The global Automotive Ultracapacitor Market is entering an accelerated growth phase, driven by rapid electrification of vehicles and the rising need for high-power, fast-response energy storage systems. The market is valued at USD 6.5 billion in 2025 and is forecast to reach USD 25.4 billion by 2035, expanding at a compound annual growth rate (CAGR) of 14.6% over the decade.

Year-by-year analysis confirms a strong and compounding adoption curve. Between 2025 and 2030, market value is expected to nearly double from USD 6.5 billion to USD 12.8 billion, supported by a five-year CAGR of approximately 14.8%. Annual value additions rise steadily from USD 0.9 billion in the early years to USD 1.6 billion by the end of the period, reflecting rapid OEM integration of ultracapacitors in regenerative braking, start-stop systems, and short-burst power delivery applications.

Subscribe for Year-Round Insights → Stay ahead with quarterly and annual data updates

https://www.futuremarketinsights.com/reports/sample/rep-gb-23344

From 2030 to 2035, growth accelerates further as the market expands from USD 12.8 billion to USD 25.4 billion, posting a sustained CAGR of around 14.4%. Annual incremental gains are projected to surpass USD 3.3 billion by the final forecast year. This phase represents a structural transition from early adoption to large-scale deployment, especially in high-performance electric vehicles, heavy-duty transport systems, and grid-connected mobility platforms.

Ultracapacitors Move from Niche to Strategic Energy Storage Component

Automotive ultracapacitors are evolving from specialized components into strategic enablers of next-generation powertrain architecture. They currently account for approximately 2.1% of the global automotive energy storage market, reflecting their growing importance in applications requiring rapid charge-discharge cycles, high power density, and extended operational lifecycles.

Within the automotive power electronics ecosystem, ultracapacitors represent an estimated 2.9% market share, largely driven by their integration with regenerative braking and start-stop systems. In the electric and hybrid vehicle components segment, they command roughly 2.6% of total value, reinforcing their role in managing peak power demands and reducing dependency on primary lithium-ion battery systems.

Their contribution to automotive lightweighting and efficiency solutions stands at about 1.9%, as these systems deliver improved energy efficiency without adding significant structural weight. In commercial vehicle electrification, ultracapacitors account for nearly 2.4% of market value, supported by increasing adoption across electric buses, delivery vehicles, and heavy-duty trucks.

Product and Vehicle Segments Show Strong Structural Leadership

By technology type, double-layered capacitors dominate the landscape, accounting for 52.0% of total market share in 2025. Their leadership is supported by superior energy density, low equivalent series resistance, and extended cycle life. Ongoing advances in electrode material science and improved system-level integration with lithium-ion batteries have positioned this segment as the preferred solution for braking energy recovery and voltage stabilization.

In terms of vehicle type, passenger cars represent 61.0% of total market demand in 2025. The integration of ultracapacitors in light-duty vehicles is being driven by growing deployment of start-stop functionality, expanding onboard electronics, and tightening global emission standards. The compact footprint and modular design of modern ultracapacitor systems have allowed seamless incorporation within passenger vehicle platforms.

By propulsion architecture, electric vehicles (EVs) account for 58.0% of market share. Ultracapacitors are increasingly being used to support acceleration, hill-start assist, and transient power delivery, actively extending battery life and improving overall drivetrain efficiency. These advantages are critical in high-frequency cycling environments where traditional batteries experience accelerated degradation.

Regional Growth Signals a Global Technology Ramp-Up

Regional analysis highlights a strong divergence in growth intensity and manufacturing focus. Asia-Pacific has emerged as both a production powerhouse and a primary consumption market, driven by large-scale EV manufacturing, particularly in China, Japan, and South Korea.

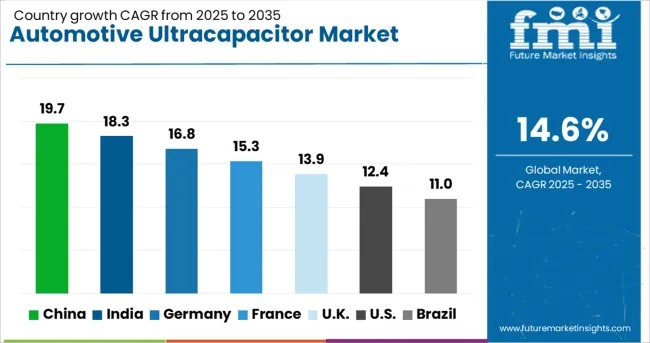

Country-level data reveals particularly aggressive expansion trajectories:

China is projected to grow at a 19.7% CAGR, supported by large-scale electric bus deployment, domestic ultracapacitor manufacturing, and strong policy-level support for fleet electrification.

India follows with an 18.3% CAGR, fueled by increasing adoption of electric three-wheelers, buses, and compact passenger vehicles.

Germany is forecast to expand at a 16.8% CAGR, driven by premium automotive engineering and early adoption of graphene-based electrode technologies.

France is expected to grow at 15.3% CAGR, while the United Kingdom is projected at 13.9% CAGR, reflecting rising integration in hybrid public transport and performance vehicles.

The United States market is anticipated to grow at 12.4% CAGR, supported by steady adoption in electric trucks, SUVs, and commercial fleet applications.

Technology Innovation Reshapes Performance Benchmarks

Continuous innovation is redefining the performance ceiling of automotive ultracapacitors. Developments in graphene-based and carbon nanotube electrodes are delivering significant improvements in energy density without compromising rapid discharge capability. Thermal management advancements are increasing operational stability under extreme temperature conditions, expanding suitability for harsh automotive environments.

Hybrid energy storage architectures, combining ultracapacitors with lithium-ion batteries, are gaining traction as OEMs seek to balance power and energy density. These systems enable improved regenerative energy capture, smoother power delivery, and longer battery lifecycles, while advanced packaging designs are reducing spatial constraints and simplifying vehicle integration.

Strategic Partnerships and Competitive Momentum

The competitive landscape is defined by a mix of global technology leaders and specialized innovators. Major participants include Maxwell Technologies, Skeleton Technologies, Panasonic Corporation, Nippon Chemi-Con Corporation, Murata Manufacturing Co., Ltd., Nichicon Corporation, Eaton Corporation, KEMET Corporation, AVX Corporation, and Ioxus, Inc.

Personalize Your Experience: Ask for Customization to Meet Your Requirements

https://www.futuremarketinsights.com/customization-available/rep-gb-23344

Strategic collaborations are accelerating commercialization. In February 2025, Skeleton Technologies announced a partnership with Honda to deploy high-performance ultracapacitors in motorsport energy-recovery systems, demonstrating viability in extreme performance environments. In October 2024, Panasonic Corporation began commercial production of automotive-grade, high-temperature hybrid capacitors designed to enhance thermal stability and reduce electronic control unit (ECU) footprint.

Outlook

The automotive ultracapacitor market is transitioning from experimental deployment to structural integration within global vehicle platforms. With sustained double-digit growth, accelerating OEM partnerships, and rapid material science breakthroughs, ultracapacitors are positioning themselves as essential components of next-generation electric and hybrid mobility. The decade ahead is expected to be defined not by whether these systems are adopted, but by how rapidly manufacturers scale and optimize them for mass-market deployment.

About Future Market Insights (FMI)

Future Market Insights, Inc. (FMI) is an ESOMAR-certified, ISO 9001:2015 market research and consulting organization, trusted by Fortune 500 clients and global enterprises. With operations in the U.S., UK, India, and Dubai, FMI provides data-backed insights and strategic intelligence across 30+ industries and 1200 markets worldwide.