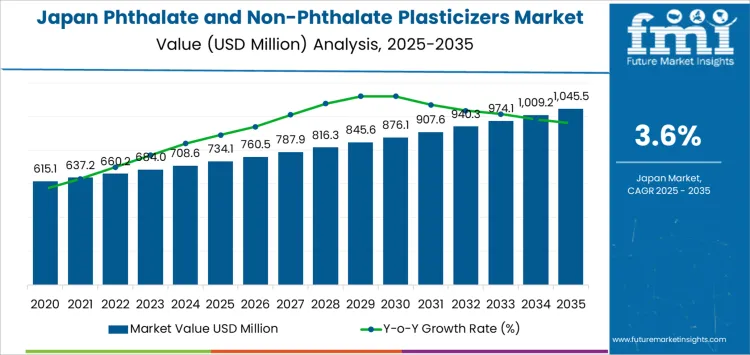

The Japan phthalate and non-phthalate plasticizers market is poised for significant expansion, with total industry value projected to grow from USD 734.1 million in 2025 to USD 1,045.5 million by 2035, reflecting sustained demand and innovation across sectors. This growth trend highlights not only the established strength of legacy chemical manufacturers but also the rising influence of new technology developers who are shaping the future of plasticizer solutions for a wide range of industrial and consumer applications.

Plasticizers play an essential role in enhancing the flexibility, durability, and performance of polymers used in automotive parts, medical devices, consumer goods, construction materials, and electronics. Historically dominated by phthalate-based plasticizers due to their cost-effectiveness and proven utility, the market landscape in Japan is changing rapidly as environmental regulations tighten and industry stakeholders increasingly adopt safer, non-phthalate alternatives.

Market Dynamics Driving Expansion

A combination of factors is fueling this growth, including strong construction and automotive industries, heightened regulatory scrutiny of phthalate substances, and a marked shift toward sustainability. Japanese manufacturers and global chemical companies are investing in next-generation plasticizer technologies that balance performance with environmental and health considerations. These advancements are helping meet evolving customer expectations while addressing stringent safety standards mandated by Japanese regulatory bodies.

The demand for non-phthalate plasticizers is especially strong in sectors where product safety is paramount, such as food packaging, medical devices, and children’s products. Non-phthalate and bio-based plasticizers are gaining traction as viable substitutes that align with global trends toward green chemistry and reduced chemical hazards.

Established Industry Leaders Innovating for the Future

Several established chemical firms continue to play a pivotal role in Japan’s plasticizers market. Industry leaders such as BASF SE, Exxon Mobil Corporation, Evonik Industries AG, Eastman Chemical Company, and Lanxess AG remain at the forefront through expansive product portfolios and ongoing research into both phthalate and non-phthalate formulations.

These established players are leveraging decades of technical expertise to optimize performance characteristics while reducing environmental impact. Their strategies include reformulating traditional plasticizers to improve compliance with strict health regulations, scaling production of non-phthalate products, and enhancing customer support services to help manufacturers transition to greener alternatives.

To access the complete data tables and in-depth insights, request a sample report here

Emerging Manufacturers and New Technologies Making an Impact

Alongside these traditional heavyweights, a new wave of manufacturers and innovators is reshaping the competitive landscape. Smaller niche firms, agile startups, and R&D-driven organizations are introducing advanced plasticizer technologies that focus on bio-based feedstocks, hybrid formulation approaches, and enhanced material compatibility.

These emerging players are not only expanding their domestic footprint but are also positioning themselves for global reach by tapping into export markets and forming strategic partnerships. Their innovations are helping accelerate the adoption of next-generation plasticizers suited for high-value applications such as flexible electronics, bio-medical devices, and eco-friendly packaging.

Technological advancements in bio-based plasticizers, including citrate esters, epoxidized oils, and other renewable materials, are gaining momentum as companies respond to both regulatory pressures and growing customer demand for safer alternatives. Investment in sustainable technology is seen as a key differentiator driving competitiveness among both established and new entrants.

Regional and Sectoral Highlights

The market’s growth is not uniform across Japan; regions with strong industrial bases such as Kyushu & Okinawa, Kanto, and Kansai are emerging as key hubs for plasticizer demand. These areas benefit from proximity to major automotive, electronics, and construction sectors, where plastics with specific performance characteristics are critical.

Wire and cable manufacturing, in particular, continues to lead application demand due to the high flexibility requirements of electrical infrastructure and telecommunications systems. Other important application segments include flooring and wall coverings, films and sheets, coatings, and consumer goods.

Opportunities for Expansion and Collaboration

As the Japan plasticizers market evolves, there are significant opportunities for manufacturers to expand business operations through innovation, strategic partnerships, and by targeting new end-use industries. Collaboration between established companies and emerging tech innovators can accelerate product development cycles, enhance supply chain resilience, and unlock new revenue streams.

Manufacturers investing in sustainable formulations are expected to benefit from growing preferences for safer materials, especially in markets where environmental concern and regulatory compliance are critical. Continued focus on R&D, combined with a flexible approach to technological integration, will enable both legacy and new manufacturers to thrive in this dynamic environment.