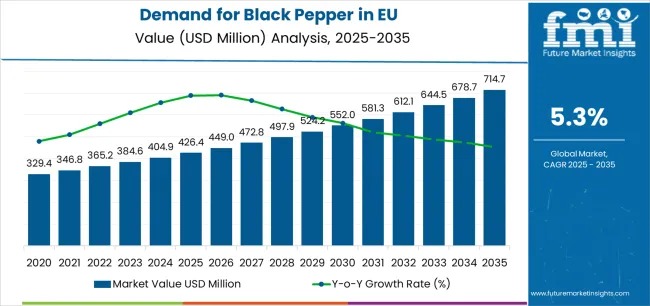

The EU black pepper industry is entering a sustained growth phase, with market value projected to rise from USD 426.4 million in 2025 to USD 714.7 million by 2035, advancing at a CAGR of 5.3%. According to peer-referenced analysis from Future Market Insights (FMI), this expansion reflects the convergence of evolving culinary preferences, rising food processing requirements, and a growing consumer shift toward authentic, high-quality spices across both household and professional kitchens.

Black pepper continues to hold a central role in Europe’s spice economy, transitioning from a basic seasoning to a differentiated ingredient valued for origin, aroma, and functionality. Demand is being reinforced by premiumization trends, the clean-label movement, and the expansion of ready-to-eat and ethnic food categories that rely on consistent natural flavor solutions.

Get Exclusive Access To Data Tables, Market Sizing Dashboards, And Analyst Insights. Request Sample Report!

Market Snapshot: EU Black Pepper at a Glance

- Market Value (2025): USD 426.4 million

- Forecast Value (2035): USD 714.7 million

- Forecast CAGR (2025–2035): 5.3%

- Leading Product Form: Whole Pepper (63.0%)

- Key End Use: Industrial (40.0%)

- Top Distribution Channel: B2B (56.0%)

Growth Phases Reflect Accelerating Momentum

Between 2025 and 2030, the EU black pepper market is expected to grow to USD 553.4 million, adding USD 127.0 million in value and accounting for 43.6% of total decade growth. This phase is supported by rising interest in global cuisines, stronger demand from food manufacturers for natural seasonings, and broader retail availability of premium pepper varieties.

From 2030 to 2035, growth accelerates further, with sales projected to reach USD 714.7 million, contributing an additional USD 164.4 million or 56.4% of total forecast expansion. This period will be defined by mainstream adoption of specialty and organic peppers, improved traceability, sustainable sourcing programs, and packaging innovations that preserve freshness while meeting environmental expectations.

Whole Pepper Retains Leadership as Formats Diversify

Whole pepper remains the dominant format, accounting for 63.0% share in 2025, though its share is expected to moderate to 60.0% by 2035 as ground and crushed variants gain traction. Whole pepper’s strength lies in its superior flavor retention, longer shelf life, and suitability for fresh grinding—attributes valued by both consumers and foodservice operators.

Ground pepper, projected to grow from USD 119.4 million in 2025 to USD 215.3 million by 2035, benefits from convenience and standardized mesh sizes required by industrial processors. Crushed pepper, while smaller in scale, shows strong momentum in artisanal foods and gourmet applications, expanding from USD 38.4 million to USD 71.8 million over the forecast period.

Industrial Demand Anchors Market Stability

Industrial applications represent the largest end-use segment, accounting for 40.0% of market share in 2025. Food processors, meat producers, sauce manufacturers, and ready-meal companies rely on black pepper for consistent flavor delivery, clean-label compliance, and functional performance. Long-term supply contracts, quality assurance, and standardized piperine content are critical procurement factors.

Foodservice demand is projected to expand at a faster pace, supported by tourism recovery, dining-out culture, and the growth of delivery and takeaway formats. Retail and household consumption remains resilient, fueled by home cooking trends, culinary education via media, and rising consumer interest in origin-specific and organic spices.

Organic Segment Gains Share Amid Sustainability Focus

Organic black pepper is emerging as a key value driver, with market share expected to increase from 26.0% in 2025 to 30.0% by 2035. Premium pricing, typically 35–50% above conventional products, is supported by strong European demand for certified, traceable, and pesticide-free ingredients. Health-conscious consumers and premium foodservice operators are accelerating adoption despite higher costs.

Regional Insights Highlight Diverse Growth Patterns

Germany maintains leadership with 28.7% market share, driven by its large food processing base and strong organic penetration. France stands out for culinary sophistication and premium pepper demand, while Spain and the Netherlands demonstrate higher growth rates supported by tourism, innovation, and advanced logistics infrastructure. Emerging markets across Eastern and Nordic Europe are contributing incremental growth through modern retail expansion and sustainability-driven consumption.

Competitive Landscape Remains Fragmented

The EU black pepper market is moderately fragmented, with global players such as McCormick & Company, Olam Food Ingredients, and ADM competing alongside regional importers and specialty distributors. Competitive differentiation centers on supply chain resilience, sustainable sourcing, origin diversification, and value-added formats such as grinders, organic lines, and standardized industrial solutions.

Outlook Through 2035

With strong fundamentals, expanding applications, and rising quality awareness, the EU black pepper industry is well-positioned for long-term growth. Companies investing in sustainability credentials, traceability technologies, and product innovation are expected to capture outsized value as Europe’s spice market continues to evolve beyond volume-driven growth toward premium, data-driven differentiation.