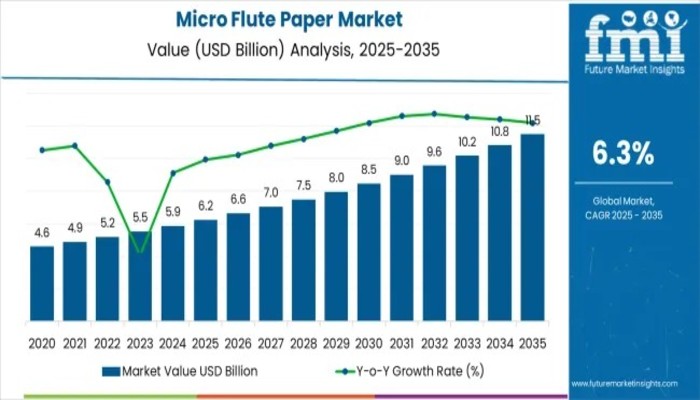

The global micro flute paper market is entering a defining decade of transformation, advancing from USD 6.2 billion in 2025 to USD 11.5 billion by 2035 at a steady CAGR of 6.3%. This accelerated growth reflects a structural shift within the packaging ecosystem, driven by lightweight corrugated formats, rising e-commerce shipments, and the increasing adoption of premium retail-ready packaging.

According to Future Market Insights, the rapid move toward thin-wall corrugated technology illustrates the market’s growing preference for compact, printable, and cost-efficient packaging systems across food, beverage, electronics, cosmetics, and consumer goods.

Unlock Growth Potential – Request Your Sample Now and Explore Market Opportunities!

A Decade of Evolution in Lightweight Packaging

Between 2025 and 2030, the market is set to rise from USD 6.2 billion to USD 8.1 billion, accounting for 36% of total decade growth. This early phase is marked by growing converter acceptance of micro flute substrates, particularly E- and F-flute, supported by improvements in thin-wall production, standardized flute specifications, and stable 65-70% efficiency levels across applications.

Established manufacturers like International Paper, WestRock, and Smurfit Kappa are strengthening their product portfolios, while new entrants focus on alternative flute geometries and enhanced surface treatments to meet global print quality standards.

Micro flute paper’s expanding role in logistics and parcel packaging is underscored by its high crush resistance and superior cushioning capabilities. As global parcel volumes rise, brands increasingly rely on micro flute options to minimize damage, reduce freight costs, and enhance unboxing experiences-key priorities for electronics, cosmetics, personal care, and small consumer goods shipped through expanding e-commerce networks.

Technology Innovation Reshapes Market Dynamics

The next wave of industry advancement is defined by enhanced flute formation technologies, precision-engineered substrate surfaces, and high-speed converting systems. Advanced flute types-E-flute, F-flute, and N-flute-offer superior foldability, print uniformity, and strength-to-weight advantages. Automated converting lines, die-cutting platforms, and digital printing compatibility are enabling converters to meet large-scale customization needs without compromising efficiency.

At the same time, the push for supply chain optimization is accelerating demand for micro flute structures that reduce material usage while maintaining robust protective characteristics. Their ability to support compact, space-saving packaging formats is reshaping storage and distribution economics worldwide.

Market Momentum Strengthens Through 2035

From 2030 to 2035, the market will grow from USD 8.1 billion to USD 11.5 billion, contributing 64% of total decade expansion. This period marks the mainstream integration of micro flute systems across automated converting and high-volume packaging operations. The focus shifts from flute innovation to end-to-end packaging performance, system compatibility, and multi-industry penetration.

Key Stats (2025-2035):

- Market Value 2025: USD 6.2 billion

- Market Forecast 2035: USD 11.5 billion

- CAGR: 6.3%

- Leading Flute Type: E-flute (44% share)

- Top Regions: North America, Europe, Asia-Pacific

- Top Players: International Paper, WestRock, Smurfit Kappa, DS Smith, Mondi

Why the Market is Growing: Three Core Catalysts

- E-Commerce Expansion: Lightweight, crush-resistant micro flute packaging reduces shipping costs while ensuring product protection-critical for D2C, subscription box, and electronics fulfillment.

- Retail Modernization: Brands are prioritizing premium shelf-ready packaging that enhances visual appeal, supports fine printing, and improves consumer engagement at point-of-sale.

- Space Optimization: Warehousing and distribution networks increasingly adopt micro flute designs that maximize storage density without compromising structural integrity.

Opportunities Across High-Growth Packaging Segments

The decade ahead presents significant opportunity pathways including:

- E-commerce packaging, offering USD 2.2-2.9 billion in value through specialized micro flute mailers, inserts, and subscription boxes.

- Asia-Pacific expansion, driven by rapid adoption in China (7.4% CAGR) and India (7.1% CAGR).

- Premium food & beverage packaging, capturing USD 1.7-2.3 billion through specialty coatings and display-ready formats.

- Advanced printing technologies, including metallic finishes, HD graphics, and embossed surfaces for brand-intensive sectors.

- Electronics, cosmetics, and luxury goods, where precision die-cutting, anti-static capabilities, and premium finishes fuel adoption.

Competitive Landscape

The market maintains moderate concentration with International Paper, WestRock, Smurfit Kappa, DS Smith, Mondi, Cascades, Stora Enso, and Nippon Paper Industries leading the segment. Their competitive advantage lies in manufacturing depth, converting infrastructure, and access to advanced forming technologies. Emerging players compete through specialized coatings, cost-effective production, and rapid-response printing solutions tailored to e-commerce and retail requirements

Why FMI: https://www.futuremarketinsights.com/why-fmi

About Future Market Insights (FMI)

Future Market Insights, Inc. (FMI) is an ESOMAR-certified, ISO 9001:2015 market research and consulting organization, trusted by Fortune 500 clients and global enterprises. With operations in the U.S., UK, India, and Dubai, FMI provides data-backed insights and strategic intelligence across 30+ industries and 1200 markets worldwide.

Contact Us:

Future Market Insights Inc.

Christiana Corporate, 200 Continental Drive,

Suite 401, Newark, Delaware – 19713, USA

T: +1-347-918-3531

For Sales Enquiries: sales@futuremarketinsights.com

Website: https://www.futuremarketinsights.com

LinkedIn| Twitter| Blogs | YouTube