The hybrid marine gensets market, currently valued at USD 190.6 million in 2025, is forecast to reach USD 485.5 million by 2035, with a robust CAGR of 9.8% over the decade. This growth is far from uniform; instead, it will unfold in waves of adoption, stabilization, and renewed acceleration. While global demand underpins this expansion, the most compelling opportunities are unfolding in Europe and the Asia-Pacific (APAC) region, where retrofit programs, emission regulations, and fleet modernization are creating fertile ground for both established manufacturers and ambitious new entrants.

In Europe, retrofit mandates in nations like Norway and Denmark and ferry modernization programs are driving steady uptake. In APAC, coastal fleet mandates in China and Korea, combined with aggressive port electrification strategies, are spurring demand—not merely in specialist vessels, but across commercial shipping, offshore support, ferries, and defense fleets alike. This is where new technology players and incumbents must focus their effort.

Growth Phases: From Early Momentum to Accelerated Gains

During the early segment (2025–2029), adoption is being led by hybrid propulsion systems aboard ferries, patrol vessels, and offshore service fleets, spurred by stringent emissions standards and operational cost pressures. Fuel savings, operational flexibility, and compliance with regulations such as IMO Tier III edges are unlocking initial gains.

Between 2029 and 2032, growth enters a more moderate phase in advanced markets, as early adopters reach saturation. Yet, retrofit cycles, second-wave adoption in defense fleets, and emerging retrofit regulations sustain steady uptake.

Post-2032, technology enhancements in battery integration, smart energy management, and modular genset blocks are projected to reignite momentum. As hybrid systems mature, they deliver more efficient battery-diesel synergy and predictive energy optimization, which unlock new value, particularly in high-utilization vessels.

This pattern implies that while the average CAGR holds at 9.8%, rolling compound growth will rise and fall in response to retrofit cycles and adoption waves.

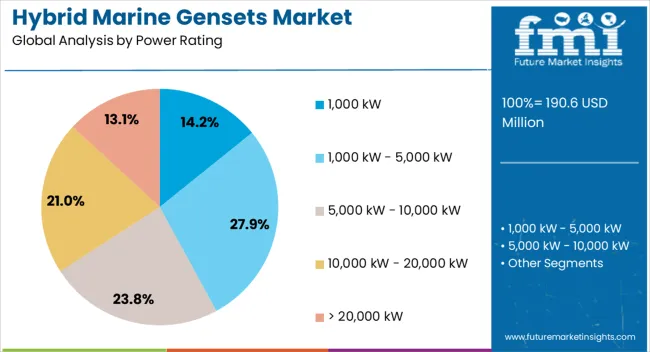

Market Structure: Segments Backing the Growth Engine

Among power ratings, the 1,000 kW to 5,000 kW segment commands the largest share (27.9%) as of 2025. This rating strikes a practical balance for large commercial vessels, offshore support ships, and ferries—vessels that demand strong continuous power and flexibility for hybrid operation. Manufacturers investing in modular platforms in this band are positioning themselves to capture a substantial portion of the addressable market.

In terms of technology, diesel-electric hybrid gensets dominate with nearly 46.7% share, thanks to their mature deployment, operational familiarity, and compatibility with existing vessel systems. The flexibility of diesel-electric systems—capable of operating engines at optimal loads while supplementing with battery power—makes them a preferred configuration for many new builds and retrofits in both Europe and APAC.

On the application front, merchant shipping leads (approx. 31.9%) given its high utilization, long voyage cycles, and growing pressure to decarbonize. Combined, commercial shipping, offshore, naval, ferries, and luxury yachts form the primary addressable sectors.

Regional data underscores APAC capturing nearly 40% of new installations, while Europe accounts for about 30%—largely via retrofit programs in Scandinavian and North Sea nations.

Challenges Remain: Costs, Integration, and Infrastructure

Upfront CAPEX remains a considerable hurdle. A hybrid retrofit can cost 20–60% more than a conventional upgrade, with batteries contributing up to 40% of that cost. Older vessels often require hull modifications, additional cooling systems, and extended maritime yard time (2 to 4 months), adding risk and expense. Battery replacement every 7 to 10 years can represent up to 25% of the initial system cost.

Infrastructure gaps threaten adoption. Many ports—especially outside Europe—lack hybrid charging compatibility: only ~35% of European ports and ~20% of U.S. ports currently support hybrid shore power. For smaller operators with limited capital, these gaps create adoption inertia.

Technical integration complexity also weighs heavily. Balancing loads among diesel engines, batteries, propulsion systems, and energy management platforms demands sophisticated control software and system design—areas where incumbents and newer technology integrators must compete.

Regional Growth Outlook: China, India, Germany Lead the Curve

China leads globally with a projected CAGR of 13.2%, enabled by robust shipbuilding, electrified vessel adoption, and port modernization. Coastal shipping routes and inland waterways are key battlegrounds for hybrid genset deployment.

India, growing at 12.3%, is quickly modernizing its ferry systems, coastal fleets, and supporting hybrid retrofits in offshore vessels, especially with state-backed clean maritime initiatives.

In Germany, predicted CAGR is 11.3%, driven by inland waterways, green shipping corridors, and retrofit programs in ports like Hamburg and Bremen. Manufacturers like MAN Energy Solutions and Rolls-Royce are actively supplying hybrid genset solutions tailored for European emission frameworks.

The UK market is expected to grow at 9.3%, driven by offshore wind support vessels, ferry services, and coastal hybrid initiatives. Ports such as Dover, Southampton, and Liverpool are focal points for deployment.

In the United States, CAGR is projected at 8.3%, with growth coming from inland waterways, offshore support vessels, and hybrid retrofits in coastal and defense fleets.

Competitive Landscape: Legacy Titans and Agile Innovators

The hybrid marine gensets market features a mix of large industrial players and agile niche innovators. ABB, Siemens Energy, Rolls-Royce, MAN Energy Solutions, Mitsubishi Heavy Industries, Nidec, Caterpillar, Cummins and BAE Systems are at the forefront, combining their power systems expertise with hybrid integration, control systems, and global reach.

These incumbents compete on system integration, modular design, after-sales service, and digital control software. Smaller firms—Fischer Panda, Steyr Motor, Scania, Anglo Belgian Corporation—carve out niches in compact designs for smaller vessels or retrofit packages. BAE, with its defense pedigree, positions hybrid systems for naval and mission-critical applications.

Partnerships among shipyards, battery manufacturers, and software providers are increasingly common, enabling quicker go-to-market for hybrid solutions. The market narrative is shifting: it’s no longer just about mechanical genset power, but the synergy of hardware, battery, and intelligent energy control.

Purchase this Report for USD 5,000 Only | Get an Exclusive Discount Instantly! https://www.futuremarketinsights.com/checkout/26106

Everything You Need—within Your Budget. Request a Special Price Now! https://www.futuremarketinsights.com/reports/sample/rep-gb-26106

About Future Market Insights (FMI)

Future Market Insights, Inc. (ESOMAR certified, recipient of the Stevie Award, and a member of the Greater New York Chamber of Commerce) offers profound insights into the driving factors that are boosting demand in the market. FMI stands as the leading global provider of market intelligence, advisory services, consulting, and events for the Packaging, Food and Beverage, Consumer Technology, Healthcare, Industrial, and Chemicals markets. With a vast team of over 400 analysts worldwide, FMI provides global, regional, and local expertise on diverse domains and industry trends across more than 110 countries.

Contact Us:

Future Market Insights Inc.

Christiana Corporate, 200 Continental Drive,

Suite 401, Newark, Delaware – 19713, USA

T: +1-347-918-3531

For Sales Enquiries: sales@futuremarketinsights.com

Website: https://www.futuremarketinsights.com

LinkedIn| Twitter| Blogs | YouTube