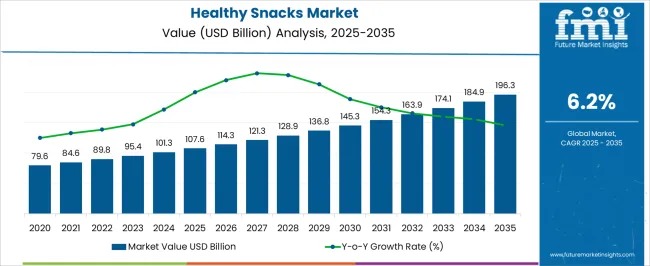

The global healthy snacks market is undergoing a structural shift as consumers worldwide re-evaluate everyday eating habits through a nutrition-first lens. Valued at USD 107.6 billion in 2025, the market is projected to reach USD 196.3 billion by 2035, expanding at a compound annual growth rate (CAGR) of 6.2% over the forecast period. Early-stage growth is predominantly volume-driven, reflecting broad consumer migration from conventional processed snacks toward healthier alternatives such as protein-enriched bars, baked chips, and fruit- and nut-based blends.

Urbanization, busier lifestyles, and rising awareness of diet-related health risks are reshaping household food choices across both developed and emerging economies. Improved accessibility through supermarkets, specialty health stores, and rapidly expanding digital retail platforms has accelerated adoption, enabling healthy snacks to transition from niche products into mainstream consumption staples.

Get Exclusive Access To Data Tables, Market Sizing Dashboards, And Analyst Insights. Request Sample Report! https://www.futuremarketinsights.com/reports/sample/rep-gb-25933

As the market progresses beyond 2030, price-led growth becomes increasingly influential. Premiumization is reshaping category economics as consumers demonstrate willingness to pay higher prices for snacks positioned around organic sourcing, plant-based formulations, functional fortification, and clean-label claims. This shift lifts average unit prices and strengthens margins, especially for brands able to differentiate through innovation, sustainability credentials, and transparent labeling. Over the decade, the market reflects a 1.82× growth multiple, with volume fueling early momentum and premium pricing driving long-term value expansion.

Market Snapshot and Structural Composition

In 2025, whole grains and seeds snacks emerge as the leading product segment, accounting for approximately 19.6% of total market share. These products align strongly with consumer demand for fiber-rich, minimally processed foods that support digestive health and sustained energy. From a structural standpoint, five parent markets collectively shape demand and innovation:

- Packaged food (35%), driven by reformulation of traditional snacks

- Functional foods (25%), featuring protein, fiber, and vitamin fortification

- Beverages (15%), including drinkable snack formats

- Bakery and confectionery (15%), redesigned with natural sweeteners and whole grains

- Retail and e-commerce (10%), expanding product access and variety

This convergence positions healthy snacks as one of the most dynamic segments within the global food industry.

Innovation, Convenience, and Sustainability at the Core

Recent developments underscore a clear focus on natural ingredients, functional benefits, and sustainability. Manufacturers are launching plant-based protein bars, low-sugar fruit snacks, and nut-based blends enriched with probiotics, adaptogens, and superfoods. Packaging innovation is also gaining momentum, with emphasis on portion control, resealable designs, and eco-friendly materials that align with evolving consumer values.

The rapid rise of online retail and subscription-based snack models has further broadened market reach, particularly among urban millennials and Gen Z consumers who prioritize convenience without compromising nutritional quality.

Segment Insights: Whole Grains and Retail Leadership

The whole grains and seeds snacks segment, representing nearly 20% of global demand, continues to benefit from clean-label momentum and growing research linking whole-grain intake with long-term health outcomes. Incorporation of superfoods such as chia, flax, and quinoa into bars, crackers, and trail mixes enhances both nutritional density and consumer appeal.

On the distribution front, retail stores dominate with a 39% share, supported by established infrastructure, in-store visibility, and impulse purchasing behavior. Supermarkets and specialty health food stores remain critical touchpoints, particularly for new product discovery and sampling. While e-commerce continues to grow rapidly, physical retail retains its leadership due to immediate availability and consumer trust in product inspection.

Regional and Country-Level Growth Dynamics

Geographically, Asia Pacific accounts for more than 35% of global consumption, driven by urbanization, dietary transitions, and expanding middle-class populations. China leads with an 8.4% CAGR, supported by functional food demand and strong e-commerce penetration, while India follows at 7.8%, fueled by millet-based innovations and quick-commerce growth. Europe demonstrates steady expansion, with Germany growing at 7.1%, reflecting strong organic and plant-based adoption.

North America remains a mature but resilient market, with the United States growing at 5.3%, anchored by protein-rich, keto-friendly, and clean-label snack formats.

Competitive Landscape and Strategic Positioning

Competition in the healthy snacks market centers on ingredient transparency, functional nutrition, and convenient formats. Companies such as Annie’s, KIND Snacks, Clif Bar, Quest Nutrition, RXBAR, and LesserEvil Snacks continue to invest in reformulation, branding, and sustainability to strengthen consumer loyalty. Emerging brands and startups are intensifying competition through niche positioning, upcycled ingredients, and direct-to-consumer models.

Outlook

Despite challenges related to ingredient costs, supply volatility, and regulatory compliance, the healthy snacks market is positioned for sustained growth. As nutrition awareness deepens and premium, functional products gain acceptance, the category is expected to remain a profitable and strategically important segment within the global food industry through 2035.