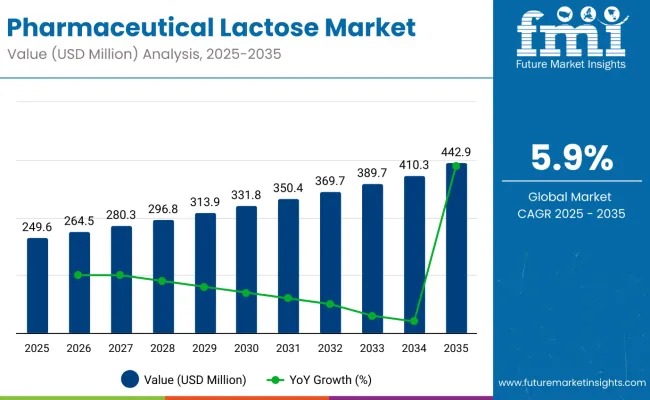

The pharmaceutical lactose market is projected to witness substantial growth during the forecast period owing to the rising demand for oral solid dosage forms, where lactose serves as a critical excipient. The market is estimated at USD 249.6 million in 2025, with an expected rise to USD 442.9 million by 2035, progressing at a 5.9% CAGR from 2025 to 2035. This trajectory is supported by the material’s extensive use as a binder and filler in tablets and capsules, alongside its compatibility, stability, and compressibility benefits widely recognized in global drug manufacturing.

Growing demand for generic drugs, expansion of OTC pharmaceutical consumption, and intensifying production in emerging economies continue to strengthen the market outlook. Tablet formulations will lead applications with a dominant 65% share in 2025, reflecting the large-scale adoption of lactose in direct compression processes for solid dosage forms.

Explore trends before investing – request a sample report today! https://www.futuremarketinsights.com/reports/sample/rep-gb-8756

Monohydrate Lactose to Maintain Its Lead in 2025

By product type, α-monohydrate lactose is expected to capture 58% of the market in 2025, supported by its stable crystalline structure, low hygroscopicity, and suitability for wet granulation and dry powder inhalation. Its high solubility and inertness make it essential for ensuring content uniformity in large-volume drug manufacturing.

A major industry milestone was announced on April 7, 2025, when MEGGLE Excipients launched three new ultra-low-nitrite lactose grades—GranuLac® 200 Low Nitrite, Tablettose® 100 Low Nitrite, and FlowLac® 100 Low Nitrite—each verified to contain no more than 0.10 ppm nitrite. This innovation directly addresses global regulatory pressure to reduce nitrosamine contamination in pharmaceutical formulations, reinforcing MEGGLE’s leadership in high-purity excipient development.

Regulatory Framework Strengthens the Need for Compliance

Pharmaceutical lactose is subject to stringent global standards, ensuring safety, purity, and consistent quality. Compliance with pharmacopeial specifications—USP, Ph. Eur., BP, and JP—is mandatory, covering parameters such as microbial limits, particle size distribution, and water content.

Key regulatory expectations include:

- GMP Compliance: Enforced by FDA, EMA, and WHO for contamination control and batch consistency.

- ISO Certification Requirements: Most producers hold ISO 9001, with some managing ISO 22000 or ISO 14001 for food safety and environmental management.

- Allergen Labeling: As lactose originates from milk, excipient manufacturers must ensure allergen transparency and protein-free processing.

- BSE/TSE Certification: Documentation verifying safe sourcing and disease-free raw materials is compulsory.

- EXCiPACT & IPEC-PQG Certification: Independent verification of excipient GMP practices supports global regulatory filings.

These frameworks ensure patient safety while enabling pharmaceutical companies to maintain cross-border compliance and smooth regulatory approvals.

Semi-Annual Market Performance Update

Market growth across forecast windows shows steady upward momentum.

Six-month CAGR comparison reveals:

- H1 2025–2035: 5.8%

- H2 2025–2035: 6.1%

This reflects a 20 BPS increase in H1 and 40 BPS in H2, signaling a healthy rise in pharmaceutical applications and excipient demand.

Risks and Market Constraints

Despite strong prospects, the industry faces challenges including fluctuating raw milk supply, stringent purity regulations, and increasing interest in lactose-free excipients. Additional concerns include:

- Climate-driven disruptions affecting dairy sourcing

- Geopolitical influences on export–import dynamics

- Rising competition from plant-based and synthetic excipients

- Growing demand for vegan-compliant drug formulations

Mitigation strategies involve supply-chain diversification, investment in advanced purification technologies, and enhanced collaboration with pharmaceutical manufacturers for customized excipient solutions.

Country-Level Growth Insights

Global growth remains strong across leading pharmaceutical hubs:

- USA: CAGR 5.8%; value USD 60.5M (2025) driven by advanced R&D and thriving generics manufacturing.

- Germany: CAGR 5.5% supported by precision manufacturing and compliance-driven innovation.

- China: CAGR 6.0% propelled by expanding domestic drug production and tightening regulatory standards.

- India: Fastest growth at 6.2%, fueled by large-scale generic drug exports.

- Japan & UK: CAGR 5.3% and 5.4%, respectively, supported by strong pharma manufacturing ecosystems.

Other markets such as France, Italy, South Korea, Australia, and New Zealand also show stable growth between 4.8% and 5.7% CAGR.

Competitive Landscape

The pharmaceutical lactose market features strong competition with leading global producers investing in purification, sustainability, and product innovation. Key players include:

- Kerry Group: 18–22% share; strong in high-purity excipients.

- DFE Pharma: 14–18%; prominent in inhalation-grade lactose.

- Meggle Group: 10–14%; expertise in spray-dried and micronized lactose.

- FrieslandCampina Domo: 8–12%; known for excipient functionality consistency.

- Armor Pharma: 6–10%; specialized in customized controlled-release lactose formulations.

These companies actively expand R&D capabilities, optimize sourcing strategies, and align with global GMP standards to maintain competitive strength.