The global phenolic antioxidants market is projected to grow from USD 4.9 billion in 2025 to USD 8.6 billion by 2035, yielding a compound annual growth rate (CAGR) of 5.8% over the forecast period. This forward path is more than a product of rising demand—it reflects the ability of manufacturers to balance technical innovation with growing regulatory complexity. Major regulatory agencies such as the U.S. Environmental Protection Agency, the European Chemicals Agency, and their Asian counterparts impose stringent guidelines on production, handling, migration, residual content, and permissible concentration limits in food, packaging, polymer, and personal care applications. Compliance with these mandates demands rigorous monitoring, documentation, and quality systems, which increase operational overhead and complicate market entry.

Nevertheless, the market trajectory from USD 4.9 billion to USD 8.6 billion signals that many players are successfully navigating these constraints, scaling up production while innovating more sustainable and low-toxicity antioxidant solutions.

Regulatory Forces Shaping Innovation and Strategy

Regulation is not merely a barrier in this industry—it is a catalyst. As authorities tighten limits on hazardous substances and demand enhanced sustainability, companies are pivoting toward natural phenolic compounds, synergistic blends, and low-migration formulations. These alternatives often require greater R&D investment and longer development cycles, but they offer a competitive edge in markets demanding clean-label ingredients and stringent performance.

At the same time, regulatory pressure influences pricing strategies, market access, and formulation decisions. In sectors such as packaging and polymers, migration limits dictate which phenolic antioxidants may be used—and at what concentrations. This drives a premium for antioxidants that combine performance with lower residuals. Buyers of the full market report gain critical insights into how these compliance landscapes vary by region and how to structure product portfolios accordingly.

Core Drivers: Industrial Use, Material Stability, and Consumer Demand

The growth of phenolic antioxidants is rooted in their indispensable role across a range of industries. In plastics and rubber, these antioxidants prevent oxidative degradation during processing and throughout the life of the product, safeguarding tensile strength, color stability, and mechanical integrity. In lubricants and fuels, phenolic antioxidants protect oils from breakdown under heat and stress, thereby preserving performance and reducing maintenance needs. In cosmetics, food, and feed sectors, both synthetic and natural phenolic antioxidants inhibit oxidation of oils and sensitive compounds, extending shelf life and preserving quality.

Simultaneously, rising consumer awareness of product quality, oxidation damage, and sustainability is fueling demand for antioxidants derived from plant sources. This trend, coupled with regulatory incentives for lower-toxicity solutions, is pushing established players and niche manufacturers alike to invest in bio-based phenolic technologies.

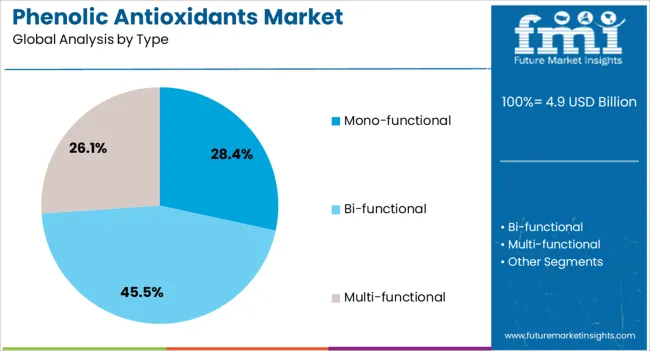

Segment Trends: Source, Type, and Form

By source, the natural phenolic antioxidant segment holds 42.7% of the market in 2025. This leadership is anchored by growing demand for sustainably derived additives with lower environmental impact and greater consumer appeal in sensitive applications like food, packaging, and personal care.

In type, mono-functional phenolic antioxidants command approximately 28.4% share. Their specialization allows for targeted, cost-effective performance where a single antioxidant function suffices rather than multifunctional blends.

By form, liquid antioxidants hold about 36.9% share. Their ease of dispersal, direct integration into production lines, and better solubility make them preferred in many polymer, emulsion, and coating systems.

In applications, demand is especially strong in the plastic & rubber, fuel & lubricants, and cosmetic & personal care segments, each contributing substantively to overall volume.

Regional Outlook and Country-Level Growth

Geographically, the Asia-Pacific region, led by China and India, exhibits the highest growth potential, with projected CAGRs of 7.8% and 7.3%, respectively. Future Market Insights These markets are bolstered by expanding polymer manufacturing, rising automotive output, and growing demand for stabilized materials in consumer goods.

In Europe, Germany leads with around 6.7% CAGR, supported by high-quality manufacturing, strict regulatory regimes, and demand for certified antioxidant solutions in performance plastics and lubricants. Future Market Insights The United Kingdom and France also register healthy growth, driven by innovation and regulatory compliance in specialty chemical markets.

In the United States, growth is steadier, estimated at around 4.9% CAGR, underpinned by demand in industrial, food, and personal care sectors and investments in advanced additive technologies.

Opportunities and Challenges for Stakeholders

For established chemical and additive giants such as BASF SE, Eastman Chemical, Lanxess AG, Afton Chemical, and Lubrizol, the challenge is to maintain technological leadership while satisfying regulatory and sustainability demands. These incumbents are already collaborating with polymer manufacturers, lubricant formulators, and specialty chemical firms to embed high-performance antioxidants deeper into industrial value chains.

At the same time, regional and niche players—such as Adeka Corporation, Chitec, Dorf Ketal, OXIRIS, and SI Group—are differentiating via specialized phenolic blends and localized supply. Their agility allows them to respond faster to end-user needs in performance, cost, or regulation-sensitive markets.

New entrants or technology-driven startups have room to compete by focusing on bio-based phenolics, encapsulation technologies, or low-odor, low-migration formulations. For buyers of the report, this presents an opportunity to identify white-space markets and partner or invest in breakthrough antioxidant technologies.

Challenges include volatility in raw materials, high regulation overhead, and the need for deep formulation expertise. Companies must invest in analytical, quality assurance, and predictive-aging tools to stay competitive.

Why Buying This Market Report Adds Value

For those considering investing, expanding, or entering this sector, the full market report delivers strategic advantage. It provides region-wise forecasts, competitive benchmarking, regulatory maps, innovation roadmaps, and barrier analyses. Whether you are an established chemical company, a specialty firm, a startup, or an investor, the insights help navigate technical, regulatory, and market-entry hurdles with more confidence.

Purchase this Report for USD 5,000 Only | Get an Exclusive Discount Instantly! https://www.futuremarketinsights.com/checkout/26068

Everything You Need—within Your Budget. Request a Special Price Now! https://www.futuremarketinsights.com/reports/sample/rep-gb-26068

About Future Market Insights (FMI)

Future Market Insights, Inc. (ESOMAR certified, recipient of the Stevie Award, and a member of the Greater New York Chamber of Commerce) offers profound insights into the driving factors that are boosting demand in the market. FMI stands as the leading global provider of market intelligence, advisory services, consulting, and events for the Packaging, Food and Beverage, Consumer Technology, Healthcare, Industrial, and Chemicals markets. With a vast team of over 400 analysts worldwide, FMI provides global, regional, and local expertise on diverse domains and industry trends across more than 110 countries.

Contact Us:

Future Market Insights Inc.

Christiana Corporate, 200 Continental Drive,

Suite 401, Newark, Delaware – 19713, USA

T: +1-347-918-3531

For Sales Enquiries: sales@futuremarketinsights.com

Website: https://www.futuremarketinsights.com

LinkedIn| Twitter| Blogs | YouTube