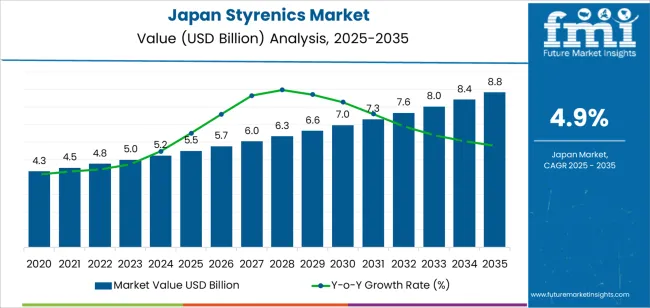

The Japan styrenics market is projected to reach a total value of USD 8.8 billion by 2035, up from USD 5.5 billion in 2025, supported by a strong compound annual growth rate (CAGR) of 4.9% over the forecast period. This optimistic outlook reflects robust demand from end-use sectors such as packaging, automotive, electrical and electronics, and consumer goods — industries that rely on styrenic polymers for their lightweight, moldable, and cost-effective material qualities.

Styrenics — a class of versatile polymers including polystyrene, acrylonitrile butadiene styrene (ABS), and styrene butadiene rubber (SBR) — has long been a cornerstone in Japan’s advanced manufacturing ecosystem. With Japan’s global reputation for precision engineering and high-performance materials, industry adoption remains strong across a wide range of applications. As consumer expectations shift toward sustainability and advanced performance, both established market giants and new entrants are racing to innovate and capture emerging opportunities.

Market Leaders Strengthen Core Capabilities

Major established players such as Asahi Kasei Corporation, Denka Company Limited, PS Japan Corporation, Mitsubishi Chemical Corporation, and Toray Industries, Inc. continue to anchor the Japan styrenics sector with diversified product portfolios and resilient supply chains.

-

Asahi Kasei Corporation stands out with its broad range of styrenic offerings, including high-performance ABS and polystyrene grades designed for automotive interiors and electronic housings. With deep roots in materials science, Asahi Kasei continues to invest in next-generation formulations that deliver strength, heat resistance, and processing flexibility for complex molding applications.

-

Denka Company Limited remains a key supplier of polystyrene and expanded polystyrene (EPS) used extensively in food packaging and insulation applications. Its ongoing enhancements in processability and material clarity help maintain Japan’s high standards for both consumer safety and packaging performance.

-

PS Japan Corporation focuses on general-purpose and high-impact polystyrene variants, catering to diverse industries such as household appliances and protective packaging.

-

Mitsubishi Chemical Corporation brings specialty styrenic blends with enhanced weatherability and chemical resistance — attributes increasingly sought after in industrial and outdoor applications.

-

Toray Industries, Inc. leverages its polymer expertise to develop engineered styrenic blends that balance process efficiency with mechanical performance, supporting automotive, electronics, and consumer segments.

These established firms are reinforcing their market leadership through capacity expansions, R&D investments, and strategic partnerships that aim to balance performance with sustainability, particularly in recyclable and lower-emission styrenic grades.

Emerging Players and New Technologies Fuel Innovation

While legacy manufacturers maintain market share, a cohort of new and dynamic companies is emerging with fresh technologies that challenge conventional value chains. These newer players are exploring advanced styrenic formulations, including heat-resistant ABS variants, monomaterial packaging solutions, and styrenic blends designed for next-generation mobility and miniaturized electronics.

Innovation hotspots are developing around recyclable styrenic materials, where research into improved sorting technologies and circular material streams is gaining traction. These efforts support broader sustainability goals that Japanese industries are embracing, and open avenues for niche players to contribute differentiated products that reduce environmental impact.

In particular, companies focusing on thin-wall injection molding compatibility are enabling manufacturers to produce lightweight components with reduced material usage — an essential trend in both consumer electronics and automotive sectors where weight savings directly influence performance and efficiency.

Sector Growth Supported by Diverse End-Use Demand

Japan’s styrenics demand is anchored by packaging applications, which account for the largest market share due to strong food safety regulations and extensive retail networks requiring high-clarity, durable materials. Automotive applications follow closely, with styrenic polymers increasingly used for interior parts, dashboards, and engineered components that contribute to vehicle lightweighting and fuel efficiency. Electronics manufacturers benefit from styrenics’ moldability and dimensional stability in devices ranging from appliances to specialized industrial equipment.

Meanwhile, demand in construction and consumer products sectors remains stable, with lightweight panels, molded fittings, and household goods supporting baseline consumption. Across these applications, material innovation — from impact-resistant grades to enhanced recyclability — continues to shape buyer decisions and product development paths.

Future Outlook and Strategic Priorities

Looking ahead, the Japan styrenics market is expected to maintain a balanced growth trajectory by blending traditional strengths with forward-looking technology adoption. Sustainability concerns — especially in single-use plastics — and competition from alternative polymers will require both established and newer manufacturers to refine product strategies and invest in eco-conscious solutions.

Key strategic priorities for industry players include:

-

Developing recyclable and bio-based styrenic grades that meet evolving environmental standards.

-

Enhancing material performance for demanding applications in EVs, smart devices, and industrial systems.

-

Expanding production capacity and supply chain resilience to meet fluctuating global feedstock dynamics.

As the Japan styrenics landscape evolves, the synergy between heritage expertise and fresh innovation promises to unlock new business opportunities, reinforce manufacturing excellence, and support Japan’s broader industrial ambitions in a competitive global environment.