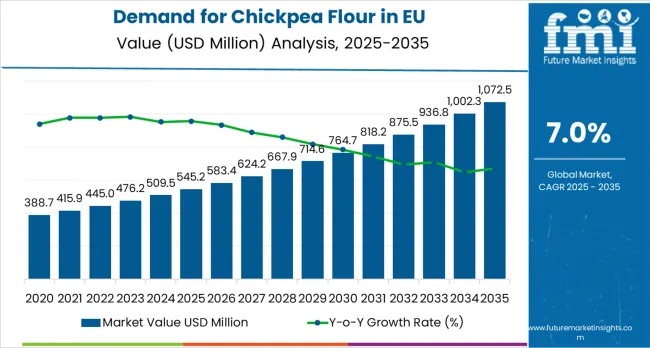

The demand for chickpea flour in the EU is entering a decisive growth phase, supported by structural shifts in dietary preferences, food innovation, and regulatory alignment with alternative nutrition. Valued at USD 545.2 million in 2025, the EU chickpea flour market is forecast to reach USD 1,072.5 million by 2035, expanding at a CAGR of 7.0%. This growth reflects accelerating adoption of plant-based, gluten-free, and protein-rich food solutions across both household and commercial food segments.

Market dynamics are increasingly shaped by consumers seeking nutrient-dense, allergen-friendly ingredients that offer functional performance comparable to wheat flour while delivering superior protein and fiber content. Chickpea flour has emerged as a preferred solution, particularly in bakery, snack, and ready-to-eat food categories, which together account for nearly 70% of total end-use consumption in the EU.

Get Exclusive Access To Data Tables, Market Sizing Dashboards, And Analyst Insights. Request Sample Report!

According to FMI’s analysis of global dietary behavior and flavor adoption patterns, companies offering high-quality, organic, fortified, or functionally enhanced chickpea flour are positioned to gain incremental market share. In contrast, suppliers with limited product differentiation or inconsistent quality standards may face gradual erosion as competition intensifies. Between 2025 and 2030, early movers investing in innovation and distribution strength are expected to outperform, while the 2030–2035 period will reward players leveraging branding, e-commerce, and diversified portfolios.

Market Structure and Key Takeaways

The EU chickpea flour industry demonstrates a clear concentration around mainstream consumption, with conventional chickpea flour accounting for 86.4% of total demand. This dominance reflects cost efficiency, wide retail availability, and strong acceptance among general health-conscious consumers. Organic and non-GMO variants, while still niche, are gaining momentum and represent 15–20% of new product launches, driven by clean-label and sustainability trends.

Other notable market characteristics include:

- Rising use of chickpea flour in bakery, snacks, and ready meals due to texture stability and nutritional enhancement

- Expanding household and foodservice usage, now representing approximately 30% of demand

- Increasing focus on fortified formulations addressing protein enrichment and functional nutrition

Overall, the market is expected to deliver net share gains for companies prioritizing quality, innovation, and regulatory compliance, while less adaptive players face competitive pressure.

Why Chickpea Flour Demand Is Rising Across the EU

Growth in the EU chickpea flour market is underpinned by a fundamental shift toward plant-based nutrition and dietary inclusivity. European consumers are increasingly reducing gluten and animal protein intake, while seeking ingredients that support balanced nutrition without compromising culinary performance.

Modern consumers and culinary professionals value chickpea flour for its:

- Naturally gluten-free profile

- High protein and fiber content

- Versatility across sweet and savory applications

- Compatibility with vegan, vegetarian, and flexitarian diets

Regulatory bodies across EU member states are also reinforcing market confidence through clearer guidelines on nutritional claims, labeling accuracy, and food safety protocols. Concurrently, European food science institutions continue to publish research supporting chickpea flour’s role in protein supplementation, fiber enhancement, and dietary optimization.

Segmental Insights: Product Type and Claims

By product type, desi chickpea flour dominates with a 59.3% market share in 2025, supported by its higher fiber content, robust flavor profile, and widespread use in ethnic and traditional cooking. Desi variants are particularly favored in Middle Eastern, Indian, Mediterranean, and North African cuisines, which are gaining popularity across Western and Central Europe.

Key advantages driving the desi segment include:

- Superior nutritional density and protein profile

- Authentic taste alignment with ethnic recipes

- Established processing efficiencies and supply infrastructure

By product claims, the conventional segment’s 86.4% share reflects strong mainstream adoption. Within this segment, enhanced processing variants are gaining traction, offering improved texture, shelf stability, and functional performance for commercial food manufacturers.

Country-Level Growth Outlook

Germany leads the EU chickpea flour market with a 26.3% share in 2025 and a projected 7.1% CAGR through 2035, supported by a mature health food ecosystem and high gluten-free awareness. France follows with 19.4% share, driven by culinary innovation and ethnic cuisine integration, while Italy holds 13.9%, benefiting from Mediterranean diet alignment.

Spain and the Netherlands each register steady 7.0% CAGR, supported by health-conscious cooking trends and sustainable food initiatives. The Rest of Europe shows slower momentum due to market consolidation, though emerging opportunities persist in Nordic and Eastern European countries.

Competitive Landscape

The competitive environment includes multinational ingredient suppliers, specialized pulse processors, and regional European manufacturers. Companies are investing in:

- European processing capacity and advanced grinding technologies

- Sustainable chickpea sourcing and certification programs

- Product portfolio expansion and direct-to-consumer channels

Key players shaping the market include Ingredion Inc., Paragh Agro, The Scoular Company, SunOpta, Anchor Ingredients, AGT Food and Ingredients, Best Cooking Pulses, Diefenbaker Spice & Pulse, Sharayu Organics, and European regional processors. Strategic partnerships, quality certifications, and culinary collaborations remain central to capturing share in this evolving market.

As plant-based diets and gluten-free lifestyles continue to gain traction, chickpea flour is positioned to become a staple ingredient across European food systems—transforming from a niche alternative into a mainstream nutritional solution.