses focus on niche local markets, holding a 20% share, often in unorganized sectors with limited formal structure.

Regional Insights

The USA, Japan, and India are among the top consumers of pulse products, recording CAGRs of 6.7%, 7.5%, and 5.3% respectively through 2035.

- USA: Rising consumer spending, growing snack food industry, and demand for plant-based protein are driving continued dominance in North America. Ancient grains like chia, quinoa, and amaranth are also gaining popularity among health-conscious consumers.

- India: The market is fueled by increasing health awareness, government initiatives, and rising demand for protein-rich foods despite challenges such as high production costs and climatic variability affecting crop yields.

- Japan: Consumption of pulses and legumes has more than doubled over the last decade, supported by the growing popularity of plant-based diets and health-focused food choices.

Leading Global Pulse Product Suppliers

ADM, Ingredion Incorporated, AGT Food and Ingredients, Buhler AG, GPA Capital Food Pvt Ltd, Diefenbaker Spice & Pulse, USA Pulses, Vestkorn, Puris, Batory Foods, Groupe Emsland, The Scoular Company, Popular Pulse Products Pvt. Ltd., Roquette Frères.

With innovations in product development, rising consumer demand for nutritious and sustainable foods, and supportive government initiatives, the global pulse products market is poised for sustained growth through 2035.