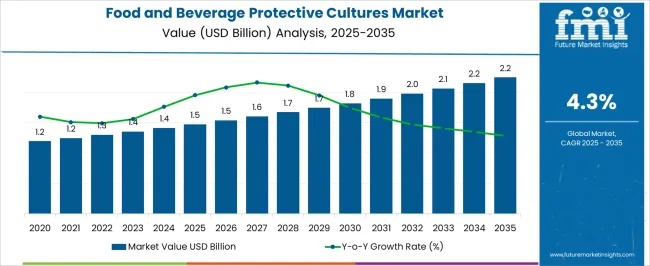

The global Food and Beverage Protective Cultures Market is entering a phase of sustained, innovation-led growth as manufacturers increasingly replace synthetic preservatives with natural, microbial solutions. Valued at USD 1.5 billion in 2025, the market is projected to reach USD 2.2 billion by 2035, expanding at a CAGR of 4.3% over the forecast period. This trajectory reflects a fundamental shift in food preservation strategies, driven by consumer trust, regulatory alignment, and supply-chain efficiency.

Protective cultures—naturally occurring microorganisms that inhibit spoilage and pathogenic bacteria—are now central to food safety strategies across dairy, meat, seafood, and fermented products. Their ability to extend shelf life while maintaining taste, texture, and nutritional integrity makes them a preferred solution for brands targeting health-conscious and clean-label consumers.

Get Exclusive Access To Data Tables, Market Sizing Dashboards, And Analyst Insights. Request Sample Report! https://www.futuremarketinsights.com/reports/sample/rep-gb-6074

Market at a Glance

- Industry value (2025): USD 1.5 billion

- Forecast value (2035): USD 2.2 billion

- Forecast CAGR (2025–2035): 4.3%

- Leading type segment (2025): Organic protective cultures (54.3% share)

- Top application (2025): Yogurt (27.4% share)

- Key growth regions: North America, Europe, Asia-Pacific

Clean-Label Demand Driving Adoption

The rapid expansion of the protective cultures market is closely linked to rising consumer awareness around ingredient transparency and food safety. Packaged and ready-to-eat foods remain under scrutiny, pushing manufacturers to eliminate artificial preservatives while still meeting shelf-life expectations. Protective cultures address this challenge by offering natural bio-protection without compromising product quality.

Industry players are also investing heavily in strain-specific R&D, enabling cultures to target precise spoilage organisms while preserving sensory attributes. Improvements in cold-chain infrastructure and the growing overlap between probiotics and protective cultures are further accelerating adoption, particularly in emerging markets.

Sustainability considerations add another layer of momentum. By reducing spoilage, recalls, and food waste, protective cultures support zero-waste strategies and improve overall supply-chain economics.

Organic Protective Cultures Lead by Type

By type, the market is segmented into organic and conventional food and beverage protective cultures. Organic protective cultures are projected to command 54.3% of total revenue in 2025, positioning them as the dominant sub-segment.

This leadership is fueled by:

- Strong global demand for certified organic and minimally processed foods

- Regulatory acceptance of organic microbial cultures

- Expanding retail shelf space for organic dairy and ready-to-eat products

Organic cultures naturally inhibit spoilage microorganisms without synthetic additives, making them highly attractive to brands targeting eco-conscious and health-aware demographics. Advances in microbial preservation and scalable production have also improved supply reliability under organic compliance frameworks.

Yogurt Remains the Anchor Application

From an application standpoint, yogurt represents the largest revenue contributor, accounting for 27.4% of the market in 2025. Yogurt’s sensitivity to microbial imbalance, post-acidification, and texture degradation makes protective cultures essential for maintaining consistency throughout storage and distribution.

Demand is rising across both traditional dairy and plant-based yogurt alternatives, where natural preservation is a key differentiator. Producers are increasingly using tailored protective cultures to stabilize probiotic, high-protein, and functional yogurt formulations, reinforcing the segment’s leadership.

Regional Outlook: North America and Europe at the Forefront

North America is expected to hold approximately 33% market share by 2025, supported by strong dairy and meat consumption, expansive retail networks, and rising beverage demand. Shelf-life optimization remains critical for inventory management across the region’s large-scale distribution systems.

Europe, accounting for 28.5% of the market, benefits from robust dairy production and a deeply ingrained preference for natural, organic, and sustainably labeled foods. Transparent ingredient labeling and stringent food safety standards continue to propel the adoption of protective cultures across the region.

Meanwhile, Asia-Pacific is emerging as a high-growth region, driven by urbanization, expanding cold-chain infrastructure, and increasing consumption of packaged and fermented foods.

Competitive Landscape and Recent Developments

The market features a mix of global leaders and specialized regional players, including DuPont, Chr. Hansen A/S, Kerry Inc., DSM N.V., Sacco S.r.l., Prayon S.A., BIOPROX Ingredients, Meat Cracks Technologie GmbH, PK Chem Industries Ltd., and OCP Group. Competition is shaped by innovation, strategic partnerships, and application-specific product launches.

Recent developments highlight this momentum:

- October 2024: Döhler and Sacco System formed an alliance to co-develop cultures for plant-based dairy alternatives.

- March 2025: DSM expanded its Delvo® Guard bio-protective culture range to help yogurt manufacturers extend shelf life naturally while improving texture and processing control.

- May 2025: Chr. Hansen introduced VEGA Boost Cultures, enabling allergen-free, dairy-free cream cheese formulations using fava bean bases.

Outlook

Despite challenges such as regulatory complexity, raw-material price fluctuations, and higher R&D costs, continuous innovation is expected to broaden application scope, including solutions compatible with heat-treated foods. As clean-label, organic, and sustainability trends intensify, protective cultures are set to become a cornerstone of modern food preservation strategies worldwide.