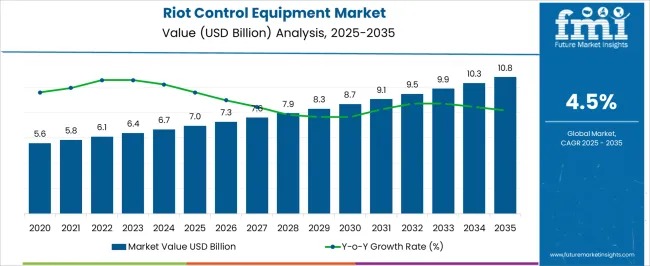

The global riot control equipment market is set for sustained expansion over the next decade, projected to grow from USD 7.0 billion in 2025 to USD 10.8 billion by 2035, registering a compound annual growth rate (CAGR) of 4.5%. This steady trajectory reflects the rising prioritization of public safety, law enforcement preparedness, and non-lethal crowd management solutions across both developed and emerging economies.

During the early adoption phase between 2020 and 2024, the market expanded gradually from USD 5.6 billion to USD 7.0 billion, as law enforcement agencies and security forces evaluated equipment performance, safety standards, and operational handling through pilot deployments. These initial programs laid the foundation for broader procurement by validating effectiveness in real-world scenarios and aligning equipment usage with regulatory and policy frameworks. By 2025, the market enters a more structured growth phase, supported by approved budgets, standardized procurement processes, and long-term modernization strategies.

Market Evolution Reflects Scaling and Consolidation Dynamics

From 2025 to 2030, the riot control equipment market is expected to move into a scaling phase, surpassing USD 8.3 billion by 2030. Growth during this period is driven by expanded deployments across urban centers and high-risk regions, rising investments in training and simulation, and increasing emphasis on maintenance and lifecycle management. Law enforcement agencies are strengthening readiness by equipping personnel with standardized protective gear and non-lethal systems designed to manage large-scale public gatherings while minimizing injury risks.

Between 2030 and 2035, the market transitions into a consolidation phase, with growth moderating toward USD 10.8 billion. During this period, established suppliers reinforce their market positions through long-term contracts, while smaller players consolidate or exit. The consistent 4.5% CAGR highlights the market’s evolution into a mature yet resilient segment, increasingly viewed as a standard component of public order management and tactical preparedness.

Get access to comprehensive data tables and detailed market insights — request your sample report today!

Law Enforcement and Public Order Management Anchor Demand

Law enforcement agencies represent the largest end-user segment, accounting for 46.8% of market revenue in 2025. This dominance reflects ongoing professionalization of police forces, expansion of urban policing strategies, and growing reliance on non-lethal solutions to balance public safety with controlled use of force. Investments in training programs, standardized protocols, and technology-enabled monitoring systems continue to reinforce adoption across municipal, regional, and national agencies.

From an application standpoint, public order management leads with a 57.2% share, driven by the need to manage protests, demonstrations, sporting events, and festivals effectively. Governments and public authorities are increasingly focused on preventive crowd control measures that reduce escalation risks, protect personnel, and safeguard public infrastructure. Integration of monitoring tools with protective gear and less-lethal systems has improved situational awareness and response coordination, strengthening this segment’s leadership.

Personal Protective Equipment Remains the Cornerstone

By product type, personal protective equipment (PPE) holds the leading position with a 39.4% market share in 2025. Helmets, shields, body armor, and protective clothing remain essential for safeguarding officers during high-risk operations. Rising concerns over officer safety, coupled with regulatory mandates on protective standards, continue to drive investment in this segment.

Advances in lightweight materials, ergonomic design, and modular configurations have enhanced mobility and comfort without compromising protection. The ability to tailor PPE to specific threat levels and operational environments further supports widespread adoption, ensuring that this segment remains central to market growth over the forecast period.

Regional Momentum Driven by Urbanization and Policy Focus

Regionally, North America, Europe, and Asia-Pacific emerge as key growth centers. North America and Europe lead in adoption of advanced non-lethal systems and high-performance protective gear, emphasizing precision, compliance, and operational efficiency. Asia-Pacific is witnessing rising demand for scalable and cost-effective riot control solutions, driven by rapid urbanization, population density, and expanding public safety initiatives.

Country-level growth highlights China (6.1% CAGR) and India (5.6%) as high-momentum markets, supported by urban security needs, government-backed procurement, and training initiatives. Germany (5.2%) demonstrates strong demand for ergonomically designed, regulation-compliant equipment, while the UK (4.3%) and USA (3.8%) reflect steady growth tied to modernization programs and public safety budgets.

Non-Lethal Systems and Training Shape Market Differentiation

Non-lethal weapon systems—including tear gas launchers, water cannons, rubber bullets, and electroshock devices—play a critical role in market expansion. Developed markets prioritize precision-engineered, multi-use systems designed to minimize collateral damage, while emerging regions favor robust and affordable solutions aligned with local operational needs.

Equally important is the role of training and operational readiness. Simulation-based training and scenario-driven exercises in North America and Europe enhance response effectiveness and reduce injury risks, while foundational training programs in Asia-Pacific balance readiness with cost efficiency. Suppliers offering integrated training, operational support, and compliance guidance gain a competitive edge in long-term procurement decisions.

Competitive Landscape Focused on Safety, Technology, and Compliance

The riot control equipment market is moderately consolidated, with leading players competing on durability, ergonomics, technological integration, and regulatory compliance. Key companies such as Axon Enterprise Inc., Blackhawk, Byrna Technologies Inc., Combined Systems, Inc., Condor Non-lethal Technologies, Etienne Lacroix Group, Genasys, Inc., Rheinmetall AG, and Safariland, LLC continue to invest in research and development to enhance protective materials, non-lethal effectiveness, and situational awareness tools.

Innovation is increasingly centered on integrating smart technologies, wearable sensors, and advanced monitoring systems to support data-driven decision-making during complex operations. These advancements are reshaping riot control equipment from basic protective tools into integrated public safety solutions.

Outlook: Steady Growth Anchored in Public Safety Priorities

As urban populations grow and public gatherings become more frequent, the need for effective, non-lethal crowd management solutions is expected to remain strong. While challenges such as regulatory complexity and budget constraints persist, the long-term fundamentals of the riot control equipment market are underpinned by sustained public safety investments and modernization efforts.

With a clear shift toward standardized, technology-enabled, and safety-focused solutions, the riot control equipment market is positioned for consistent growth through 2035—offering a compelling outlook for stakeholders seeking insight into evolving public security and law enforcement infrastructure trends.

About Future Market Insights (FMI)

Future Market Insights, Inc. (FMI) is an ESOMAR-certified, ISO 9001:2015 market research and consulting organization, trusted by Fortune 500 clients and global enterprises. With operations in the U.S., UK, India, and Dubai, FMI provides data-backed insights and strategic intelligence across 30+ industries and 1200 markets worldwide.