According to Future Market Insights (FMI), the global coated fabrics market is entering a decade of sustained expansion, driven by its crucial role in automotive interiors, protective clothing, industrial applications, and architectural membranes. The market is forecast to advance from USD 50 billion in 2025 to USD 79.9 billion by 2035, reflecting a compound annual growth rate (CAGR) of 4.8%.

Polymer-coated fabrics remain the dominant material type, commanding roughly 25% of total market value, owing to their versatility, processability, and performance across multiple industrial and consumer end uses. FMI’s analysis indicates that while saturation in mature regions may begin post-2030, the market’s long-term outlook remains robust due to innovation in sustainable coatings, regional manufacturing expansion, and EV-related interior demand.

Subscribe for Year-Round Insights → Stay ahead with quarterly and annual data updates: https://www.futuremarketinsights.com/reports/sample/rep-gb-288

Automotive and Industrial Growth Anchor Global Demand

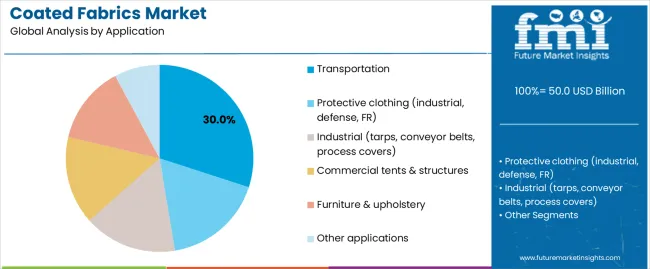

Transportation applications account for approximately 30% of total coated fabric consumption, led by seat covers, airbag fabrics, headliners, and trim materials. FMI notes that the automotive industry’s focus on lightweight, durable, and cost-effective interior materials continues to drive strong substitution away from leather toward coated alternatives.

Industrial and protective clothing applications represent another 40% of total demand, underscoring the material’s importance in worker safety, chemical protection, and flame-retardant apparel. Construction and commercial architecture contribute the remaining 25%, reflecting growing use of tensile structures, façade membranes, and industrial tarpaulins.

Regional Insights: Asia-Pacific, Europe, USA, and Saudi Arabia

Asia-Pacific (APAC) leads global consumption, accounting for approximately 40% of total demand. Within the region, China (5.3% CAGR) and India (5.1% CAGR) dominate growth, supported by expanding automotive production, infrastructure investment, and EV interior development. Local coating capacity additions and supply chain integration enhance cost competitiveness and regulatory compliance.

Europe contributes around 31% of global market revenue (USD 15.5 billion in 2025), with Germany maintaining technological leadership in automotive interiors and PTFE/silicone architectural applications. France, the United Kingdom, and Italy collectively reinforce Europe’s sustainability and design-driven coated fabric innovation, supported by REACH compliance and solvent-free chemistry transitions.

In the United States, FMI identifies architectural membrane adoption, automotive recovery, and environmental compliance as the primary growth vectors. The market’s 4.6% CAGR is propelled by solvent-free polyurethane innovations and circular economy participation across major OEM and construction supply chains.

Meanwhile, in Saudi Arabia, industrialization, infrastructure expansion, and large-scale commercial construction programs are amplifying coated fabric demand, particularly within tensile architecture, protective apparel, and logistics sectors. Supported by Vision 2030 diversification initiatives, Saudi Arabia’s coated fabrics market is evolving into a regional manufacturing and export hub for GCC applications.

Material Leadership: Polymer-Coated Fabrics Command 25% Share

FMI’s segmentation indicates that polymer-coated fabrics dominate the global market with approximately 25% value share, encompassing polyurethane (11%), low-phthalate PVC (9%), and TPU-based systems (5%). These materials are favored for their adaptability across automotive interiors, industrial tarpaulins, and furniture upholstery.

Solvent-free and water-based polyurethane systems are rapidly gaining traction, reflecting environmental regulations and corporate sustainability goals. The share of bio-attributed and recycled-content coatings in new product launches has increased to 20%, underlining a clear transition toward eco-compliant, circular chemistry solutions.

Segmental Highlights

- By Application: Transportation dominates with 30% market share, followed by protective clothing (22%), industrial (18%), commercial structures (15%), and furniture (15%).

- By Material: Polymer-coated fabrics (25%) lead, followed by rubber-coated (23%), fabric-backed vinyl (22%), silicone-coated (10%), and fluoropolymer-coated (8%).

- By Substrate: Polyester (PET) retains a 46% share, due to its dimensional stability, cost efficiency, and recyclability.

Need tailored insights? Request report customization to match your specific business objectives: https://www.futuremarketinsights.com/customization-available/rep-gb-288

Strategic Opportunity Pathways Identified by FMI

FMI’s growth outlook outlines seven major strategic pathways for coated fabric stakeholders:

- Polymer-Coated Innovation Excellence: Enhancing PU and PVC-free formulations to reduce VOCs and extend service life to 10 years.

- Transportation Leadership: Developing soft-touch, low-fogging automotive interiors aligned with EV and luxury trends.

- Sustainable Fiber Integration: Scaling recycled PET substrates and circular textile feedstocks.

- Protective Clothing Expansion: Meeting global industrial safety and flame-retardant garment standards.

- Asia-Pacific Localization: Strengthening China and India manufacturing ecosystems for automotive and infrastructure sectors.

- Bio-Attributed Chemistry: Accelerating adoption of renewable feedstock coatings for environmental compliance.

- Architectural Membrane Advancement: Advancing PTFE/PVDF-coated fabrics for stadiums, façades, and commercial roofing.

Each of these pathways collectively contributes to a USD 50–70 billion global revenue opportunity through 2035, reflecting parallel advances in coating chemistry, substrate engineering, and sustainability validation.

Competitive and Innovation Landscape

The coated fabrics industry exhibits moderate concentration, with the top 30 players commanding around 35% of the total market. FMI’s analysis shows that innovation, certification, and sustainability credentials now outweigh price competitiveness as primary differentiators.

Key technology innovators focus on solvent-free processing, low-phthalate PVC alternatives, and bio-attributed polyurethane systems. Partnerships between automotive OEMs, architectural firms, and coating technology providers are deepening across Asia-Pacific and Europe, while North American suppliers emphasize premium quality and long-term durability to maintain domestic production competitiveness.

About Future Market Insights (FMI)

Future Market Insights, Inc. (FMI) is an ESOMAR-certified, ISO 9001:2015 market research and consulting organization, trusted by Fortune 500 clients and global enterprises. With operations in the U.S., UK, India, and Dubai, FMI provides data-backed insights and strategic intelligence across 30+ industries and 1200 markets worldwide.

Why Choose FMI: Empowering Decisions that Drive Real-World Outcomes: https://www.futuremarketinsights.com/why-fmi