The global helicopter blades market is entering a period of stable yet significant expansion, projected to rise from USD 670.3 million in 2025 to USD 900.8 million by 2035, registering a CAGR of 3.0%. This forecast highlights the essential role rotor blades play in both defense and civilian aviation, as modernization programs, rising air mobility, and aftermarket services shape demand across regions.

Between 2025 and 2030, the market will see consistent growth, reaching USD 777 million by the end of that period. This early expansion reflects the sustained replacement of aging helicopters, strong defense procurement, and growing civilian applications ranging from medical evacuations to offshore operations. By 2035, steady adoption of lightweight composite blades, better vibration control technologies, and aftermarket upgrade programs will reinforce the market’s value at USD 900.8 million.

Why Helicopter Blades Are Becoming a Priority

Helicopter blades may seem like a niche within the vast aerospace sector, but they are the lifeline of rotorcraft performance. Their share across parent markets—25% within rotorcraft systems and nearly 8% in defense aviation equipment—underscores their critical role in safety, maneuverability, and mission readiness. In civil aviation, where helicopters are increasingly deployed for emergency services, tourism, and offshore transport, blades represent 4% of market value within broader aircraft components.

The transition toward composites, active blade control systems, and modular designs is redefining rotor performance. Government R&D funding and the gradual shift toward hybrid and electric helicopters are also influencing how next-generation blades are designed, manufactured, and deployed.

Key Growth Drivers

The helicopter blades market is driven by three powerful forces: defense modernization, fleet expansion, and technological innovation. Military spending across the USA, China, India, and NATO allies continues to prioritize rotorcraft, fueling demand for main and tail rotor blades designed for stealth, durability, and agility. Civil applications are equally important, as urban mobility, medical air services, and firefighting increasingly rely on helicopters to deliver speed and access where fixed-wing aircraft cannot.

Innovation in carbon fiber composites and titanium edges is improving fatigue resistance, noise suppression, and operational efficiency. This has strengthened confidence in aftermarket services, as operators seek longer life cycles and reduced downtime for their fleets.

Market Segmentation Insights

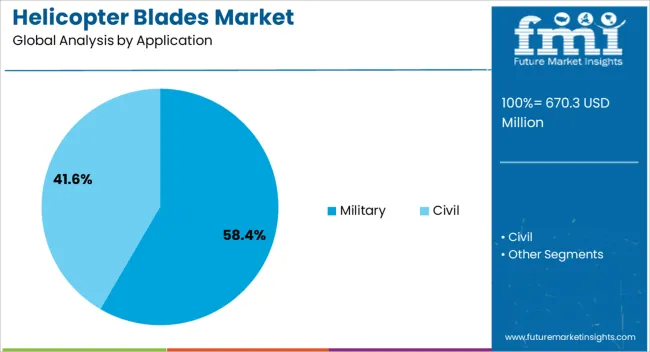

Military Dominance

The military segment is expected to account for 58.4% of total market share in 2025. This leadership is reinforced by global fleet modernization, stealth technologies, and the need for high-performance blades in tactical and logistic missions. Countries like the USA and India are investing heavily in blade upgrades for combat and utility helicopters, while NATO forces are upgrading fleets to meet new mission profiles.

Main Rotor Leadership

Main rotor blades, which are central to lift and maneuverability, will hold 67.9% of the market in 2025. Frequent wear and tear, high replacement rates, and continuous innovation in shape optimization and composite structures make this category the largest contributor to revenue growth.

OEM Distribution

Original Equipment Manufacturers (OEMs) will dominate distribution channels with a 61.2% share in 2025. Their advantage lies in early-stage design integration, long-term service contracts, and guaranteed quality assurance. Aftermarket players remain vital, but OEMs are setting the pace through proprietary technologies and defense partnerships.

Regional Growth Analysis

China leads the global growth outlook with a projected CAGR of 4.1% from 2025 to 2035, reflecting strong defense budgets and expanding civil helicopter use in surveillance, medical, and transport services. India follows with 3.8%, boosted by the “Make in India” initiative, which is driving domestic blade manufacturing and technology partnerships with international firms.

Europe maintains steady momentum, with France growing at 3.2% and Germany at 3.5%, supported by Airbus Helicopters’ R&D investments and strong export demand. The United Kingdom is expected to see a 2.9% CAGR, focused on defense programs and offshore applications. Meanwhile, the USA, despite being the world’s largest rotorcraft hub, will grow more slowly at 2.6%, largely due to its mature market status.

Opportunities for New Entrants

The helicopter blades market presents clear opportunities for both established aerospace giants and new manufacturers looking to expand. Start-ups specializing in composites, noise-reduction technologies, and modular blade designs have the chance to collaborate with OEMs or provide aftermarket upgrades. With the rise of eVTOL and hybrid rotorcraft, new players developing lightweight, efficient blades can position themselves as disruptors in a traditionally consolidated market.

For stakeholders such as fleet operators, defense contractors, and investors, the consistent CAGR and long replacement cycles highlight a dependable sector with gradual but reliable returns. Manufacturers focusing on eco-friendly materials, localized production, and long-term service packages will be best positioned to capture emerging demand.

Competitive Landscape

The competitive arena is led by aerospace leaders such as Airbus S.A.S., Bell Helicopter Textron, Boeing, and Lockheed Martin, all of whom integrate rotor systems into their broader helicopter platforms. Van Horn Aviation, LLC differentiates itself by specializing in aftermarket upgrades, FAA-certified composite replacements, and high-performance retrofit kits. Hindustan Aeronautics Limited (HAL) plays a key role in India’s defense procurement, supported by national programs for indigenous production.

Strategies among these players emphasize material innovation, lifecycle management, and international partnerships. Airbus and Boeing push composite designs with extended service life, while Bell focuses on aftermarket kits and modular retrofits. Lockheed Martin leverages defense contracts to expand rotor solutions, and HAL secures domestic demand through government procurement.

Marketing strategies across these firms highlight cross-sections of carbon fiber assemblies, aerodynamic shaping, and noise-reduction features, all designed to reassure operators about mission readiness, cost efficiency, and safety.

Purchase this Report for USD 5,000 Only | Get an Exclusive Discount Instantly! https://www.futuremarketinsights.com/checkout/24700

Everything You Need—within Your Budget. Request a Special Price Now! https://www.futuremarketinsights.com/reports/sample/rep-gb-24700

About Future Market Insights (FMI)

Future Market Insights, Inc. (ESOMAR certified, recipient of the Stevie Award, and a member of the Greater New York Chamber of Commerce) offers profound insights into the driving factors that are boosting demand in the market. FMI stands as the leading global provider of market intelligence, advisory services, consulting, and events for the Packaging, Food and Beverage, Consumer Technology, Healthcare, Industrial, and Chemicals markets. With a vast team of over 400 analysts worldwide, FMI provides global, regional, and local expertise on diverse domains and industry trends across more than 110 countries.

Contact Us:

Future Market Insights Inc.

Christiana Corporate, 200 Continental Drive,

Suite 401, Newark, Delaware – 19713, USA

T: +1-347-918-3531

For Sales Enquiries: sales@futuremarketinsights.com

Website: https://www.futuremarketinsights.com

LinkedIn| Twitter| Blogs | YouTube