The global drone warfare market is entering a high-growth phase, propelled by the rapid integration of artificial intelligence, autonomous navigation, and network-centric combat capabilities. The market is valued at USD 29.2 billion in 2025 and is forecast to reach USD 75.8 billion by 2035, expanding at a 10.0% compound annual growth rate (CAGR). This trajectory reflects a structural shift in global defense strategies, where unmanned systems are becoming central to intelligence, surveillance, and precision strike missions.

Between 2025 and 2030, the market is expected to expand from USD 29.2 billion to USD 47.1 billion, adding USD 17.9 billion in new value. This early-stage growth is being driven by accelerated procurement cycles across the Middle East, Eastern Europe, and Asia-Pacific, as national defense programs prioritize long-range UAV platforms, border security enhancements, and rapid ISR modernization. From 2030 to 2035, market growth intensifies, rising from USD 47.1 billion to USD 75.8 billion, adding a substantially larger USD 28.7 billion. More than 60% of absolute market gains are projected to materialize after 2030, underscoring the long-term strategic importance of autonomous combat and swarm-capable drone platforms.

Subscribe for Year-Round Insights → Stay ahead with quarterly and annual data updates

https://www.futuremarketinsights.com/reports/sample/rep-gb-23282

This acceleration is largely attributed to the emergence of AI-enabled autonomous drones, coordinated swarm architectures, and hypersonic-capable unmanned platforms, which command higher unit costs and deliver superior operational impact. Semi-autonomous systems remain widely deployed, but fully autonomous capabilities are gaining rapid acceptance in strike and multi-domain combat scenarios, reshaping force structures across major defense markets.

Drone Warfare’s Expanding Role in Modern Defense Platforms

Drone warfare systems now account for 34-42% of the broader military unmanned aerial systems (UAS) market, highlighting their central position in modern warfighting. Within battlefield intelligence, surveillance, and reconnaissance (ISR) platforms, drones represent approximately 50-52% of total deployments, driven by the dominance of fixed-wing, high-endurance systems. Strike-capable drones capture 30-35% of the armed UAV category, reflecting increased global adoption of precision-strike unmanned combat aerial vehicles (UCAVs).

The tactical loitering munition segment contributes 10-15%, offering highly mobile, short-range strike capability, while ground control systems and support infrastructure represent 5-8%, enabling mission coordination, secure communications, and real-time data processing. These figures illustrate how drone warfare technologies are now tightly interwoven into global military modernization frameworks.

Segment Leadership: Combat-Ready, Medium-Range, Autonomous

Combat drones lead the market by type, accounting for 33.0% of global revenue in 2025. Their dominance is driven by their unique ability to conduct real-time surveillance while delivering precision-guided munitions without exposing pilots to hostile environments. Defense programs in the United States, China, Israel, and Turkey are accelerating investment in next-generation stealth-enabled UCAVs, embedding AI-assisted targeting and autonomous decision-making modules to increase battlefield effectiveness.

By range, medium-range drones (150-650 km) dominate with a 42.0% share, reflecting their optimal balance of endurance, operational flexibility, and cost efficiency. These platforms are widely deployed in border patrol, maritime surveillance, and counter-insurgency operations, where persistence and rapid redeployment are critical.

In terms of operational mode, autonomous drones are projected to command 61.0% of the market in 2025, marking a fundamental transition away from human-in-the-loop systems. Autonomous platforms now conduct adaptive flight routing, real-time target tracking, and collaborative swarm coordination, significantly reducing response time and operator workload in high-risk combat theaters.

Global and Regional Growth Dynamics

North America continues to lead global deployment, accounting for 34-41% of the market, supported by strong industrial capabilities and advanced defense infrastructure. Europe holds 20-25%, driven by NATO-aligned modernization programs and collaborative UAV initiatives. Asia-Pacific represents 30-35% of global demand and remains the fastest-growing region, underpinned by rising defense budgets and domestic manufacturing strategies.

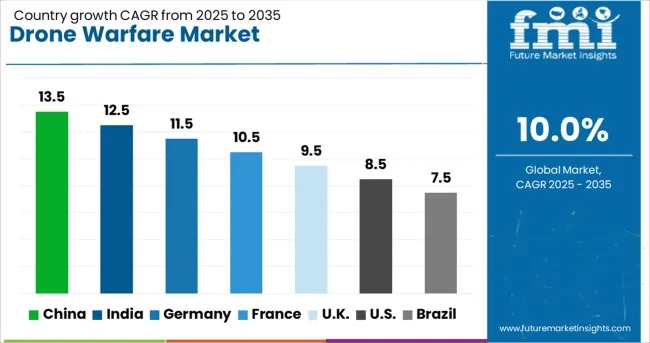

Country-level growth highlights strategic shifts in defense priorities:

China leads global growth with a 13.5% CAGR, fueled by domestic manufacturing, high-altitude long-endurance (HALE) platforms, and rapid UCAV expansion.

India follows at 12.5% CAGR, supported by indigenous drone warfare programs, swarm deployment testing, and accelerated avionics localization.

Germany is forecast to grow at 11.5% CAGR, driven by NATO interoperability programs, modular drone fleets, and encrypted communications development.

The United Kingdom expands at 9.5% CAGR, primarily through fleet modernization, AI-enabled targeting systems, and allied export partnerships.

The United States registers 8.5% CAGR, reflecting a mature market focused on software upgrades, counter-drone systems, and interoperability enhancements.

Technology Evolution and Battlefield Transformation

Rapid innovation is reshaping drone warfare architectures. Advances in AI-driven navigation, embedded payload analytics, and impact sensing are enabling drones to perform complex missions with reduced latency. Hybrid and battery-powered propulsion systems are enhancing endurance and operational flexibility, while solar-powered variants are emerging for extended surveillance applications.

Swarm technologies are redefining tactics by enabling coordinated, multi-drone operations that overwhelm traditional air defenses and enhance mission resilience. At the same time, counter-drone technologies, including directed-energy weapons and electronic warfare-resistant communication links, are being rapidly integrated to mitigate emerging threats.

Personalize Your Experience: Ask for Customization to Meet Your Requirements

https://www.futuremarketinsights.com/customization-available/rep-gb-23282

Competitive Landscape and Industry Innovation

The drone warfare market remains highly competitive, led by established defense technology leaders. Northrop Grumman Corporation continues to dominate high-altitude ISR platforms through advanced autonomous mission systems. Raytheon Technologies strengthens drone lethality through precision payloads and electronic warfare integration. Israel Aerospace Industries (IAI) maintains strong global presence with modular, long-range platforms, while General Atomics Aeronautical Systems continues to expand the operational reach of its armed UAV portfolio.

Innovation-focused players such as Teledyne FLIR, AeroVironment, Inc., and Boeing are advancing thermal imaging, tactical strike drones, and autonomous swarm-enabled combat platforms, respectively. Emerging startups across Europe and Asia are also reshaping procurement cycles by offering modular, cost-efficient drone systems.

Outlook

With rising geopolitical tensions, rapid technological advancement, and sustained defense modernization programs, the drone warfare market is entering a decisive growth era. The convergence of AI, autonomy, and swarm intelligence is no longer experimental-it is becoming foundational. As militaries worldwide transition toward lighter, smarter, and more autonomous combat architectures, drone warfare systems are positioned as a central pillar of future defense capabilities, presenting substantial opportunities for organizations seeking deeper strategic insights and market intelligence.

Why Choose FMI: Empowering Decisions that Drive Real-World Outcomes: https://www.futuremarketinsights.com/why-fmi

About Future Market Insights (FMI)

Future Market Insights, Inc. (FMI) is an ESOMAR-certified, ISO 9001:2015 market research and consulting organization, trusted by Fortune 500 clients and global enterprises. With operations in the U.S., UK, India, and Dubai, FMI provides data-backed insights and strategic intelligence across 30+ industries and 1200 markets worldwide.