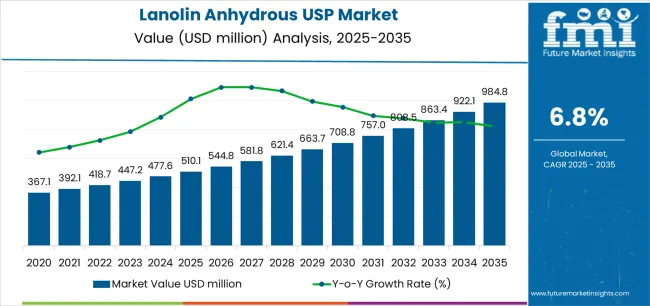

The global Lanolin Anhydrous USP market is estimated to be valued at approximately USD 510.1 million in 2025 and is on a robust growth trajectory toward nearly USD 1 billion by 2035, supported by strong demand across industrial, personal care, cosmetics, and pharmaceutical applications. This projected growth underscores the increasing adoption of high-purity lanolin anhydrous in a variety of sectors and highlights the market’s appetite for sustainable, natural ingredient solutions that resonate with evolving consumer and regulatory expectations.

Industry leaders and new entrants alike are positioning themselves for expansive growth by leveraging technological breakthroughs, enhancing product portfolios, and targeting emerging regional markets. With lanolin anhydrous USP becoming a cornerstone ingredient in clean beauty, advanced pharmaceuticals, and industrial formulations, the competitive landscape is undergoing rapid transformation driven by innovation, strategic collaborations, and capacity expansions.

Market Dynamics and Technology Trends

The lanolin anhydrous USP market’s growth trajectory is powered by multiple converging trends. Natural and clean-label ingredient preferences continue to gain traction among consumers, pushing manufacturers to refine formulation processes that deliver superior emollient properties while maintaining strict purity standards. At the heart of these developments is a technological shift toward advanced purification systems that deliver enhanced water-removal efficiency, greater stability, and traceable quality control. This heightened focus on purification and process optimization has enabled manufacturers to achieve ultra-pure grades sought after in pharmaceutical and luxury cosmetic applications.

New technological initiatives also include digitalized quality monitoring, batch tracking integrations, and supply chain transparency platforms that help producers better manage compliance across global markets. These innovations not only strengthen product reliability but also help brands demonstrate regulatory documentation and certification readiness — a critical requirement in highly regulated segments such as medical devices and therapeutic ointments.

To access the complete data tables and in-depth insights, request a sample report here

Established Players Driving Market Stability

Long-standing leaders in the lanolin anhydrous USP industry have been instrumental in shaping market direction through consistent quality, broad product portfolios, and expansive geographic reach. These seasoned manufacturers have deep roots in traditional emulsifier and natural ingredient supply chains, supplying to multinational cosmetic houses, pharmaceutical companies, and industrial formulators seeking reliable raw materials.

Such established players are now doubling down on strategic investments to enhance production capacities, strengthen sustainability credentials, and integrate cutting-edge purification technologies. Their goals include catering to stricter regulatory frameworks, accelerating product innovation timelines, and capturing greater market share in evolving application areas.

Emerging Manufacturers and Growth Opportunities

In parallel, newer entrants and regional specialists are making notable inroads by capitalizing on niche demand segments and regional supply advantages. These emerging manufacturers are carving out unique market positions by focusing on high-growth regional hubs such as Asia Pacific and South Asia, where personal care manufacturing and cosmetics production are expanding rapidly.

By partnering with local wool producers and technical research organizations, these companies are developing tailored lanolin anhydrous grades that meet specific performance and compliance criteria sought by rapidly evolving domestic brands. Additionally, emerging players are actively engaging in partnerships and co-development initiatives with established global suppliers to enhance technical expertise and widen distribution reach.

Strategic Expansion and Collaboration

Across the industry, collaborative ventures are becoming a defining trend. Established companies are entering into joint development agreements with technology innovators to co-create next-generation lanolin derivatives and specialty formulations. These partnerships often focus on enhancing hypoallergenic properties, introducing functional modifications for industrial use, and integrating traceability technologies that align with sustainability goals.

Emerging players are also forming alliances with regional distributors and formulation experts to accelerate market penetration. By offering localized technical support and custom formulation services, these companies are strengthening their competitive positions and fostering closer engagement with customers seeking tailored ingredient solutions.

Future Outlook and Market Opportunities

Looking forward, industry observers project that expanding demand for natural ingredient solutions in clean beauty, pharmaceuticals, and sustainable industrial applications will continue to fuel market expansion. Regions with burgeoning personal care manufacturing ecosystems are expected to contribute significantly to future demand, while established markets will drive innovation fronts through quality enhancements and regulatory leadership.

Both well-established manufacturers and agile new entrants are preparing to harness these trends by broadening product offerings, strengthening R&D capabilities, and implementing advanced manufacturing technologies that meet evolving customer expectations. The race to innovate and lead in the lanolin anhydrous USP market reflects not only a quest for greater market share but also a collective commitment to delivering high-quality, sustainable solutions that address diverse formulation needs across multiple industries.