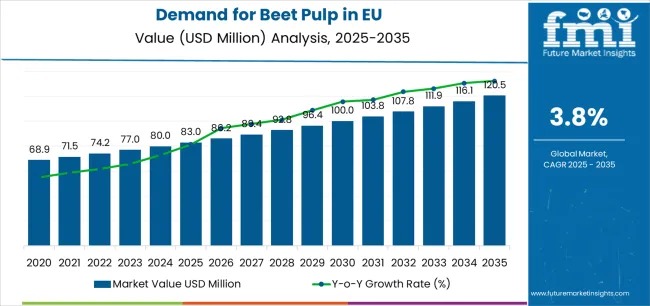

The EU beet pulp industry is entering a phase of steady, sustainability-led expansion, underpinned by structural shifts in livestock nutrition and circular agriculture. The market is projected to grow from USD 83 million in 2025 to USD 120.5 million by 2035, advancing at a CAGR of 3.8%. This growth reflects increasing reliance on cost-effective, digestible fiber sources as European dairy and livestock producers optimize feed efficiency amid rising input costs and stricter sustainability expectations.

Beet pulp, derived as a byproduct of sugar beet processing, has transitioned from a secondary output into a strategically valued feed ingredient. As highlighted in FMI’s analysis of global dietary behavior and feed formulation trends, the EU beet pulp industry is expected to expand 1.45X over the next decade, supported by stable sugar beet production, improved processing infrastructure, and broader recognition of beet pulp’s nutritional and environmental advantages.

Get Exclusive Access To Data Tables, Market Sizing Dashboards, And Analyst Insights. Request Sample Report!

Market Snapshot: A Decade of Measured Expansion

Between 2025 and 2030, EU beet pulp demand is forecast to rise from USD 83 million to USD 96.6 million, adding USD 16.3 million in value. This phase represents 45.5% of total decade growth, driven by increased adoption in dairy rations, heightened awareness of rumen-friendly fiber sources, and growing alignment with circular economy principles that valorize sugar industry byproducts.

From 2030 to 2035, the market is expected to accelerate further, expanding from USD 96.6 million to USD 120.5 million. This second phase contributes USD 19.5 million, or 54.5% of total growth, reflecting advancements in drying, pelletization, and preservation technologies. Feed manufacturers are increasingly integrating beet pulp into specialized formulations for performance animals, supported by research highlighting its prebiotic properties and consistent energy release.

Why Demand for Beet Pulp Is Rising Across the EU

The growth trajectory of beet pulp is closely tied to evolving livestock production priorities. European farmers are under pressure to improve feed efficiency while reducing environmental impact. Beet pulp offers a compelling solution, combining digestible fiber, moderate energy density, and excellent palatability with a lower carbon footprint than many conventional fiber sources.

Key demand drivers include:

- Rising dairy and cattle production requiring stable rumen health

- Preference for sustainable, locally sourced feed ingredients

- Regulatory emphasis on safe, traceable, and standardized feed inputs

- Proven nutritional benefits validated through feeding trials

As a result, beet pulp is increasingly treated as an essential feed component rather than a residual byproduct.

Segment Insights: Dried Pulp and Cow Feed Dominate

By product type, dried beet pulp (pellets and shreds) leads the EU market with a 45.6% share in 2025, projected to reach 47.6% by 2035. Its dominance is driven by superior storage stability, ease of handling, and compatibility with mechanized feeding systems. Dried pulp enables year-round utilization and long-distance trade without compromising nutritional integrity.

By application, cow feed accounts for 56.0% of total demand, reflecting Europe’s extensive dairy sector. Beet pulp is widely used in total mixed rations to support rumen function, enhance palatability, and deliver fermentable fiber without increasing acidosis risk. While cattle remain the primary consumers, faster growth is emerging in equine and small ruminant segments, slightly moderating cattle’s share over time.

Distribution and Product Nature Trends

Modern trade channels, including agricultural cooperatives and bulk feed suppliers, represent 35.0% of EU beet pulp sales in 2025, supported by established logistics and technical advisory services. However, online and direct-to-farm channels are gaining traction, expected to lift their combined share to nearly 20% by 2035.

By nature, molassed beet pulp holds a 55.0% share, favored for its enhanced palatability, higher energy density, and binding properties in pelleted feeds. Demand remains stable as producers balance performance benefits with cost and storage considerations.

Country-Level Dynamics: Germany and the Netherlands Lead Growth

Germany remains the largest and fastest-growing EU market, expanding from USD 28.1 million in 2025 to USD 42.6 million by 2035, at a 4.3% CAGR. Integrated sugar-livestock value chains, advanced feed manufacturing, and strong dairy demand underpin its leadership.

France follows with solid growth at 3.7% CAGR, supported by large sugar beet cooperatives and a diversified livestock base. The Netherlands, despite its smaller size, records a robust 4.1% CAGR, driven by intensive livestock systems and its role as a European feed trading hub.

Competitive Landscape: Scale Meets Specialization

The EU beet pulp market is moderately fragmented. Tereos and Nordzucker together account for over 40% of total sales, leveraging scale, processing efficiency, and year-round supply capabilities. The remaining 58% is held by regional sugar producers, cooperatives, and specialized processors focusing on niche formulations, sustainability certification, and localized distribution.

Outlook

As sustainability, feed efficiency, and circular economy principles reshape European agriculture, beet pulp is set to play a growing strategic role. Continued investment in processing technology, nutritional enhancement, and traceability will be critical in capturing value and supporting the EU beet pulp industry’s steady growth through 2035.