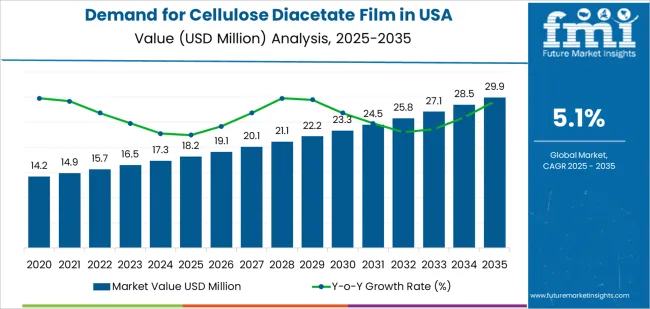

The United States Cellulose Derivative Market is poised for significant expansion, with the industry projected to grow from approximately USD 2.5 billion in 2025 to USD 4.1 billion by 2035, representing a robust growth trajectory as demand accelerates across key sectors including pharmaceuticals, food processing, cosmetics, and construction. This upward momentum underscores the increasing adoption of sustainable, high-performance materials and the vital role cellulose derivatives play in meeting modern manufacturing challenges.

Cellulose derivatives — naturally sourced polymers such as methyl cellulose, ethyl cellulose, and carboxymethyl cellulose — are becoming essential building blocks for businesses seeking eco-friendly, bio-based solutions. As more manufacturers seek to optimize performance while reducing environmental impact, these versatile materials are gaining traction both among established chemical producers and emerging innovators looking to expand their footprint in the U.S. market.

Industry Leaders Drive Market Stability and Innovation

Several legacy manufacturers continue to anchor the U.S. cellulose derivative landscape, leveraging decades of expertise to supply high-quality products that meet stringent regulatory and performance standards. Companies such as Dow Chemical Company, Ashland Global Holdings Inc., Rayonier Advanced Materials Inc., CP Kelco, and Celanese Corporation remain leading contributors to market supply, driving innovation in product formulations and broadening the spectrum of applications. These firms are boosting their R&D capabilities to tailor cellulose derivatives for advanced drug delivery systems, next-generation food formulations, and novel industrial applications.

At the same time, emerging players and mid-tier manufacturers are actively entering the space, bringing fresh perspectives and nimble approaches that challenge traditional production paradigms. These newer entrants often focus on specialized technologies — such as recycled cellulose feedstocks, high-purity derivatives optimized for sensitive biochemical processes, and smart materials that respond to environmental stimuli — adding competitive dynamism and accelerating overall market growth.

Growing Demand Across End-Use Segments

The pharmaceutical industry remains the largest end user of cellulose derivatives in the United States, accounting for nearly one-third of total demand. Manufacturers in this sector rely on these materials as excipients, binders, stabilizers, and controlled-release agents in oral dosage forms. Rising healthcare innovation and an expanding pipeline of complex drug formulations are key factors pushing pharmaceutical demand upward.

In the food and beverage domain, cellulose derivatives are prized for their ability to act as natural thickeners, emulsifiers, and texture enhancers. As consumer preference shifts toward “clean label” products and ingredients perceived as healthier and more transparent, food manufacturers are increasingly incorporating cellulose-based components into their products.

Other sectors such as personal care, cosmetics, construction, and specialty chemicals are also contributing to the uptick in demand. In construction, for instance, cellulose derivatives improve water retention and workability in mortars and plasters, while in personal care they enhance product texture and stability.

To access the complete data tables and in-depth insights, request a sample report here

Technological Advancements Power New Applications

Innovation in cellulose derivative technology is a key theme shaping the market’s evolution. Manufacturers are deploying advanced processing methods to produce derivatives with unique functionality — from modified cellulose esters with tailored solubility to ultra-fine grades that boost performance in high-precision applications.

Emerging technologies such as digitally controlled manufacturing platforms and real-time quality monitoring systems are enabling producers to consistently deliver high-specification cellulose derivatives that meet the demands of sophisticated end users. These technological investments are not only improving product quality but also accelerating time-to-market for customized solutions.

Sustainability and Regulatory Alignment Offer Competitive Edge

A notable trend influencing both established and new market participants is the focus on sustainability. Cellulose derivatives’ renewable nature aligns with corporate environmental goals and regulatory pressures aimed at reducing reliance on synthetic polymers. Manufacturers that emphasize sustainable sourcing — including recycled or circular feedstocks — are seeing increased interest from brands committed to greener product portfolios.

Additionally, compliance with food and pharmaceutical regulations remains a priority, prompting producers to invest in high-purity, well-characterized cellulose derivatives that satisfy global quality benchmarks.

Market Outlook and Future Growth Prospects

The outlook for the U.S. cellulose derivative market is decidedly positive, with anticipated steady growth through 2035. The combination of strong demand, innovative product development, sustainability initiatives, and cross-industry adoption positions this market as a dynamic area for both traditional chemical giants and new technology-driven manufacturers.

As the industry evolves, collaboration between research institutions, material scientists, and end users will remain crucial to unlocking new applications and delivering products that meet the performance and environmental expectations of tomorrow’s economy.