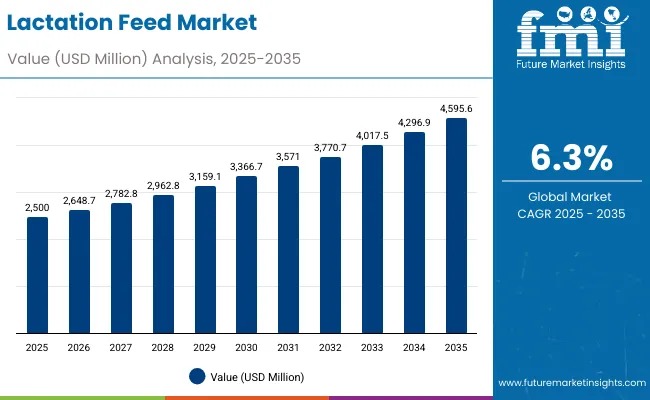

The global lactation feed market is projected to reach USD 4,595.6 million by 2035, expanding from USD 2,500 million in 2025 at a CAGR of 6.3%. The market is gaining momentum as dairy farms, livestock enterprises, and agricultural cooperatives increase their adoption of specialized feed formulations designed to enhance milk yield, reproductive performance, and overall herd health.

Rising focus on milk production efficiency, precision nutrition, and commercial dairy optimization continues to strengthen industry growth. Producers are shifting from conventional feed to structured lactation formulations that offer balanced proteins, energy-dense grains, vitamins, minerals, and advanced additives tailored to the metabolic needs of lactating animals.

Explore trends before investing – request a sample report today! https://www.futuremarketinsights.com/reports/sample/rep-gb-28560

Market Overview: Strong Demand Backed by Technological Improvements

The industry’s upward trajectory is strengthened by intensifying dairy production worldwide and a surge in nutritional science innovation. Modern processing technologies—pelleting systems, total mixed ration (TMR) units, and controlled mash preparation—ensure consistent nutrient delivery and feed quality. These systems are increasingly adopted across Europe, South Asia & Pacific, and North America, which represent the strongest growth regions.

Pellets remain the most preferred feed form, accounting for 35% market share, due to automation-ready handling and uniform nutrition. By livestock type, dairy cattle dominate the category, holding a 60% share in 2025, followed by sows as producers expand specialized lactation programs for swine.

Key Market Highlights (2025–2035)

- Market Value (2025): USD 2,500 million

- Forecast Value (2035): USD 4,595.6 million

- Absolute Growth: USD 2,095.6 million

- CAGR: 6.3%

- Leading Animal Type: Dairy cattle

- Top Regions: Europe, South Asia & Pacific, North America

- Notable Players: Cargill, De Heus Animal Nutrition, Alltech, Land O’Lakes (Purina), ADM

Growth Drivers: Why Demand Is Accelerating

Several structural forces are boosting global demand:

- Dairy Intensification:

The expansion of commercial dairy operations in India, China, France, Germany, and the United States is pushing farms toward advanced nutrition strategies. High-quality lactation feed can improve milk output by 40–60% compared with traditional mixes. - Livestock Development Programs:

Government initiatives promoting dairy modernization and rural livestock productivity—such as India’s National Programme for Dairy Development—are enhancing adoption. - Precision Nutrition & Automated Feeding:

The shift toward automated systems and nutrient-optimized feeding supported by R&D in enzymes, probiotics, and bypass fats is reshaping feed specifications.

However, the market faces challenges including ingredient price volatility, specialized formulation costs, and the requirement for consistent technical expertise among farmers in emerging markets.

Regional & Country-Level Insights

Europe leads global expansion, growing from USD 822.2 million in 2025 to USD 1,498 million by 2035 at a 6.2% CAGR.

- France shows the strongest pace at 6.4%, supported by advanced dairy technologies.

- Germany maintains market leadership with a 20% share due to extensive infrastructure and precision farming systems.

- UK follows with a 5.7% CAGR, reflecting rising emphasis on feed efficiency and animal welfare.

Asia Pacific remains a significant growth engine:

- India grows at 6.3%, driven by dairy cooperatives and rural modernization.

- China records 5.1% CAGR, backed by large-scale dairy expansion and state-led feed quality improvements.

North America remains a technology-driven market:

- USA grows at 5.6%, supported by commercial dairies deploying automated TMR systems and advanced feed formulations.

Brazil, while large in livestock, records a modest 2.3% CAGR due to mature market dynamics and cost-oriented feed adoption.

Segmental Insights: Pellets & Protein-Rich Inputs Lead Adoption

- By Feed Form:

Pellets (35%) lead due to mechanization and feed uniformity. Mash (25%) and TMR (20%) follow, while crumbles (15%) and liquids (5%) cater to specialized segments. - By Ingredient:

Grains dominate at 20%, followed by oilseed meals (18%), bypass fats (12%), vitamins/minerals (10%), and probiotics/yeast (10%).

These ingredients support energy balance, milk protein synthesis, gut health, and immune stability—critical for sustained lactation performance.

Competitive Landscape

The market remains moderately consolidated with 10–15 key players. The top five control 40–50% of global share.

Leading companies—including Cargill, De Heus, Alltech, Land O’Lakes (Purina), and ADM—are focusing on advanced formulations, R&D in metabolic nutrition, and expanded feed manufacturing capabilities. Many are strengthening partnerships with dairy cooperatives and large livestock operations to secure long-term demand.