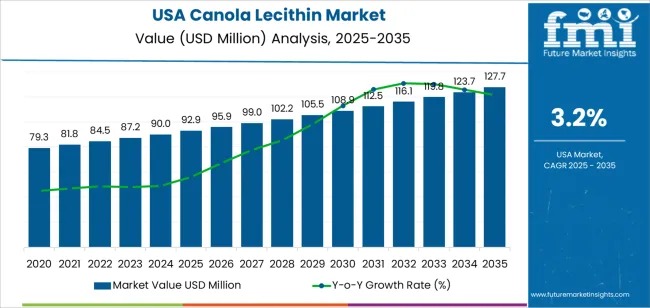

The demand for canola lecithin in the United States continues its upward trajectory, reaching a valuation of USD 92.9 million in 2025 and projected to climb to USD 127.7 million by 2035, driven by a healthy CAGR of 3.2%. As consumers increasingly prioritize clean-label products, allergen-free ingredients, and plant-based formulations, canola lecithin is rapidly gaining share as a preferred natural emulsifier across food, beverage, nutraceutical, and personal care sectors.

Explore trends before investing – request a sample report today! https://www.futuremarketinsights.com/reports/sample/rep-gb-28848

Strong Momentum Driven by Clean-Label & Plant-Based Adoption

Demand patterns show a steady expansion, rising from USD 79.3 million in the early 2020s to USD 92.9 million in 2025, and then accelerating gradually to USD 99.0 million, USD 102.2 million, and finally USD 127.7 million by 2035. This growth reflects consistent industry shifts toward natural ingredients and the reformulation of foods with non-GMO labels.

The growing appeal of canola lecithin is supported by its superior functionality—acting as an emulsifier, texturizer, and stabilizer—while offering the added advantage of being allergen-free, unlike soy lecithin.

Quick Market Insights

- 2025 Market Value: USD 92.9 million

- 2035 Forecast Value: USD 127.7 million

- Forecast CAGR: 3.2%

- Top End Use: Food & Beverages (63%)

- Key Regions: West, South, Northeast, Midwest

- Leading Companies: Cargill, Ciranda, Austrade Inc., Lecico, American Chemie

Market Forecast: Growing Preference for Natural Emulsifiers

Canola lecithin is steadily capturing share from traditional soy lecithin, powered by its non-GMO profile, cleaner sensory properties, and compatibility with vegan and allergen-free product lines. With manufacturers reformulating beverages, bakery goods, dairy alternatives, confectionery, and functional foods, the ingredient’s adoption is projected to grow consistently through 2035.

Growing health consciousness—especially regarding cholesterol management and cognitive wellness—further supports the transition to canola-based lecithin due to its choline content and favorable lipid profile.

However, price volatility in canola seeds and competition from lower-cost lecithin sources such as soy and sunflower may temper growth. The U.S. emulsifier market remains competitive, with canola lecithin expected to secure 10–12% market share over the next decade.

Why Demand Is Rising: Key Market Drivers

Growth is strongly supported by the U.S. food processing ecosystem, which is highly responsive to evolving consumer preferences. The ingredient finds broad application due to its versatility, clean-label appeal, and compatibility with organic and non-GMO certifications.

Key demand drivers include:

- Rising preference for plant-based, non-GMO, and allergen-free formulations

- Expanding use in bakery, dairy alternatives, confectionery, beverages, and nutraceuticals

- Improved processing technologies leading to higher purity lecithin grades

- Increasing adoption in personal care, cosmetics, pharmaceuticals, and animal nutrition

Available Grades Influence Adoption Trends

Canola lecithin is produced in several grades—standard, extra filtered, bleached, and hydrolyzed. Among these, standard-grade lecithin accounts for 53% of total demand, driven by its affordability and broad suitability in mainstream food applications. It is particularly valuable in improving texture, preventing separation, and enhancing shelf-life across a variety of packaged products.

Manufacturers targeting cleaner, healthier ingredient profiles increasingly prefer canola-derived emulsifiers over traditional soy-based options.

Food and Beverage Sector Leads with 63% Market Share

The food and beverages category remains the largest consumer of canola lecithin, contributing 63% of overall demand. Its role in improving viscosity, ensuring stable emulsions, and enhancing mouthfeel makes it indispensable in:

- Smoothies and energy drinks

- Dairy alternatives such as plant-based milk and yogurt

- Bakery and confectionery items

- Convenience foods including sauces, soups, and spreads

The rapid acceleration of plant-based innovation across the U.S. is expected to push this share even higher through 2035.

Regional Demand Outlook

Demand for canola lecithin is expanding nationwide, but at different paces.

- West (3.7% CAGR): Leads growth due to strong natural and organic product adoption, especially in California and Washington.

- South (3.3% CAGR): Driven by expanding food manufacturing hubs in Texas and Florida.

- Northeast (3.0% CAGR): High concentration of food processors and strong demand for non-GMO, functional ingredients.

- Midwest (2.6% CAGR): Established food production clusters and rising interest in healthier, plant-based options.

States across these regions are actively reformulating product lines to replace synthetic emulsifiers with natural alternatives like canola lecithin.

Industry Landscape: Key Companies Shaping the Market

Leading suppliers—including Cargill, Ciranda, Austrade Inc., Lecico, and American Chemie—play an essential role in scaling high-quality, non-GMO lecithin solutions tailored for food, pharma, and personal care applications. Their innovations in extraction and refining technologies continue to enhance lecithin purity and functionality.