The global Steering Wheel Switches Market is entering a decade of steady, functionality-driven expansion as automotive manufacturers prioritize driver-centric control architectures and safer in-cabin experiences. The market is valued at USD 3.5 billion in 2025 and is projected to reach USD 4.1 billion by 2035, expanding at a compound annual growth rate (CAGR) of 1.8% over the forecast period.

Market modelling reveals a distinctly phased growth pattern. From 2025 to 2028, the market advances from USD 3.5 billion to USD 3.6 billion, reflecting annual increments of approximately USD 0.03-0.05 billion. This period is characterized by high product penetration and mature adoption across mainstream vehicle categories, which has constrained rapid value expansion despite broad deployment.

Subscribe for Year-Round Insights → Stay ahead with quarterly and annual data updates

https://www.futuremarketinsights.com/reports/sample/rep-gb-23348

Between 2029 and 2032, the market accelerates from USD 3.7 billion to USD 3.9 billion, with annual value additions increasing to USD 0.07-0.10 billion. This phase represents a structural inflection point, as automotive OEMs deepen the integration of multifunction controls, driver-assistance interfaces, and connected vehicle features directly into the steering wheel architecture. From 2033 to 2035, the market stabilizes, reaching USD 4.1 billion, with annual increments of around USD 0.05 billion, reflecting a transition from expansion to feature optimization and product refinement.

Steering Wheel Switches Emerge as a Core Human-Machine Interface

Steering wheel switches now occupy a strategic role within modern vehicle interiors, representing approximately 2.2% of the global automotive interior components market and 2.9% of the automotive electronics segment. Their growing importance is most visible within connected and smart vehicle platforms, where they account for about 2.5% of functional interface value, enabling seamless, hands-on control of infotainment, navigation, communication, and driver-assistance systems.

In premium and performance-oriented vehicles, steering wheel switches contribute roughly 2.4% of value creation, as tactile feedback, illuminated controls, and customized layouts become key design differentiators. Commercial vehicles are also emerging as an important adoption segment, where multifunction switches now represent approximately 2.0% of cabin system value due to their role in enhancing fleet safety and operational efficiency.

OEM Dominance and Product Innovation Define the Competitive Structure

OEM-fitted steering wheel switches account for 64.0% of total market revenue in 2025, reflecting the industry-wide shift toward factory-integrated controls. Automakers increasingly standardize switch modules across model portfolios to ensure compliance, safety consistency, and cost efficiency. Pre-installed systems have become the preferred approach for managing complex integrations with infotainment units, driver-assistance platforms, and vehicle networks.

From a product standpoint, push-type switches dominate with a 59.0% market share in 2025. Their mechanical reliability, intuitive user experience, and cost advantages have positioned them as the primary interface for frequently used functions such as volume adjustment, cruise control activation, and call handling. Continuous improvements in backlighting, tactile feedback, and haptic confirmation have further strengthened their preference across both mass-market and premium vehicles.

By functionality, audio controls lead application demand, accounting for 33.0% of market share in 2025. With in-vehicle entertainment systems becoming increasingly sophisticated, automakers are prioritizing instant, distraction-free access to volume, track navigation, and source switching. As streaming services, connected media, and voice integration expand, audio-focused switch modules are being elevated from convenience features to essential safety-enabling interfaces.

Regional Production Strength and Technology Adoption Drive Market Direction

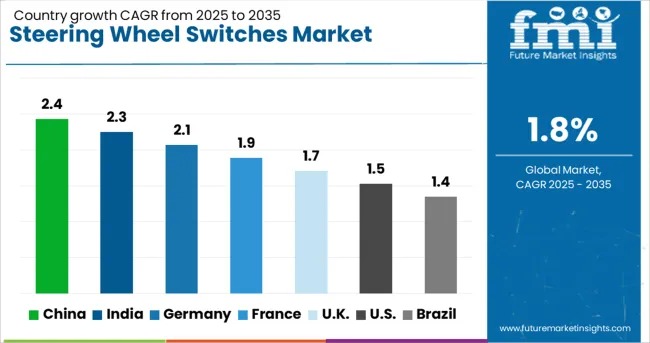

Asia-Pacific continues to lead production and adoption, backed by large-scale vehicle manufacturing and high penetration of feature-rich mid-range vehicles. China, with a 2.4% CAGR through 2035, remains the fastest-growing national market, driven by expanding integration of multifunction steering wheels in mass-market and connected vehicles. India follows closely at 2.3% CAGR, as feature upgrades rapidly move into entry- and mid-level models.

Germany, growing at 2.1% CAGR, remains the innovation hub for premium steering wheel interfaces, where haptic feedback, touch-sensitive panels, and seamless ADAS integration are becoming standard. The United Kingdom (1.7% CAGR) demonstrates stable growth through demand from luxury and specialty vehicle segments, while the United States (1.5% CAGR) reflects a mature but resilient market driven by SUV, pickup, and electric vehicle production.

Policy and Safety Dynamics Reinforce the Role of Physical Switches

A significant structural catalyst is emerging from evolving safety policy frameworks. In May 2025, Euro NCAP announced its intention to incentivize the return of physical tactile buttons for critical vehicle functions starting in 2026, highlighting concerns over driver distraction linked to touchscreen-heavy interiors. This regulatory position has effectively validated the strategic importance of steering wheel switches as a safer alternative to touch-only interfaces.

Technological advances continue to elevate switch performance. Haptic-feedback systems, touch-capacitive hybrids, water-resistant designs, and illumination technologies are becoming mainstream. The 2023 launch of a haptic-feedback steering wheel switch system by Alps Alpine marked a pivotal industry shift toward restoring tactile engagement while maintaining modern interface precision.

Personalize Your Experience: Ask for Customization to Meet Your Requirements

https://www.futuremarketinsights.com/customization-available/rep-gb-23348

Competitive Landscape Reflects High Entry Barriers and Innovation Focus

The market is characterized by strong participation from Tier-1 suppliers and OEM-integrated manufacturers. Continental, Denso, Valeo, and ZF Friedrichshafen lead in developing multifunction modules with low-latency response and ergonomic optimization. Panasonic Corporation has expanded its role by combining mechanical and capacitive interfaces, while TOKAI RIKA continues to specialize in high-precision, automaker-specific designs.

Manufacturing hubs such as Dongguan play a central role in cost-competitive production, while automakers including Toyota Motor, Nissan Motor, and Hyundai Motor increasingly integrate switch development into their in-house electronic architectures. The high barriers to entry – including strict automotive quality certifications, long validation cycles, and deep supplier-OEM integration – continue to protect established players and reinforce long-term partnerships.

Outlook

The steering wheel switches market is evolving from a purely mechanical component category into a central human-machine interface ecosystem. While growth remains gradual, the strategic value of reliable, tactile, and intuitively placed controls is rising sharply in response to safety regulations, connected vehicle applications, and shifting consumer expectations. As physical interfaces regain prominence alongside touch and voice systems, steering wheel switches are positioned to remain a critical pillar of next-generation cockpit design well beyond 2035.