The global vacuum blood collection devices market is entering a period of strong growth and rapid innovation. Both well-established leaders and emerging manufacturers are expanding their reach, embracing new technologies, and reshaping the future of blood collection systems across healthcare and diagnostics.

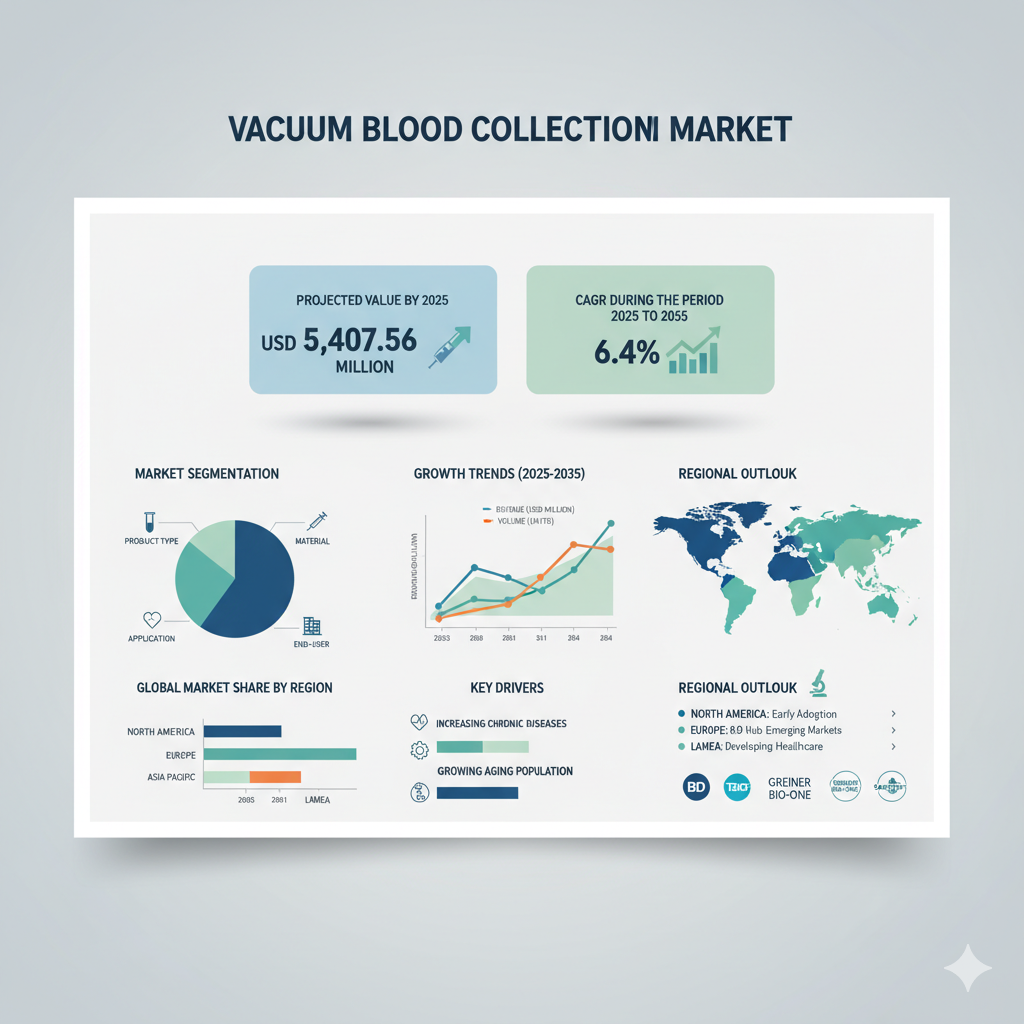

According to a new industry analysis, the global market is projected to reach USD 5.4 billion by 2035, growing at a healthy compound annual growth rate (CAGR) of 6.4% during 2025–2035. As healthcare systems evolve, advancements in automation, safety, and sustainability are becoming central to the industry’s progress.

Established Manufacturers Leading the Charge

The market continues to be led by several major global companies such as Becton, Dickinson and Company (BD), Greiner Bio-One GmbH, Cardinal Health, SARSTEDT AG & Co. KG, and Sekisui Medical Ltd. Together, these firms represent nearly half of the market’s total share and are driving technological leadership in product design and clinical safety.

BD, for instance, is leveraging its experience in developing safety-engineered devices to reduce needle stick injuries and improve healthcare worker protection. Greiner Bio-One has advanced its product line with clot-activator tubes that enable faster sample processing and better test accuracy. SARSTEDT has been focusing on enhanced plasma collection technologies that maintain sample stability — a critical factor for modern diagnostic applications.

These established manufacturers are also expanding their geographic footprints, especially in Asia-Pacific and Latin America, where rising healthcare expenditure and a growing number of diagnostic labs are fueling product demand. The next decade is expected to bring a surge of partnerships and capacity expansions as these players seek to strengthen their presence in emerging regions.

New and Emerging Manufacturers: Seizing Fresh Opportunities

At the same time, smaller manufacturers and regional companies are making their mark. Approximately 30% of the market is now held by local suppliers and mid-sized firms offering affordable, adaptable blood collection solutions tailored to regional healthcare needs. Another 20% of the market is being driven by start-ups and R&D-focused organizations developing next-generation, technology-driven sampling devices.

These emerging players are using agility as a competitive advantage — experimenting with sustainable materials, micro-sampling devices, and digital connectivity features that appeal to hospitals, clinics, and even home-testing providers. They are increasingly targeting niche segments such as veterinary diagnostics, pediatric blood collection, and portable, point-of-care systems.

The result is a highly dynamic landscape where smaller innovators complement the scale of established brands by offering flexibility, affordability, and faster development cycles. For these new entrants, success will depend on strategic collaborations with healthcare facilities, diagnostic chains, and research institutions — while keeping pace with evolving regulatory and safety standards.

Technology and Market Dynamics: The Future Takes Shape

Several major factors are steering the market’s next phase of growth:

- Rising demand for diagnostics: The increasing prevalence of chronic diseases such as diabetes, heart conditions, and cancer continues to drive the need for accurate and efficient blood collection systems.

- Material innovations: PET and other advanced plastics are rapidly replacing glass tubes, offering better durability, lighter weight, and easier disposal.

- Automation and digitalization: Integration of RFID tracking, barcode systems, and smart connectivity ensures higher accuracy in sample handling and identification, improving workflow efficiency in laboratories.

- Regional growth potential: While North America and Europe remain strongholds due to established infrastructure, countries in Asia-Pacific — especially India and China — are expected to record the fastest growth rates over the next decade.

- Regulatory compliance and safety: Companies adhering to strict quality and safety standards are gaining competitive advantage, as healthcare providers increasingly prioritize patient and clinician protection.

Together, these trends are redefining the vacuum blood collection devices industry — transforming it from a purely functional market into one centered on innovation, sustainability, and digital integration.

Strategic Outlook for Manufacturers

For established players, the future depends on continued investment in R&D, automation, and geographic diversification. Companies are expected to focus on expanding their product portfolios with connected, smart sampling systems that reduce manual intervention and error rates.

For new entrants, the pathway lies in differentiation — whether through eco-friendly materials, cost-effective local production, or partnerships with regional diagnostic providers. Many start-ups are already integrating artificial intelligence, robotics, and portable collection kits to make blood sampling more accessible and patient-friendly.

Across the board, three strategies stand out for long-term growth:

- Portfolio expansion: Introduce home-collection kits, AI-enabled tracking, and micro-sampling devices that align with global trends toward decentralized diagnostics.

- Emerging market focus: Build regional manufacturing hubs and leverage partnerships with hospitals and laboratories to penetrate high-growth regions.

- Sustainability and education: Transition toward recyclable materials, eco-friendly production, and awareness initiatives that encourage adoption of new technologies.

Conclusion

With the vacuum blood collection devices market expected to more than double in value by 2035, the coming decade represents a pivotal time for both established and emerging manufacturers. The race toward innovation, automation, and global expansion is redefining how blood samples are collected, stored, and analyzed.