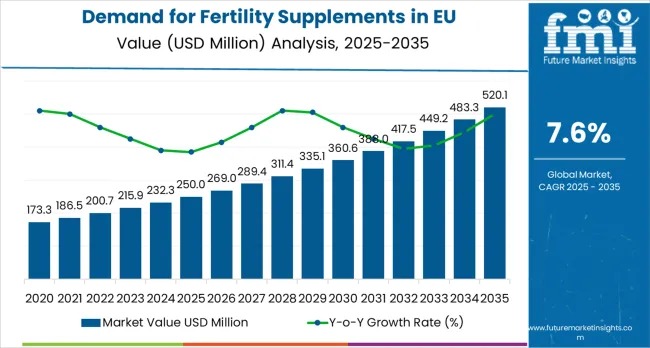

The demand for fertility supplements across the European Union is entering a sustained growth phase, reflecting a broader shift toward proactive reproductive health management. According to the latest food and health industry intelligence, the EU fertility supplements market is projected to expand from USD 250.0 million in 2025 to USD 520.1 million by 2035, registering a robust CAGR of 7.6% over the forecast period. This expansion is primarily supported by rising awareness of fertility nutrition, increasing adoption among couples, and improving access through pharmacies, specialty health stores, and rapidly growing online channels.

Market growth is expected to be largely volume-driven, particularly in the first half of the forecast period. Increasing unit consumption reflects growing acceptance of fertility supplements as part of preventive healthcare rather than niche wellness products. While price growth will play a secondary role, the gradual introduction of premium, plant-based, organic, and clinically enhanced formulations is expected to lift average selling prices, especially between 2030 and 2035.

Explore trends before investing – request a sample report today! https://www.futuremarketinsights.com/reports/sample/rep-gb-27169

Volume Expansion Anchors Market Momentum

As per FMI’s global health and ingredients research, volume growth will remain the dominant contributor to market expansion, supported by several structural factors. These include delayed parenthood trends across Europe, rising diagnosis rates of fertility-related challenges, and increasing endorsement of nutritional interventions by healthcare professionals. Women’s fertility supplements currently account for nearly 65% of total demand, while men’s formulations represent around 35%, reflecting growing awareness of male reproductive health.

Price-led growth, while smaller in comparison, is becoming increasingly relevant. Premiumization is being driven by innovations such as advanced delivery systems, enhanced bioavailability technologies, and clean-label ingredient sourcing. Together, these factors are enabling manufacturers to capture incremental value without slowing adoption.

Market Snapshot Highlights

- Market Value (2025): USD 250.0 million

- Forecast Value (2035): USD 520.1 million

- Forecast CAGR: 7.6%

- Leading Product Type: Vitamins & Minerals (50.0% share)

- Top Form Segment: Tablets (33.8%)

- Key Growth Regions: Western and Central Europe

Shifting Consumer and Clinical Priorities

Demand growth in the EU is closely tied to evolving consumer perceptions of reproductive health. Fertility supplements are increasingly viewed as evidence-based, essential healthcare solutions rather than optional wellness products. European consumers and reproductive health professionals place high emphasis on ingredient authenticity, clinical validation, regulatory compliance, and bioavailability, driving demand for specialty formulations with documented efficacy.

Regulatory oversight is also shaping the market. EU authorities continue to refine guidelines around fertility health claims, safety standards, and clinical substantiation, favoring manufacturers with strong research capabilities and compliant production processes. Clinical studies across European research institutions have reinforced the role of targeted nutrition in areas such as ovulation support, sperm quality enhancement, hormonal balance, and overall reproductive wellness.

Segmental Insights

By product type, vitamins and minerals dominate with a 50.0% share, supported by their central role in evidence-based fertility nutrition. These formulations offer consistent dosing, strong clinical acceptance, and seamless integration with fertility treatment protocols across EU healthcare systems.

By form, tablets account for 33.8% of total demand, reflecting high patient compliance, cost efficiency, and compatibility with advanced release technologies. Capsules and tablets together make up nearly 70% of consumption, while powders and liquids address niche personalization needs.

Distribution remains concentrated across online platforms and pharmacies, contributing roughly 60% of total sales, underscoring the importance of digital health engagement and trusted clinical channels.

Regional Performance Across the EU

Germany leads the EU fertility supplements market with a 28.5% share in 2025, supported by its advanced reproductive healthcare infrastructure and strong emphasis on evidence-based medicine. France follows with 19.2%, driven by premium clinical positioning, while Italy accounts for 15.1%, benefiting from integration into traditional healthcare practices.

Spain is among the fastest-growing markets, registering a CAGR of 7.9%, fueled by expanding fertility clinics and rising urban health awareness. The Netherlands grows at 7.4%, leveraging its strong research ecosystem and clinical leadership. Emerging markets across the Rest of Europe are expected to post the highest growth at 8.1% CAGR, reflecting improving access and awareness.

Competitive Landscape and Strategic Focus

The EU fertility supplements market is highly competitive, featuring multinational nutraceutical brands, regional European manufacturers, and specialized reproductive health companies. Key players such as Garden of Life, Thorne Research, Fertility Nutraceuticals, and Nature’s Way are investing heavily in clinical research, European manufacturing capacity, and healthcare professional partnerships.

Strategic priorities include portfolio expansion, premium product launches, regulatory certifications, and direct-to-consumer engagement. Sustainability and clean-label sourcing are also emerging as critical differentiators, particularly in Germany, France, the Netherlands, and Nordic countries.

Outlook

With fertility health moving firmly into the mainstream of preventive care, the EU fertility supplements market is set for sustained, high-quality growth. Volume-led expansion, supported by clinical validation, personalization, and premium innovation, will continue to define competitive success through 2035.