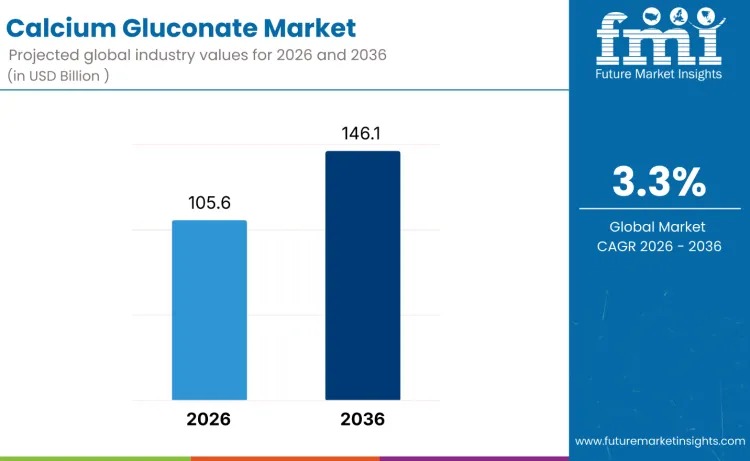

The global calcium gluconate market is estimated at USD 105.6 billion in 2026 and is projected to reach USD 146.1 billion by 2036, expanding at a steady compound annual growth rate (CAGR) of 3.3%. Market momentum is supported by increasing reliance on pharmaceutical-grade calcium gluconate, heightened focus on preventive healthcare, and expanding use of fortified foods to address widespread calcium deficiency. Long-term consumption is further reinforced by aging populations and a global shift toward healthier dietary patterns.

Calcium gluconate continues to gain preference as a safe, highly bioavailable calcium source across medical, nutritional, and food applications. Its favorable absorption profile and low risk of adverse reactions position it as a critical ingredient in intravenous therapies, supplements, and clean-label food formulations. Demand growth remains consistent across both developed and emerging markets as healthcare systems and food manufacturers prioritize reliable mineral fortification.

Explore trends before investing – request a sample report today! https://www.futuremarketinsights.com/reports/sample/rep-gb-1275

Pharmaceutical applications represent the largest share of global demand, accounting for approximately 40% of total consumption. Calcium gluconate is widely used in IV treatments for hypocalcemia, cardiac care, and magnesium toxicity management. Hospitals and drug manufacturers rely on its predictable clinical performance, high purity, and established regulatory acceptance. With rising hospitalization rates among elderly populations and increasing incidence of calcium imbalance disorders, pharmaceutical demand remains structurally strong.

Beyond clinical use, the food and beverage sector is steadily increasing adoption of calcium gluconate for fortification. Manufacturers favor the ingredient for dairy products, plant-based beverages, functional drinks, cereals, and infant nutrition due to its neutral taste, clean-label compatibility, and allergen-free profile. As consumers become more nutrition-conscious, fortified everyday foods are emerging as a primary channel to close calcium intake gaps.

The nutraceutical segment is also expanding, driven by rising sales of bone health supplements, prenatal formulations, and geriatric nutrition products. Growth in vegan and lactose-free diets has further accelerated the use of calcium gluconate as a non-dairy, highly soluble alternative. Preventive wellness trends continue to boost demand for supplements and functional foods that support long-term bone density and mineral balance.

Quick Market Snapshot (2026–2036):

- Market Value (2026): USD 105.6 billion

- Forecast Value (2036): USD 146.1 billion

- Forecast CAGR: 3.3%

- Leading Grade: Pharmaceutical grade

- Leading Application: Pharmaceuticals

- High-Growth Regions: India, USA, China

From a segmentation perspective, pharmaceutical-grade calcium gluconate dominates global demand, holding close to 40% share. This grade is essential for injectable therapies, emergency medicine, and high-purity supplement manufacturing. Food-grade material supports fortified foods and beverages, while technical-grade calcium gluconate serves agriculture, animal feed, and industrial nutrient blending. Demand distribution closely reflects regulatory standards, purity requirements, and end-use performance needs.

In terms of form, powder calcium gluconate accounts for around 62% of global demand. Powder formats offer longer shelf life, superior stability, and ease of integration into tablets, capsules, functional foods, and feed blends. Liquid forms are preferred in beverage fortification and syrup production, while injectable formulations remain indispensable in hospital and emergency care settings.

End-use analysis shows bulking agents as the largest segment, representing nearly 50% of demand. Calcium gluconate enhances structural integrity, density, and formulation stability in pharmaceuticals, nutraceuticals, and fortified foods. Direct supplementation continues to grow alongside sports nutrition, multivitamins, and deficiency correction products.

Despite positive growth fundamentals, the market faces challenges from lower-cost substitutes such as calcium carbonate and calcium citrate, particularly in price-sensitive food and supplement applications. Strict regulatory requirements for pharmaceutical-grade production also increase capital and compliance costs. However, emerging opportunities in enhanced absorption technologies, microencapsulation, vegan-certified ingredients, and innovative supplement formats—including gummies, liquid shots, and effervescent powders—are expected to support broader adoption through 2036.

Regionally, India leads global growth with a projected CAGR of 5.1%, driven by expanding hospital use, rapid supplement adoption, and government-backed food fortification programs. The United States follows at 4.8%, supported by strong pharmaceutical demand and clean-label fortification trends. China grows at 4.0% as fortified beverages and clinical nutrition scale nationwide, while the UK posts 4.5% growth linked to supplement use and plant-based beverage fortification. Japan records steadier expansion at 2.5%, reflecting its mature healthcare market and aging population.

The competitive landscape is defined by suppliers capable of delivering consistent purity, regulatory compliance, and scalable production. Key players shaping global demand include BASF SE, Koninklijke DSM N.V., Jungbunzlauer Suisse AG, Roquette Frères, GlaxoSmithKline plc, and Global Calcium Pvt Ltd. Competition increasingly centers on manufacturing efficiency, medical-grade certification, and collaboration with pharmaceutical and nutrition brands.

As preventive healthcare, fortified nutrition, and clinical calcium therapies continue to gain importance, calcium gluconate is positioned to remain a cornerstone ingredient across healthcare and food systems worldwide.