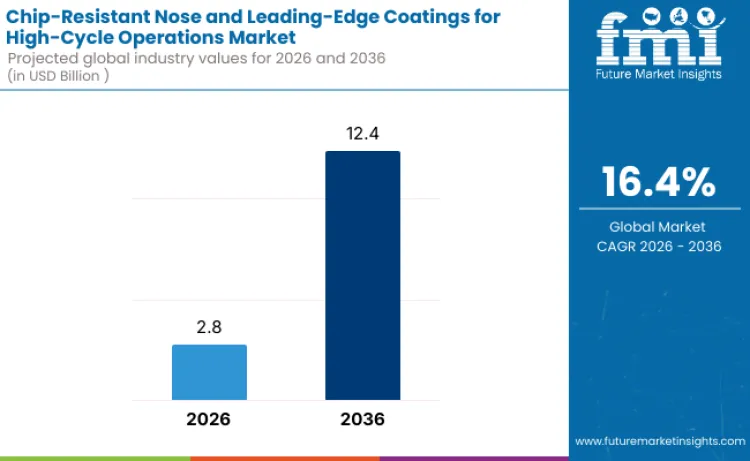

The global chip-resistant nose and leading-edge coatings for high-cycle operations market is on track for remarkable expansion, with estimated industry value poised to more than quadruple by 2036. Valued at USD 2.8 billion in 2026, this specialized segment of aerospace surface protection is forecast to grow to approximately USD 12.4 billion by 2036, driven by surging aircraft utilization, increasing flight cycles, and rising demand for durable exterior surface coatings. The projected compound annual growth rate of 16.4 % over the 2026-2036 period underscores the heightened emphasis on protective coatings that counter wear, environmental erosion, and foreign object damage in high-performance aircraft operations.

Modern aviation fleets — encompassing commercial airlines, defense transport, and unmanned aerial systems — are experiencing unprecedented operational demands. More frequent takeoffs and landings elevate exposure to particulates, dust, rain erosion, and runway debris, accelerating degradation on critical aerodynamic surfaces such as nose cones and leading edges of wings and engines. As a result, industry players and airline operators are embracing advanced chip-resistant coatings not just as maintenance necessities but as core enablers of lifecycle cost reduction, improved operational uptime, and surface integrity in high-cycle environments.

Technology and Innovation Driving the Market

At the heart of this market’s evolution are innovations in coating materials and application technologies. High-durability polyurethane impact-resistant coatings currently lead market adoption due to their balance of abrasion resistance and flexibility under dynamic flight stresses. These coatings are engineered to absorb particulate impact without compromising adhesion or aerodynamic profiles, making them ideal for both metallic and composite surfaces.

Beyond traditional polyurethane systems, next-generation formulations incorporate nano-additives, elastomeric modifiers, and advanced adhesion promoters to further extend wear life and erosion resistance. Hybrid ceramic and nano-composite coatings are gaining traction for their ability to combine high hardness with reduced weight — an important factor as airlines and OEMs strive to improve fuel efficiency while maintaining superior protective performance.

Automated application processes and rapid cure technologies are also transforming how these advanced coatings are applied within MRO (Maintenance, Repair and Overhaul) and OEM (Original Equipment Manufacturer) environments, facilitating better consistency and faster turnarounds for high-throughput operations.

To access the complete data tables and in-depth insights, request a sample report here

Regional Growth Hotspots and Market Dynamics

Market growth is being fueled across major aviation regions, notably in Asia Pacific and North America, where expanding aircraft fleets and modernization programs are creating robust demand for enhanced exterior surface protection. Key growth markets such as China and India are witnessing particularly strong adoption rates as both domestic and international flight operations intensify. Operators in the United States and Japan are driven by advanced coating R&D and a focus on cutting-edge materials science.

This global demand reflects a broader shift toward coatings that not only extend service intervals and reduce maintenance disruptions but also contribute to long-term economic and environmental efficiencies across fleets operating in diverse climatic conditions.

Competitive Landscape: Established Leaders and Emerging Innovators

The competitive arena is shaped by both long-standing coating manufacturers and emerging technology developers seeking to expand their footprint in the high-cycle aerospace coatings segment.

Leading established players include aerospace surface protection specialists whose portfolios now feature a range of high-performance coating solutions designed for rigorous operational environments. These vendors continue to invest in material science advancements that improve impact resistance, adhesion stability, and environmental durability.

Alongside these industry incumbents, several newer and aggressive technology entrants are introducing disruptive coating systems that leverage hybrid material structures and novel additives. These innovators are positioning themselves to capture niche segments of the market, particularly where extreme erosion resistance or specialized performance attributes are required for next-generation aircraft surfaces.

Both established manufacturers and new market challengers are forging strategic collaborations with airlines, MRO service providers, and aircraft OEMs to co-develop application techniques, certify novel materials for high-cycle usage, and accelerate commercialization. These alliances reflect a broader industry commitment to more resilient aircraft coatings capable of meeting tomorrow’s operational demands.

Outlook and Strategic Imperatives

As flight frequencies continue to increase and airline operators prioritize lifecycle cost efficiencies, the chip-resistant nose and leading-edge coatings market stands at a pivotal inflection point. Adoption of advanced surface protection systems is no longer confined to legacy corrosion-mitigation strategies but is emerging as a strategic capability that enhances aircraft availability, lowers unscheduled maintenance, and supports aggressive utilization targets.