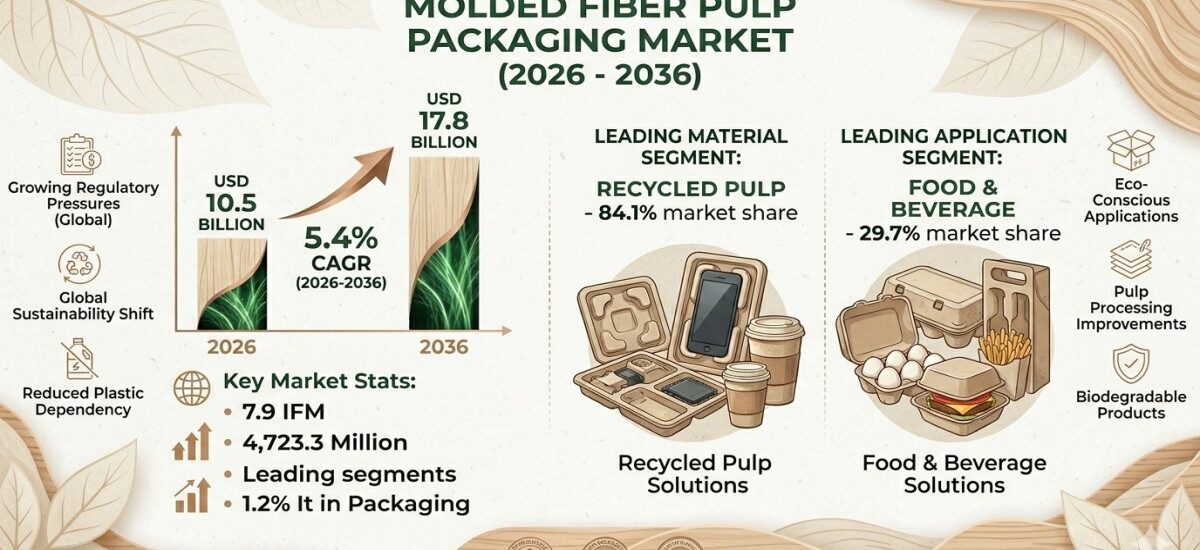

The global molded fiber pulp packaging market is entering a steady growth phase, driven by increasing demand for sustainable, biodegradable, and recyclable packaging solutions across food service, consumer goods, electronics, and industrial sectors. Valued at USD 10.5 billion in 2026, the market is projected to reach USD 17.8 billion by 2036, reflecting a CAGR of 5.4% over the forecast period.

Growth reflects a broader shift away from single-use plastics toward fiber-based alternatives that align with environmental regulations and circular economy goals. Molded fiber packaging, produced primarily from recycled pulp, is gaining traction due to its low environmental impact, cost efficiency, and compatibility with existing recycling systems.

Discover Growth Opportunities in the Market – Get Your Sample Report Now

https://www.futuremarketinsights.com/reports/sample/rep-gb-2900

Sustainability Regulations and Circular Economy Driving Adoption

Molded fiber pulp packaging adoption is strongly supported by global regulatory pressure to reduce plastic waste and improve recyclability. Governments and environmental bodies are promoting compostable and fiber-based materials, encouraging industries to transition toward eco-friendly packaging formats.

Key demand drivers include:

• Growing regulatory restrictions on single-use plastics across food service and retail sectors

• Increasing consumer preference for sustainable and recyclable packaging

• High availability and recyclability of paper and pulp-based raw materials

• Expansion of food delivery, takeaway, and protective packaging applications

Material Innovation Enhancing Performance and Application Scope

Historically, molded fiber packaging faced limitations in moisture resistance, barrier performance, and surface finish.

Recent advancements are addressing these challenges:

• Transfer molded fiber: Cost-efficient, scalable, and widely used in egg cartons and trays

• Thermoformed fiber: Improved surface finish, precision, and suitability for premium packaging

• Thick-wall pulp: Strong cushioning for industrial and protective applications

• Barrier coatings: Development of PFAS-free, grease-resistant, and moisture-control solutions

Transfer molded products dominate the market, accounting for 52.2% of demand, while thermoformed fiber is gaining traction in high-end consumer-facing applications.

Key Applications: Primary Packaging Leads Market Expansion

Primary packaging is the largest application segment, accounting for 70.1% of global demand. Molded fiber is increasingly used in direct consumer packaging, replacing plastic containers, trays, and clamshells.

Key application highlights include:

• Primary packaging: Food containers, clamshells, trays, and consumer packaging formats

• Secondary packaging: Protective inserts and transport cushioning solutions

• Edge protectors: Industrial and logistics applications requiring structural protection

Product Insights: Trays and Clamshells Dominate

Trays remain the leading product segment, capturing 34.3% of market share in 2026, due to their versatility across food, agriculture, and industrial applications.

Other key product segments include:

• Clamshell containers: Combining protection and presentation in food service

• End caps: Protective packaging for electronics and appliances

• Plates, bowls, and cups: Growing adoption in sustainable food service packaging

• Drink carriers: Widely used in takeaway and quick-service restaurants

Source Analysis: Recycled Pulp Defines Market Identity

Recycled pulp dominates the market, accounting for 91.7% of total demand, highlighting the industry’s strong alignment with circular economy principles.

• Recycled pulp: Cost-effective, sustainable, and widely available

• Virgin pulp: Used in applications requiring higher strength, cleanliness, or finish quality

While recycled pulp supports sustainability goals, it also introduces challenges related to fiber quality and contamination control.

End-Use Insights: Egg Packaging Remains Core Segment

Egg packaging is the largest end-use segment, holding 23.9% of market share, driven by the material’s natural suitability for cushioning, stacking, and ventilation.

Other major end-use industries include:

• Fruit packaging: Protection and ventilation for fresh produce

• Food service: Containers, trays, and takeaway packaging

• Consumer durables: Protective inserts for electronics and appliances

• Automotive and logistics: Industrial packaging and transport protection

• Healthcare and cosmetics: Emerging applications requiring sustainable packaging

Regional Insights: Asia-Pacific Leads Growth

Asia-Pacific (APEJ) remains the largest and fastest-growing region, supported by manufacturing expansion, rising consumption, and strong packaging demand.

• APEJ – CAGR 7.4%: Manufacturing scale, export demand, and cost-efficient production

• Latin America – CAGR 5.7%: Growth in food and agricultural packaging

• North America – CAGR 4.4%: Regulation-driven substitution and mature demand

• Western Europe – CAGR 3.8%: Sustainability regulations and recycling targets

• Japan – CAGR 3.6%: High-quality, precision-focused packaging demand

Competitive Landscape: Performance and Sustainability Define Leaders

The molded fiber pulp packaging market is moderately fragmented, with companies competing on material innovation, production scale, and barrier technology.

Key players include:

• Huhtamaki

• Brødrene Hartmann A/S

• Genpak

• CKF Inc.

• Sabert

• UFP Technologies

• Pactiv Evergreen

• Henry Molded Products

• Keiding, Inc.

These companies focus on:

• Scalable production of trays, cartons, and protective packaging

• Development of PFAS-free and compostable barrier solutions

• High-quality thermoformed fiber for premium applications

• Regional manufacturing expansion and supply chain optimization

Analyst Perspective: From Plastic Substitute to Performance Material

Industry analysts highlight that molded fiber packaging is evolving beyond a simple plastic alternative into a performance-driven material category.

“Adoption depends not only on sustainability benefits but also on consistency, barrier performance, and product presentation. The winners will be those who combine material innovation with manufacturing precision,” said a senior market analyst.

Future Outlook: Performance Innovation and Sustainable Growth

Over the next decade, growth opportunities will focus on:

• Development of advanced barrier coatings without PFAS

• Expansion of thermoformed fiber in premium packaging

• Integration of circular economy and recycling systems

• Increased adoption in electronics, healthcare, and cosmetics packaging

Despite challenges in moisture resistance and finish consistency, continuous innovation is expected to expand the application scope of molded fiber packaging globally.

Key Market Stats

• Market Size (2026): USD 10.5 Billion

• Forecast Value (2036): USD 17.8 Billion

• CAGR (2026–2036): 5.4%

• Leading Product Segment: Trays – 34.3% market share

• Leading Process Type: Transfer Molded – 52.2% market share

• Leading Source: Recycled Pulp – 91.7% share

• Leading Application: Primary Packaging – 70.1% share

Key Growth Regions

Asia-Pacific (APEJ), North America, Western Europe, Latin America, Japan

Top Players

Huhtamaki, Brødrene Hartmann A/S, Genpak, CKF Inc., Sabert, UFP Technologies, Pactiv Evergreen

Why FMI: https://www.futuremarketinsights.com/why-fmi

About Future Market Insights (FMI)

Future Market Insights, Inc. (FMI) is an ESOMAR-certified, ISO 9001:2015 market research and consulting organization, trusted by Fortune 500 clients and global enterprises. With operations in the U.S., UK, India, and Dubai, FMI provides data-backed insights and strategic intelligence across 30+ industries and 1200 markets worldwide.

Contact Us:

Future Market Insights Inc., Christiana Corporate, 200 Continental Drive, Suite 401, Newark, Delaware – 19713, USA

T: +1-347-918-3531

For Sales Enquiries: sales@futuremarketinsights.com

Website: https://www.futuremarketinsights.com

LinkedIn| Twitter| Blogs | YouTube