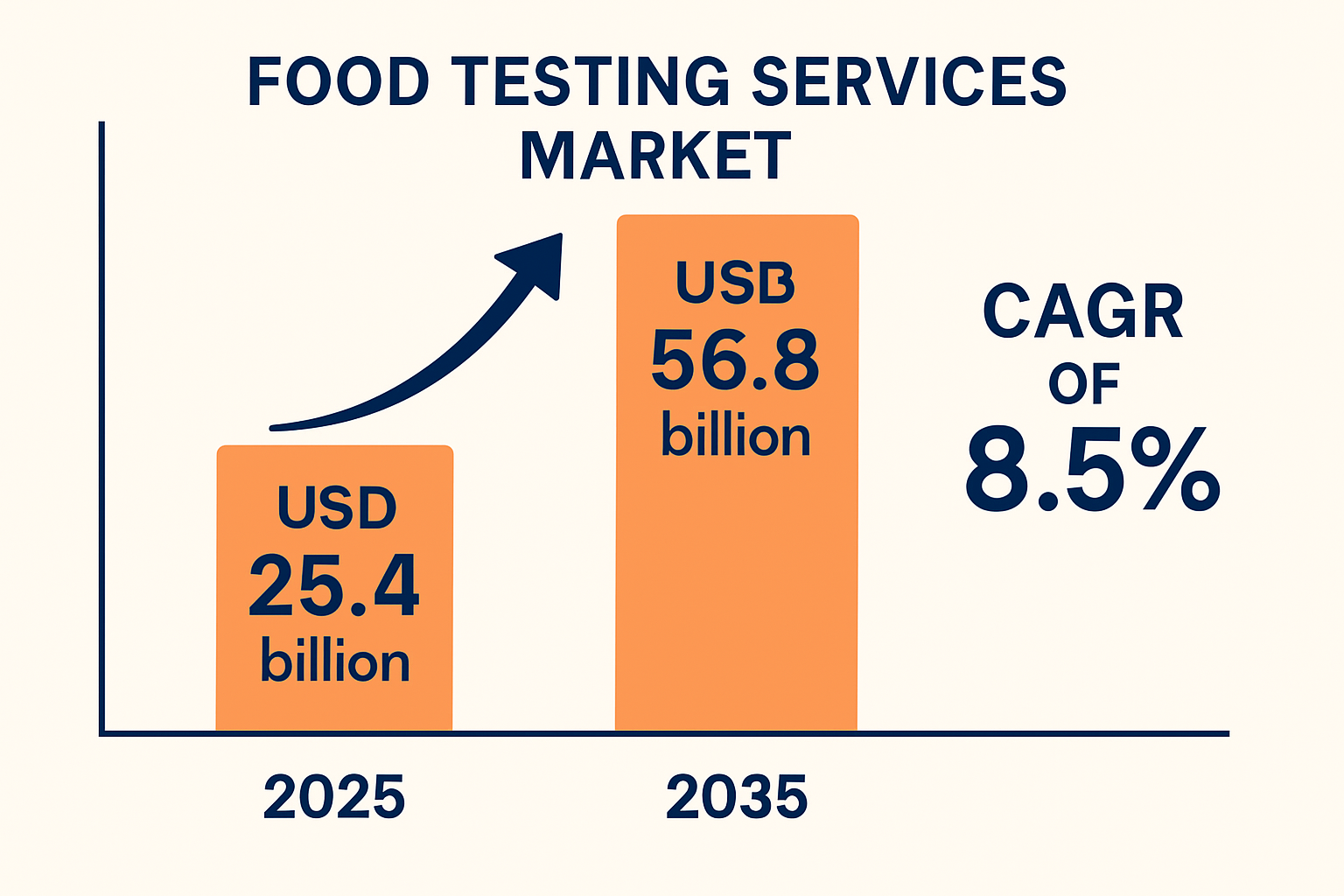

The food testing services market is forecast to surge from USD 25.4 billion in 2025 to USD 56.8 billion by 2035, delivering a robust 8.5 % CAGR. Escalating food‑borne illness outbreaks, complex cross‑border supply chains, and tougher enforcement by regulators such as the FDA, EFSA, and Codex Alimentarius are pushing manufacturers, processors, and importers to tighten quality‑control regimes. Microbiological testing leads today’s service mix, yet rapid gains in allergen, pesticide‑residue, and authenticity testing signal a broadening safety mandate across every food category.

Uncover Essential Data – Get A Sample Copy: https://www.futuremarketinsights.com/reports/sample/rep-gb-10486

Market Trends Highlighted

- Regulation‑Driven Testing Boom

• Mandatory HACCP plans, FSMA rules, and EU hygiene packages are elevating routine testing volumes. - Shift to Rapid & High‑Throughput Methods

• PCR, MALDI‑TOF, next‑gen sequencing, and biosensors cut turnaround times from days to hours, enabling real‑time release. - Clean‑Label & “Free‑From” Verification

• Growth in organic, non‑GMO, gluten‑free, and plant‑based foods fuels demand for residue, allergen, and authenticity assays. - E‑Commerce & Direct‑to‑Consumer Pressures

• Online grocery expands cold‑chain complexity and recall risk, prompting brands to outsource more frequent spot checks. - Data‑Integrated Quality Management

• Cloud LIMS, blockchain traceability, and AI‑driven risk modeling help labs deliver actionable insights, not just test results. - Outsourcing Surge Among SMEs

• Smaller processors lacking in‑house labs rely on third‑party providers for compliance, driving market consolidation.

Get Report Link: https://www.futuremarketinsights.com/reports/food-testing-market

Key Takeaways of the Report

- Market Size & Growth: from USD 25.4 billion in 2025 to USD 56.8 billion by 2035at 8.5 % CAGR, outpacing overall food‑processing capex.

- Service Mix (2025):

• Microbiological testing holds 34.6 % share, led by Salmonella, Listeria, E. coli screening.

• Chemical & residue testing is the fastest‑growing sub‑segment as pesticide, veterinary‑drug, and mycotoxin limits tighten. - Technology Adoption: next‑gen sequencing costs have fallen 50 % in five years, unlocking source‑tracking and outbreak forensics for mid‑tier brands.

- Demand Hotspots: organic, non‑GMO, allergen‑free, and “clean‑label” claims are now audited by retailers, stimulating third‑party verification.

- Regulatory Momentum: over countries updated food‑safety statutes since 2022, expanding mandatory test panels and driving global harmonization.

- Digital Transformation: leading labs have deployed cloud‑based LIMS; real‑time dashboards shorten recall decision cycles by up to 48 hours.

Regional Market Outlook

- North America: The United States posts a 6.2 % CAGR as FSMA full enforcement, rising recalls, and e‑commerce logistics propel microbiological and allergen testing across meat, dairy, and meal‑kit segments.

- Europe: The UK (5.8 % CAGR), France (6.0 %), Germany (5.7 %), and Italy (5.4 %) upgrade traceability and sustainability audits—especially for organic, plant‑based, and PDO/PGI products—spurring demand for authenticity, residue, and environmental monitoring services.

- Asia‑Pacific: China (7.0 % CAGR) and South Korea (7.1 %) spearhead growth; rising middle‑class incomes, export ambitions, and zero‑tolerance safety campaigns escalate outsourcing. Japan (5.5 %) focuses on allergen and radionuclide testing post‑Fukushima, while Australia/New Zealand prioritize clean‑label verification for premium exports.

- Key Takeaways Of The Report

-

The food testing services market is experiencing strong growth driven by rising food safety concerns and regulatory pressure.

-

Microbiological testing remains the dominant segment due to increasing pathogen-related contamination.

-

Demand is rising for allergen, pesticide, and GMO testing in response to clean-label, organic, and plant-based food trends.

-

The growth of e-commerce and processed food sectors is boosting the need for advanced, third-party testing services.

-

Countries across Asia-Pacific, North America, and Europe are prioritizing food safety compliance, sustainability, and traceability.

-

Technological advancements are enhancing testing accuracy and speed, making testing services more accessible and efficient.

-

Key Industry Players

- Eurofins Scientific

- SGS SA

- Intertek Group PLC

- Bureau Veritas

- ALS Limited

- MérieuxNutriSciences

- NSF International

- TÜV SÜD

- UL LLC

- AsureQuality

- Microbac Laboratories

- EMSL Analytical, Inc.

- Food Safety Net Services (FSNS)

- QIMA

- Symbio Laboratories

- Romer Labs

- Campden BRI

- Silliker

Explore Food Technology Industry Analysis : https://www.futuremarketinsights.com/industry-analysis/food-technology

Key Segmentation

By Testing Type:

In terms of testing type, the industry is divided into microbiological testing, chemical testing, allergen testing, and molecular testing.

By Technology:

With respect to technology, the market is classified into traditional methods and advanced methods.

By Food Products Tested:

Based on food products tested, the industry is divided into dairy products, meat and seafood, fruits and vegetables, cereals and grains, beverages, processed and packaged foods, infant and baby food, animal feed, and pet food.

By Region:

The industry is segmented into North America, Latin America, Europe, Asia Pacific, and the Middle East & Africa (MEA).